Sign in

Sign in

Profile

Profile Signout

Signout

Karnataka Board 2nd PUC 12th Exam 2024 : Accountancy Important Question Answer

Karnataka 12th exams are going on and your Accountancy paper is on 9th March 2024. You have only a few hours left for the Accountancy exam.

As the Karnataka Board 2nd PUC Exam 2024 approaches, students preparing for the Accountancy paper often find themselves looking for a comprehensive resource that throws light on important questions.

In this, every important question has been sorted and collected, which is very important for your paper, so that the student can score good marks in less time. Answers to all the questions are given together.

For this we have compiled a detailed guide that breaks down important topics, provides important questions for each chapter, and aligns them with the marking scheme.

Short Answer Questions With Answers

Question 1.

State the meaning of Not-for-profit organizations.

Answer:

Not-for-profit organizations refers to the organizations that are used for the welfare of the society and are set up as charitable institutions which function without any profit motive.

Question 2.

State the meaning of Receipts and Payments Account.

Answer:

Receipt and payment account is the summary of cash and bank transactions which helps in the preparation f income and expenditure account and the balance sheet.

Question 3.

State the meaning of Income and Expenditure Account.

Answer:

It is the summary of income and expenditure for the accounting year. It is like a profit and loss account prepared on accusal basis in case of the business organization.

Question 4.

Define Partnership Deed.

Answer:

When the partnership agreement is written and signed By all the partners and is duly stamped according to the Stamp Act, it is called “Partnership Deed”.

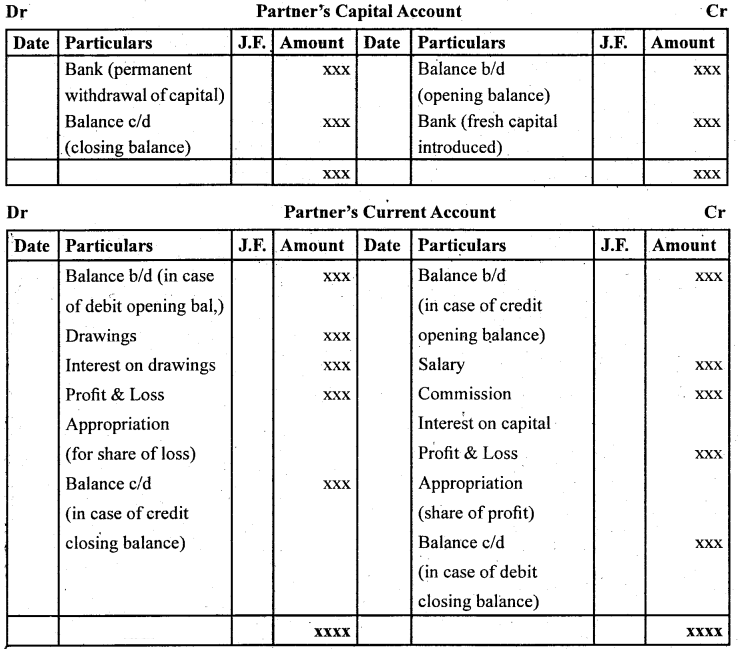

Question 3.

List the items which may be debited or credited in capital accounts of the partners when:

(i) Capitals are fixed.

(ii) Capital are fluctuating.

Answer:

(i) Capitals are fixed.

(ii) Capital are fluctuating.

Question 4.

Identify various matters that need adjustments at the time of admission of a new partner.

Answer:

The important points which require attention at the time of admission of a new partner:

- New profit sharing ratio;

- Sacrificing ratio;

- Valuation and adjustment of goodwill;

- Revaluation of assets and Reassessment of liabilities;

- Distribution of accumulated profits (reserves); and

- Adjustment of partners capitals.

Question 5.

Why it is necessary to ascertain new profit sharing ratio even for old partners when a new partner is admitted?

Answer:

When new partner is admitted he acquires his share in the profits from the old partners. In other words, on the admission of a new partner, the old partners sacrifice a share of their profit in favour of the new partner. But, what will be the share of new partner and how he will acquire it from the existing partners is decided mutually among the old partners and the new partner.

On admission of a new partner, the profit sharing ratio among the old partners will change . keeping in view their, respective contribution to the profit sharing ratio of the incoming partner. Hence, there is a need to ascertain the new profit sharing ratio among all the partners.

Question 6.

What are the different ways in which a partner can retire from the firm.

Answer:

The partner retire from the business for money reasons they are

- Insolvency

- Because of age factor

- Not interested to continue

- All other partner decided

Karnataka 2nd PUC Supplementary Study Material

| Karnataka 2nd PUC Supplementary Study Material Free | |

| Karnataka 2nd PUC Previous Year Question Papers | Karnataka 2nd PUC Question Bank |

| Karnataka 2nd PUC Model Paper | Karnataka 2nd PUC Textbooks |

| Karnataka 2nd PUC Syllabus | |

Question 7.

Write the various matters that need adjustments at the time of retirement of a partners.

Answer:

The various accounting aspects involved on retirement or death of a partner are as follows:

- Ascertainment of new profit sharing ratio and gaining ratio;

- Treatment of goodwill;

- Revaluation of assets and liabilities;

- Adjustment in respect of unrecorded assets and liabilities;

- Distribution of accumulated profits and losses;

- Ascertainment of share of profit or loss up to the date of retirement/death;

- Adjustment of capital, if required;

- Settlement of the amounts due to retired/deceased partner;

Question 8.

Why do firm reyaiuate assets and reassers their liabilities on retirement or on the event of death of a partner.

Answer:

At the time of retirement or death of a partner there may be some assets which may not have been shown at their current values. Similarly, there may be certain liabilities which have been shown at a value different from the obligation to be met by the firm. Not only that, there may be some unrecorded assets and liabilities which need to be brought into books.

As learnt in case of admission of a partner, a Revaluation Account is prepared in order to ascertain net gain (loss) on revaluation of assets and/or liabilities and bringing unrecorded items into firm’s books and the same is transferred to the capital account of all partners including retiring/deceased partners in their old profit sharing ratio.

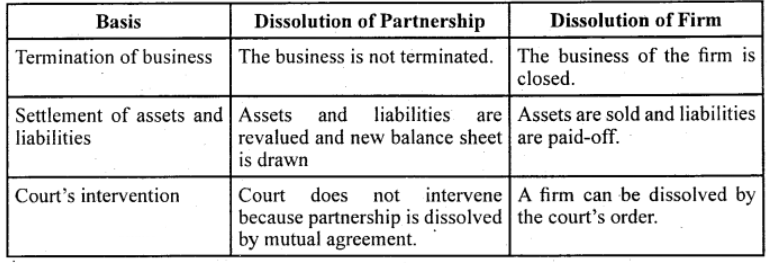

Question 9.

State the difference between dissolution of partnership and dissolution of partnership firm.

Answer:

Question 10.

State the accounting treatment for:

1. Unrecorded assets

2. Unrecorded liabilities

Answer:

For realisation of any unrecorded assets including goodwill, if any

Bank A/c Dr.

To Realisation A/c

10. For settlement of any unrecorded liability Realisation A/c Dr.

To Bank A/c

Question 11.

What is public company?

Answer:

A public company is defined as a company that offers a part of its ownership in the form of

shares, debentures, bonds, securities to the general public through stock market.

Question 12.

What is private limited company.

Answer:

As defined by the Section 3 (1) (iii) of Companies Act 1956, private limited company is ; defined by the following characteristics:

- It restricts the right to transfer its shares.

- There must be at least two and a maximum of 50 members (excluding current and former employees) to form a private company.

- It cannot invite application from the general public to subscribe its shares, or debentures.

- It cannot invite or accept deposits from persons other than its members, Directors and their relatives.

Question 13.

Define Government Company?

Answer:

As per the Section 617 of Company Act of 1956, a Government Company means any company in which not less than 51% of the paid up share capital is held by the Central Government, or by any State Government or Governments, or partly the Central Government and partly by one or more State Governments and includes a company which is a subsidiary of a Government Company as thus defined.

Question 14.

What is meant by a Debenture?

Answer:

The word Debenture is derived from a Latin word ‘debere’ which means to borrow. A debenture is issued in the form of a certificate under the seal of a company and containing a contract for the repayment of the principal sum after a fixed period of time and payment of interest at regular intervals, generally half yearly. Debentures are issued by a company for acquiring long-term borrowings.

Question 15.

What does a Bearer Debenture mean?

Answer:

When a company does not maintain any record of the debenture holders and the debenture is transferable mere by delivery, then the type of the debenture held by the holders is termed as Bearer Debenture. Interests on such debentures are paid to the persons who produce the interest coupons that are attached with these debentures in a specified bank.

Question 16.

State the meaning of ‘Debentures issued as a Collateral Security’.

Answer:

The term collateral security means additional or secondary security in addition to the primary security. Sometimes, when a company takes loan from a financial institution, then besides the primary security, the company may issue debenture for additional security (as collateral security). The lender who receives debenture as collateral security is not entitled for interest on these debentures.

Question 17.

What is meant by ‘Issue of debentures for Consideration other than Cash?

Answer:

If a company purchases assets from its suppliers or vendors, then instead of paying them in cash the company issues debentures to them. This is known as issue of debenture for consideration other than cash. The issue of debenture for consideration other than cash serves the purpose of both the vendor as well as of the purchaser (company).

Question 18.

What is public company?

Answer:

A public company is defined as a company that offers a part of its ownership in the form of shares, debentures, bonds, securities to the general public through stock market:

Question 19.

What is private limited company?

Answer:

As defined by the Section 3. (1) (iii) of Companies Act 1956, private limited company is defined by the following characteristics:

- It restricts the right to transfer its shares.

- There must be at least two and a maximum of 50 members (excluding current and former employees) to form a private company.

- It ca not invite application from the general public to subscribe its shares, or debentures.

- It cannot invite or accept deposits from persons other than its members, Directors and their relatives.

Question 20.

Define Government Company?

Answer:

As per the Section 617 of Company Act of 1956, a Government Company means any company in which not less than 51% of the paid up share capital is held by the Central Government, or by any State Government or Governments, or partly the Central Government and partly by one or more State Governments and includes a company which is a subsidiary of a Government Company as thus defined.

Question 21.

List the techniques of Financial Statement Analysis.

Answer:

The following are the commonly used techniques of Financial Statement analysis:

- Comparative Financial Statements

- Common Size Financial Statements

- Trend Analysis

- Ratio Analysis

- Cash Flow Statement

- Fund Flow Statement

Question 22.

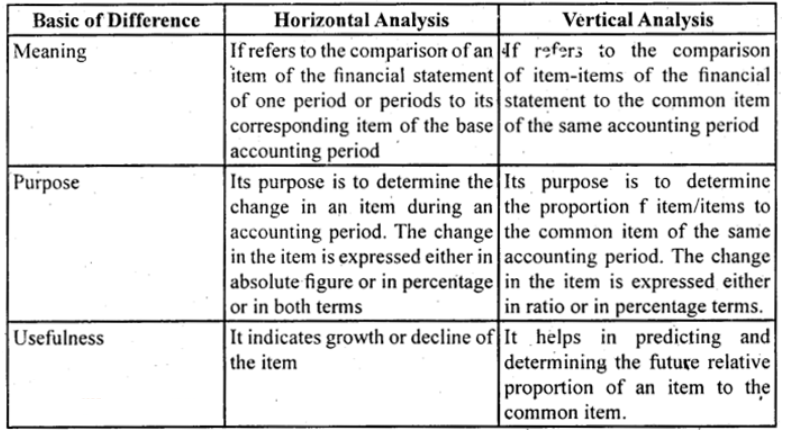

Distinguish between Vertical and Horizontal Analysis of financial data.

Answer:

Question 23.

What are Comparative Financial Statements?

Answer:

Those financial statements that enable intra-firm and inter-firm comparisons of financial statements over a period of time are called Comparative Financial Statements. In other words, these statements help the accounting users to evaluate and assess the financial progress in the relative terms. These statements express the absolute figures, absolute change and the percentage change in the financial items over a period of time.

Question 24.

What do you mean by Common Size Statements?

Answer:

These statements depict the relationship between various items of financial statements and some common items in percentage terms. In other words, various items of Trading and Profit and Loss Account such as Cost of Goods Sold, Non-Operating Incomes and Expenses are expressed in terms of percentage of Net Sales. On the other hand, different items of Balance Sheet such as Fixed Assets, Current Assets, Share Capital etc. are expressed in terms of percentage of Total of Balance Sheet. These percentage figures are easily comparable with that of the previous years’ and with that of the figures of other firms in the same industry as well.

Question 25.

What do you mean by Ratio Analysis?

Answer:

Ratio Analysis is a technique of financial analysis. It describes the relationship between various items of Balance Sheet and Income Statements. It helps us in ascertaining profitability, operational efficiency, solvency, etc. of a firm. It may be expressed as a fraction, proportion, percentage and in times. It enables budgetary controls by assessing qualitative relationship among different financial variables.

Ratio Analysis provides vital information to various accounting users regarding the financial position and viability and performance of a firm. It also lays down the basic framework for decision making and policy designing by management.

Question 26.

What are the various types of ratios?

Answer:

Accounting ratios are classified in the following two ways.

1. Traditional Classification: This classification is based on the financial statements, i.e. profit and Loss Account and Balance Sheet. The Traditional Classification further bifurcates accounting ratios as:

(a) Income Statement Ratios: These are those ratios whose all the elements belong only to the Trading and Profit and Loss Account, like Gross Profit Ratio, etc.

(b) Balance Sheet Ratios: These are those ratios whose all the elements belong only to the Balance Sheet, like Current Ratio, Debt Equity Ratio, etc,

(c) Composite Ratios: These are those ratios whose elements belong both to the Trading and Profit and Loss Account as well as to the Balance Sheet, like Debtors Turnover Ratio, etc.

2. Functional Classification: This classification reflects the functional need and the purpose of calculating ratio. The basic rationale to compute ratio is to ascertain liquidity, solvency, financial performance and profitability of a business. Consequently, the Functional Classification classifies various accounting ratios as:

(a) Liquidity Ratio: These ratios are calculated to determine short term solvency.

(b) Solvency Ratio: These ratios are calculated to determine long term solvency.

(c) Activity Ratio: These ratios are calculated for measuring the operational efficiency and efficacy of the operations. These ratios relate to sales or cost of goods sold.

(d) Profitability Ratio: These ratios are calculated to assess the financial performance and the financial viability of the business.

Question 27.

What relationships will be established to study?

(a) Inventory Turnover

(b) color Turnover

(c) Payables Turnover

(d) king Capital Turnover

Answer:

(a) Inventory Turnover Ratio: This ratio is cc puted to determine the efficiency with which the stock is used. This ratio is b; scd on the relationship between cost of goods sold and average stock kept during the year

Question 28.

Why would the inventory turnover ratio be more important when analysing a grocery store than an insurance company?

Answer:

Grocery store is a trading concern and involved in business of buying and selling of grocery. It keeps stock of various groceries to meet the requirement of the customers and it should calculate the inventory turnover ratio. Hence, this ratio is more important for a grocery store then it is for an insurance company as the latter does not need to maintain any stock of goods sold. The insurance company is engaged in delivering service that is intangible and, thus, cannot be stored.

Question 29.

What is a Cash Flow Statement?

Answer:

A Cash Flow Statement is a statement showing inflows and outflows of cash and cash equivalents from operating, investing and financing activities of a company during a particular period. It explains the reasons of receipts and payments in cash and change in cash balances during an accounting year in a company.

Question 30.

How are the various activities classified (as per AS-3 revised) while preparing cash flow statement?

Answer:

As per the Revised Accounting Standard 3 (AS-3), preparation of Cash Flow

Statement for each period is mandatory. AS-3 also specifies the classification of all inflows and outflows basically under the following heads:

- Cash Flow from Operating Activities

- Cash Flow from Investing Activities

- Cash Flow from Financing Activities

Question 1.

Explain the statement: “Receipt and Payment Account is a summarised version of Cash Book”.

Answer.

It is prepared at the end of the accounting year on the basis of cash receipts and cash payments recorded in the cash book. It simply is a summary of cash and bank transactions under various heads. Receipt and Payment Account gives summarised picture of various receipts and payments, irrespective of whether they pertain to the current period, previous period or succeeding period or whether they are of capital or revenue nature. It may be noted that this account does not show any non-item like depreciation.

The opening balance in Receipt and Payment Account represents cash in hand/ cash at bank which is shown on its receipts side, and the closing balance of this account represents cash in hand and bank balance as at the end of the year, which appear on the credit side of the Receipt and Payment Account.

Question 2.

“Income and Expenditure Account of a Not-for-Profit Organisation is akin to Profit and Loss Account, of a business concern”. Explain the statement.

Answer:

It is the summary of income and expenditure for the accounting year. It is just like a profit and loss account prepared on accrual basis in case of the business organisations. It includes only revenue items and the balance at the end represents surplus or deficit. The Income and Expenditure Account serves the same purpose as the profit and loss account of a business organisation does.

Question 3.

Distinguish between Receipts and Payments Account and Income and Expenditure Account.

Answer:

| Receipts and Payments A/c | Income and Expenditure A/c |

| (i) It is a real account. | (i) It is a nominal account. |

| (ii) It is prepared from the cash book. | (ii) It is prepared from the receipts and payments and other information. |

| (iii) It is on the basis of actuals Receipts and Payments and not considered accruals. | (iii) In this statement accruals of Receipts and Payments considered. |

| (iv) The different treated as cash balance or bank balance. | (iv) The different treated as profit or deficit for the year. |

Question 4.

Show the treatment of the following items by a not-for-profit organization:

(i) Annual subscription

(ii) Specific Donation

(iii) Sale of Fixed Assets

(iv) Sale of old periodicals

(v) Sale of Sports Materials

(vi) Life Membership Fee

Answer:

(i) Annual subscription :

- Actual subscription received during an accounting year are shown on debit side of receipts and payment a/c.

- Later subscription transfered to income and expenditure account to the extent of current year amount. Such transfer shown on credit side of inc.ome and expenditure a/c

- Subscription received, which is related to previous year should deducted from balance sheet assets side amount shown.

- Subscription received for next year should be shown an balance sheet liabilities side as received in advance.

- Subscription due but not received should be added to subscription received on income and expenditure a/c credit side and the same to be shown on assets side of the balance sheet under‘Receivables or amount due but not received’.

(ii) Specific donation – The fund received for specific purpose From the donors called special funds or special donation. The accounting treatment of special donation:-

- Amount received as specific donation should be shown on receipts side or debit side of receipts and

- Specific donation capital receipts in its nature so it should be shown on balance sheet liability side.

- Any payment made for that specific purpose to that extent should deduct from balance of amount shown in previous year balance sheet.

- Any amount received during the year should added to previous year balance amount.

(iii) Sale of fixed assets – The assets in the business should be sale for many reasons. In case of such sales doing the year, the accounting treatment is as follows.

- Sale of assets is the receipt such receipt should be shown on debit side of receipt and payment a/c.

- Sale of assets receipt is a capital receipt. The book value should be deducted from the existing assets balance.

- In case of any loss on sale of fixed assets should be debited to income and expenditure account. Any profit on sale of fixed assets. Shown on credit side of income and expenditure a/c.

(iv) Sale of old periodicals

- The-receipt out of sale of newspaper and periodicals should be shown oh debit side of receipt and payment a/c

- Sale of newspaper and periodicals is the revenue, it should be transfer to income and expenditure a/c credit side as income.

(v) Sale of sports materials – Sale of sports materials dr items are’ capital receipts. The accounting treatment is as treatment of sale of fixed assets. Sports materials is a part of fixed assets.

(vi) Life membership fee:

- The person normally paid fees to the organization foe the intention to become life member of the organization. It is the revenue of the organization, shown an debit side of receipt and payment a/c.

- Life membership fees is the capital receipt in its nature. These fees amount are added to the capital fund on the liability side of the balance sheet.

Question 5.

What is partnership? What are its chief characteristics? Explain.

Answer:

Any association of two or more persons who carry on a business jointly with the intention of sharing Profit / Loss is called “Partnership”.

- Two or More Persons: In order to form partnership, there should be at least two persons coming together for a common goal.

- Agreement: Partnership is the result of an agreement between two or more persons to do business and share its profits and losses.

- Business: The agreement should be to carry on some business. Mere co-ownership of a property does not amount to partnership.

- Mutual Agency: The business of a partnership concern may be carried on by all the partners or any of them acting for all.

- Sharing of Profit: Another important element of partnership is that, the agreement between partners must be to share profits and losses of a business.

- Liability of Partnership: Each partner is liable jointly with all the other partners and also severally to the third party for all the acts of the firm done while he is a partner.

Question 6.

Discuss the main provisions of the Indian Partnership Act 1932 that are relevant to partnership accounts if there is no partnership deed.

Answer:

The important provisions affecting partnership accounts are as follows:

(a) Profit Sharing Ratio: If the partnership deed is silent about the profit sharing ratio, the profits and losses of the firm are to be shared equally by partners, irrespective of their capital contribution in the firm.

(b) Interest on Capital: No partner is entitled to claim any interest on the amount of capital contributed by him in the firm as a matter of right. However, interest can be allowed when it is expressly agreed to by the partners. Thus, no interest on capital is payable if the partnership deed is silent on the issue. In case the deed provides for payment of interest on capital but does not specify the rate, the interest will be paid at the rate of 6 per cent per annum. Further the interest is payable only out of the profits of the business and not if the firm incurs losses during the period.

(c) Interest on Drawings: No interes. is to be charged on the drawings made by the partners, if there is no mention in the Deed.

(d) Interest on Advances: If any partner has advanced some money to the firm beyond the amount of his capital for the purpose of business, he shall be entitled to get an interest on the amount at the rate of 6 per cent per annum.

(e) Remuneration for Firm’s Work: No partner is entitled to get salary or other remuneration for taking’-part in the conduct of the business of the. firm unless there is a provision for the same in the Partnership.Deed.

Question 7.

Explain why it is considered better to make a partnership agreement in writing.

Answer:

Normally the partner is admitted for the needs of additional capital and managerial help. When a partner is admitted the financial structure also changes. Some times all old partners may decided to have their capital in proportion of new profit sharing ratio. If they decided as per new ratio, then capital should be adjusted. The partner may bring the cash or excess capital may be withdrawn. But this changes not effected to new partner based on new partner share the old partners capital adjusted.

Example : A and B are partners sharing equally their capital before admitting a new partner, stood at and 30,000 and 20,000.

They agreed to admit Mv-C for 1 /3 share of future profit and has to bring ₹ 25,000 as capital. The new profit sharing ratio is 1 : 1 : 1. The old partner decided to adjust the capital as per new profit sharing ratio.

In this case – the new partner brings capital of ₹ 25,000 where as MvA’s capital is 30,000 and Mv. B’s capital is 20,000. Hence Mv. A has to withdraw ₹ 5,000 from the business and Mr. B has to bring ₹ 5000 to the business.

Question 8.

Explain various methods of valuation of goodwill.

Answer:

Goodwill is an intangible asset it is very difficult to accurately calculate its value. Various methods have been advocated for the valuation of goodwill of a partnership firm, Goodwill calculated by one method may differ from the goodwill.

Calculated by another method. Hence, the method by which goodwill is to be calculated, may be specifically decided between the existing partners and the incoming partner.

The important methods of valuation of goodwill are as follows:

- Average Profits Method.

- Supper Profits Method

- Capitalisation Method

1. Average Profits Method: Under this method, the goodwill is valued at agreed number of . ‘years’ purchase of the average profits of the past few years. It is based on the assumption that a new business will not be able to earn any profits during the first few years of its operations.

2. Supper Profits Method : The basic assumption in the average profits (simple or weighted) method of calculating goodwill is that if a new business is set up, it will not be able to earn any profits during the first few years of its operations. Hence, the person who purchases an existing business has to pay in the form of goodwill a sum equal to the total profits he is likely to receive for the first‘few years’.

(a) by capitalizing the average profits, or

(b) by capitalizing the super profits.

(a) Capitalisation of Average Profits: Under this method, the value of goodwill is ascertained by deducting the actual capital employed (net assets) in the business from the capitalized value of the average profits on the basis of normal rate of return. This involves the following steps:

- Ascertain the average profits based on the past few years’ performance.

- Capitalize the average profits on the basis of the normal rate of return to ascertain the capitalised value of average profits as follows:

Average Profits × 100/Normal Rate of Return - Ascertain the actual capital employed (net assets) by deducting outside liabilities from the total assets (excluding goodwill).

Capital Employed = Total Assets (excluding goodwill) – Outside Liabilities - Compute the value of goodwill by deducting net assets from the capitalised value of average profits, i.e. (2) – (3).

Question 9.

How will you compute the amount payable to a deceased partner?

Answer:

The sum due to the retiring partner (in case of retirement) and to the legal representatives/ executors (in case of death) includes:

- credit balance of his capital account;

- credit balance of his current account(if any);

- his share of goodwill ;

- his share of accumulated profits (reserves);

- his share in the gain of revaluation of assets and liabilities;

- his share of profits up to the date of retirement/death;

- interest on his capital, if involved, up to the date of retirement/death; and

- salary/commission, if any, due to him up to the date of retirement/death.

The following deductions, if any, may have to be made from his share:

- debit balance of his current account(if any);

- his share of goodwill to be written off; if necessary;

- his share of accumulated losses;

- his share of loss on revaluation of assets and liabilities;

- his share of loss up to the date of retirement/death;

- his drawings up to the date of retirement/death;

- interest on drawings, if involved, up to the date of retirement/death.

Question 10.

Explain the treatment of goodwill at the time of retirement or on the event of death of a partner?

Answer:

The retiring or deceased partner is entitled to his share of goodwill at the time of retirement/ death because the goodwill has been earned by the firm with the efforts of all the existing partners. Hence, at the time of retirement/death of a partner, goodwill is valued as per agreement among the partners the retiring/ deceased partner compensated for his share of goodwill by the continuing partners (who have gained due to acquisition of share of profit from the retiring/ deceased partner) in their gaining ratio.

When goodwill does not appear in the books of the firm there are four ways in which the . retiring partner can be given the necessary credit for loss of his share of goodwill, these are as follows:

(a) Goodwill is raised at its full value and retained in the books as such: In this case, Goodwill Account is debited will its full value and all the partner’s (including the retired/deceased partner) capital accounts are credited in the old profit sharing ratio. The full value of goodwill will appear in the balance sheet of the reconstituted firm.

(b) Goodwill is raised at it’s full value and written off immediately: If it decided that goodwill should not be refrained and shown in the balance sheet of the reconstituted firm then, after raising goodwill at its value by crediting all the partners’ capital accounts (including that of the retired/ deceased partners, it should be written off by debiting the remaining partners in their new profit sharing ratio and crediting the goodwill account with its full value.

(c) Goodwill is raised to the extent of retired/deceased partner’s share and written off immediately: In this case goodwill account is raised only to the extent of retired/ deceased partner’s share by debiting goodwill account with the proportionate amount and credited only to the retired/deceased partner’s capital account. Thereafter, the remaining partners capital accounts are debited in their gaining ratio and goodwill account/credited to write it off.

(d) No goodwill account is raised at all in firm’s books: If it is decided that the goodwill account should not appear in firm’s books at all, in that case it is adjusted discretely, through partners capital accounts.

If value of goodwill already appearing in the books of the firm equals with the current value of goodwill, normally no adjustment is required because goodwill stands credited in the accounts of all the partners including the retiring one.

It may be noted that in all the above situations, goodwill appears in the balance sheet at its full value. In case it is decided by the partners that it should be written-off, fully or partially.

Hidden Goodwill: If the firm has agreed to settle the retiring or deceased partner by paying him a lump sum amount, then the amount paid to him in excess of what is due to him based on the balance in his capital account after making necessary adjustments in respect of accumulated profits and losses and revaluation of assets and liabilities, etc. shall be treated as his share of goodwill (known as hidden goodwill).

Question 11.

Discuss the various methods of computing the share in profits in the event of death of a partners.

Answer:

The accounting treatment in the event of death of a partner is similar to that in case of retirement of a partner, and that in case of death of a partner his claim is transferred to his executors and settled in the same manner as that of the retired partner. However, there is one major difference that, while the retirement normally takes place at the end of an accounting period, the death of a partner may occur any time.

Hence, in case of a death, his claim shall also include his share of profit or loss, interest on capital, interest on drawings (if any) from the date of the last Balance Sheet to the date of his death of these, the main problem relates to the calculation of profit for the intervening period (i.e., the period from date of the last balance sheet and the date of the partner’s death.

Since, it is considered cumbersome to close the books and prepare final account, for the period, the deceased partner’s share of profit may be calculated on the basis of last year’s profit (or average of past few years) or on the basis of sales.

Question 12.

What is meant by dissolution of partnership firm?

Answer:

Dissolution of a partnership firm may take place without the intervention of court or by the order of a court, in any of the ways specified later in this section.

It may be noted that dissolution of the firm necessarily brings in dissolution of the partnership. Dissolution of a firm takes place in any of the following ways:

1. Dissolution by Agreement: A firm is dissolved :

(a) with the consent of all the partners or

(b) in accordance with a contract between the partners.

2. Compulsory Dissolution: A firm is dissolved compulsorily in the following cases:

(a) when all the partners or all but one partner, become insolvent, rendering them incompetent to sign a contract;

(b) when the business of the firm becomes illegal; or

(c) when some event has taken place which makes it unlawful for the partners to carry on the business of the firm in partnership, e.g., when a partner who is a citizen of a countiy becomes an alien enemy because of the declaration of war with his countiy and India.

3. On the happening of certain contingencies: Subject to contract between the partners, a firm is dissolved :

(a) if constituted for a fixed term, by the expiry of that term;

(b) if constituted to carry out one or more ventures, by the completion thereof;

(c) by the death of a partner;

(d) by the adjudication of a partner as an insolvent.

4. Dissolution by Notice: In case of partnership at will, the firm may be dissolved if any one of the partners gives a notice in writing to the other partners, signifying his intention of seeking dissolution of the firm.

5. Dissolution by Court: At the suit of a partner, the court may order a partnership firm to be dissolved on any of the following grounds:

(a) when a partner becomes insane;

(b) when a partner becomes permanently incapable of performing his duties as a partner;

(c) when a partner is guilty of misconduct which is likely to adversely affect the business of the firm;

(d) when a partner persistently commits breach of partnership agreement;

(e) when a partner has transferred the whole of his interest in the firm to a third party;

(f) when the business of the firm cannot be carried on except at a loss; or

(g) when, on any ground, the court regards dissolution to be just and equitable.

Question 13.

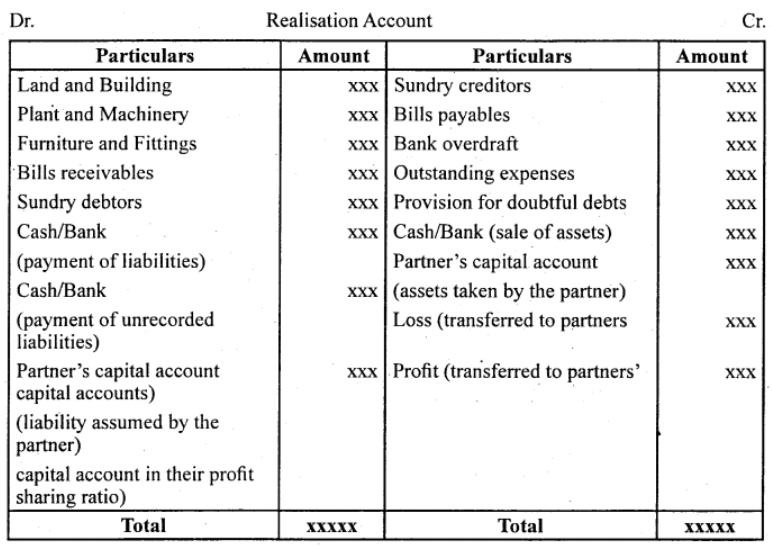

Reproduce the format of Realisation Account.

Answer:

Question 14.

How deficiency of Crditors is paid off?

Answer:

For settlement with the creditor through transfer of assets when a creditor accepts an asset in full and final settlement of his account, journal entry needs to be recorded. But, if the creditor accepts an asset only as part payment of his/her dues, the entry will be made for cash payment only. For example, a creditor to whom ₹ 10,000 was due accepts office equipment worth ₹ 8,000 and is paid ₹ 2,000 in cash, the following entry shall be made for the payment of ₹ 2,000 only.

Realisation A/c Dr.

To Bank A/c

However, when a creditor accepts an asset whose value is more than the amount due to him, he/she will pay cash to the frim for the difference for which the entry will be:

BankA/c Dr.

To Realisation A/c

For payment of realisation expenses

(a) When some expenses are incurred and paid by the firm in the process of realisation of assets and payment of liabilities:

Realisation A/c Dr.

To Bank A/c

Question 15.

What is meant by the word‘Company? Describe its characteristics.

Answer:

The Section 3 (1) (i) of the Company Act of 1956 defines an organisation as a company that is formed and registered under the Act or any existing company that is formed and registered under any earlier company laws. In general, a company is an artificial person, created by law that has a separate legal entity, perpetual succession, common seal and has limited liability.

1. Association of Person: A company is formed Voluntarily by a group of persons to perform a common business. Minimum number of person should be two for formation of a private company and seven for a public company.

2. Artificial Person: Company is an artificial and juristic person that is created by law.

3. Separate Legal Entity: A company has a separate legal entity from its members

(shareholders) and Directors. It can open a bank account, sign a contract and can own a property in its own name. ‘

4. Limited Liability: The liability of the members of a company is limited up to the nominal value or the face value of the shares. Unlike a partnership firm, on insolvency of a company, the members and the shareholders are not liable to pay the amount due to the creditors of the company. In fact, the members and the shareholders are only liable to pay the unpaid amount of the shares held by them.

5. Perpetual Existence: The existence of company is not affected by the death, retirement, and insolvency of its members. That is, the life of a company remains unaffected by the life and the tenure of its members in the company. The life of a company is infinite until it is properly wound up as per the Company Act.

6. Common Seal: The Company is an artificial person ‘and has no physical existence hence it cannot put its signature. Thus, the Common Seal acts as an official signature of a company that validates the official documents.

7. Transferability of Shares: The shares of public limited company are easily and freely transferable without any consent from other members. But the share of ownership of a private limited company is not transferable without the consent of the other members.

Question 16.

What is a preference Share’? Describe the different types of preference shares.

Answer:

Preference Shares: Section 85 of the Company Act, 1956 defines Preference Shares to be featured by the following rights:

- Preference Shares entitle its holder the right to receive dividend at a fixed rate or fixed amount.

- Preference Shares entitle its holder the preferential right to receive repayment of capital invested by them before their equity counterparts at the time of winding up of the company.

Types of Preference Shares

1. Cumulative Preference Shares: When a preference shareholder has a right to recover any arrears of dividend, before any dividend is paid to the equity shareholders, then the type of Preference Shares held by the shareholder is known as Cumulative Preference Shares.

2. Non-Cumulative Preference Share: When a preference shareholder receives dividend only in case of profit and is not entitled any right to recover the arrears of dividend, then the type of Preference Shares held by the shareholder is known as Non-Cumulative Preference Shares.

3. Participating Preference Share When a preference shareholder enjoys the right to participate in the surplus profit (in addition to the fixed rate of dividend) that is left after the payment of dividend to the equity shareholders, the type of shares held by the shareholder is known as Participating Preference Share.

4. Non-participating Preference Share: When a preference shareholder receives only a fixed rate of dividend every year and do not enjoy the additional participation in the surplus profit, then the type of shares held by the shareholder is known as Non¬Participating Preference Shares.

5. Redeemable preference share: When a preference shareholder is repaid by the company after a certain specified period in accordance with the term specified in the Section 80 of Company Act of 1956, then the type of the shares held by him/her is known as Redeemable Preference Shares.

6. Non-Redeemable Preference share: These shares are not repaid by the company during its lifetime. As per the Section 80A of the Company Act of 1956, no company can issue Non-Redeemable Preference Shares. It is merely a theoretical concept.

7. Convertible Preference Share: The shareholders holding Convertible Preference Shares have a right to convert his/her shares into equity shares.

8. Non-Convertible Preference Share: Unlike Convertible Preference Shares, the shareholders holding Non-Convertible Preference Shares do not enjoy the right to convert their shares into equity shares.

Question 17.

What is meant by a debenture? Explain the different types of debentures?

Answer:

The word Debenture is derived from a Latin word ‘debere’ which means to borrow. A debenture is issued in the form of a certificate under the seal of a company and containing a contract for the repayment of the principal sum after a fixed period of time and payment of interest at regular intervals, generally half yearly. Debentures are issued by a company for acquiring long-term borrowings.

Types of Debenture:

- Redeemable Debentures: The debentures which are repayable on a specified date are called redeemable debentures.

- Irredeemable Debentures: If there is no fixed time by which the company is bound to pay back the money then it is known as irredeemable debentures. These debentures are also called perpetual debentures.

- Convertible Debentures: Debentures which can be converted into equity shares after a specified period of time are known as convertible debentures.

- Non-convertible Debentures: Debentures which cannot be converted into equity shares after a specified period of time are known as non-convertible debentures.

- Secured Debentures: If debentures are issued with a charge on the assets of the company as security it is known as Secured debentures. The charge may be fixed i.e., on specified asset, or it may be floating. Secured debentures are also known as mortgaged debentures.

- Unsecured Debentures: if debentures are issued with merely a promise of payment without having any charge on any assets as security is known as, unsecured debentures.

So these debentures are also known as naked or simple debentures. - Registered Debentures: Registered debentures are those which are duly recorded in the register of debenture holders maintained by the company. These can be transferred only through a regular transfer deed.

- Bearer Debentures: Bearer debentures are those which are not recorded in the register of debenture holders maintained by the company.

Question 18.

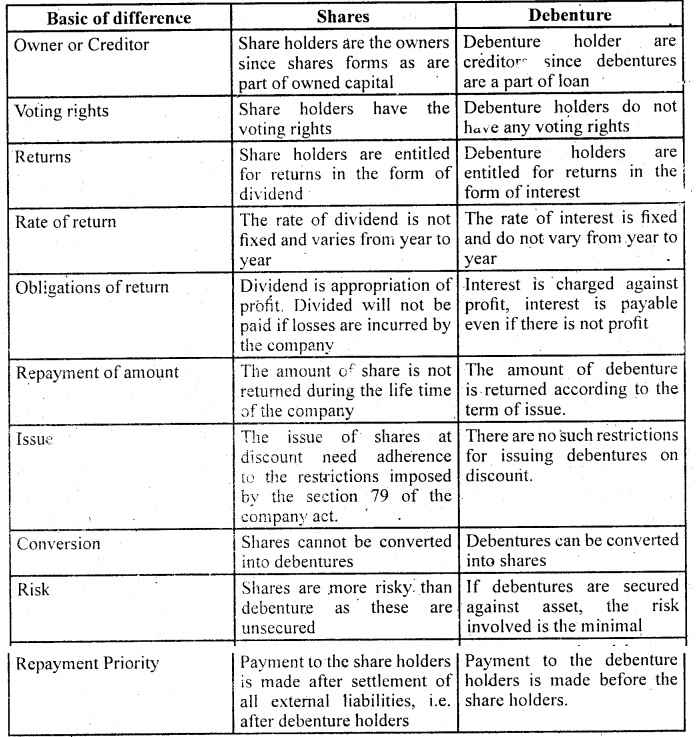

Distinguish between a debenture and a share. Why is debenture known as loan capital? Explain.

Answer:

Issue of debentures implies incurring long-term indebtedness. Generally, a company issues debentures for acquiring long-term borrowings to achieve its long-run targets and growth. Like the owner’s capital, interest is also payable on the principal amount of the debenture. The interest paid is regarded as an expense for the company and is deductible under Income Tax Act. Therefore, debentures are also known as loan capital because they are redeemable after a long period of time.

Question 19.

Describe the different techniques of financial analysis and explain the limitations of financial analysis.

Answer:

The various techniques used in financial analysis are as follows:

Comparative Statements: These statements depict the figures of two or more accounting years simultaneously that help to access the profitability and financial position of a business. The Comparative Statements help us in analysing the trend of the financial position of the business. These statements also enable us to undertake various types of comparisons like inter¬firm comparisons and intra-firm comparisons. It presents the change in the financial items both in absolute as well as percentage terms. Therefore, these statements help in measuring the efficiency of the business in relative terms. The analyses based on these statements are known as Horizontal Analysis.

Common Size Statements: These statements depict the relationship between various items of financial statements and some common items (like Net Sales and the Total of Balance Sheet) in percentage terms. In other words, various items of Trading and Profit and Loss Account such as Cost of Goods Sold, Non-Operating Incomes and Expenses are expressed in terms of percentage ofNet Sales. On the other hand, different items of Balance Sheet such as Fixed Assets,

Current Assets, Share Capital, etc. are expressed in terms of percentage of Total of Balance Sheet. These percentage figures are easily comparable with that of the previous years’ (i.e. inter-firm comparison) and with that of the figures of other firms in the same industry (i.e. inter-firm comparison) as well. The analyses based on these statements are commonly known as Vertical Analysis.

Trend Analysis: This analysis undertakes the study of trend in the financial positions and the operating performance of a business over a series of successive years. In this technique, a particular year is assumed to be the base year and the figures of all other years are expressed in percentage terms of the base year’s figures. These trends (or the percentage figures) not only helps in assessing the operational efficiency and the financial position of the business but also helps in detecting the problems and inefficiencies.

Ratio Analysis: This technique depicts the relationship between various items of Balance Sheet and the Income Statements. It helps in ascertaining the profitability, operational efficiency, solvency, etc of a firm.. The analysis expresses financial items in terms of percentage, fraction, proportion and as number of times. It enables budgetary controls by assessing the qualitative relationship among different financial variables. This analysis provides vital information to different accounting users regarding the financial position, viability and performance of a firm. It also facilitates decision making and policy designing process.

Cash Flow Analysis: This analysis is presented in the form of a statement showing inflows and outflows of cash and cash equivalents from operating, investing and financing activities of a company during a particular period of time. It helps in analysing the reasons of receipts and payments in cash and change in the cash balances during an accounting year in a company.

Limitations of Financial Analysis

The limitations of Financial Analysis are:

Ignores Changes in the Price level: The financial analysis fails to capture the change in price level. The figures of different years are taken on nominal values and not in real terms (i.e. not taking price change into considerations).

Misleading and Wrong Information: The financial analysis fails to reveal the change in the accounting procedures and practices. Consequently they may provide wrong and misleading information.

Interim and Final Picture: The financial analysis presents only the interim report and ‘ thereby provides incomplete information. They fail to provide the final and holistic picture.

Ignores Qualitative and Non-monetary Aspects: The financial analysis reveals only the monetary aspects. In other words, these analyses consider only that information that can be expressed only in monetary terms. These analyses fail to disclose managerial efficiency, growth prospects, and other non-operational efficiency of a business.

Accounting Concepts and Conventions: The financial analysis are based an accounting concepts and conventions. Therefore, the analysis and conclusions based on such analyses may not be reliable. For example, the analysis considers only the book-value of various items (i.e. according to the Going Concept) and consequently ignores the present market value of those items. Hence, the analysis may not be realistic.

Involves Personal Biasness: The financial analysis reflects the personal biasness and personal value judgments of the accountants and clerks involved. There are different techniques used by different personnel for charging depreciation (original cost or written-down value method) and also for inventory valuation. The use of different techniques by different people reduces the effectiveness of the financial analysis.

Unsuitable for Comparisons: Due to the involvement of personal value judgment, personal biasness and use of different techniques by different accountant, various types of comparisons such as inter-firm and intra-firm comparisons may not be possible and reliable.

Question 20.

Describe the procedure to prepare Cash Flow Statement.

Answer:

The procedure to prepare Cash Flow Statement is described in the following steps in their chronological order. ‘

Step 1: Ascertain the cash flows from operating activities

Step 2: Ascertain the cash flows from investing activities

Step 3: Ascertain the cash flows from financing activities

Step 4: Ascertain net increase or decrease by summing up the amounts of Steps 1, 2, and 3.

Step 5: Write the opening balance of cash and cash equivalents and deduct it from the amount ascertained in Step 4. The resulting figure arrived is the Closing Balance of Cash and Cash Equivalents.

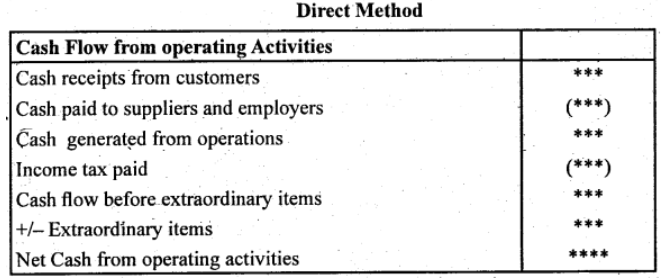

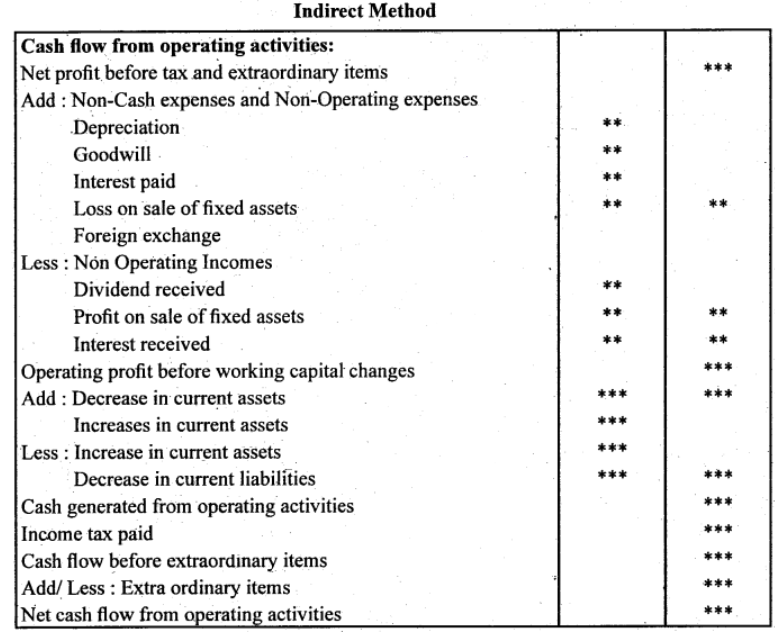

Describe ‘Direct’ and ‘Indirect’ methods of ascertaining Cash Flow from Operating Activities.

As per the Accounting Standard 3 issued by the Institute of Chartered

Accountant of India, an enterprise should report cash flows from operating activities Using either of the following methods:

Direct Method: It represents the cash receipts from debtors (customers) and customers and cash payments to creditors (sellers) and employees. It assists in estimating future cash flows. The excess of cash payments over cash.receipts is known as Net Cash Flow of Operating Activities.

Indirect Method: This method starts with the Net Profit before tax and extraordinary items. For this purpose, the Net Profit as revealed by the Profit and Loss Account cannot be taken into consideration as there exists some items which do not leads to outflow of cash. The following are those items that need to be added back to the Net Profit of the Profit and Loss Account.

Quiz

Quiz