-

Question 1

5 / -1

Very small Not-for-Profit Organizations (NPOs) prepare only ______

Solution

The correct answer is receipts and payment account.

Key Points

Key Points

- Receipts and payments account is an account that shows the summary of all cash and bank transactions that occurred during an accounting period.

- It starts with the opening balances of cash and bank and ends with the closing balances of cash and bank.

- This account is a Real Account and lays the basis for the preparation of the Income and Expenditure Account and the Balance Sheet.

- Need for Receipts and payments Account:

- As most of the transactions of Not-for-Profit Organisations are for cash, the Receipts and Payments Account shows most of the items in one place.

- As it is in a summary form, it gives an idea of a large number of transactions at a glance.

- It contains accounting information under various heads. So it gives information item-wise for the accounting year.

- It shows the closing cash or/and bank balance, this cash/Bank balance is taken to the Balance Sheet.

- The Receipts and Payments Account serves the purpose of trial balance and becomes the basis of preparing financial statements i.e. Income and Expenditure Account and Balance Sheet for the organization.

- Very small Not-for-Profit Organisations (NPOs) prepare only Receipts and Payments Account.

-

Question 2

5 / -1

Statement of cash flows includes:

Solution

The correct answer is All of these.

- Cash Flows: Cash flows are inflows and outflows of cash and cash equivalent.

- It implies movement in and movement out of cash and cash equivalents.

- Receipt of cash from a non-cash item is termed as ‘cash inflow’, while cash payment in respect of such item is termed as ‘cash outflow’.

- Statement of cash flows includes Financing Activities, Operating Activities, and Investing Activities.

Additional Information

Additional Information

- In the cash flow statement, financing activities refer to the flow of cash between a business and its owners and creditors. It focuses on how the business raises capital and pays back its investors.

- Operating activities are the daily activities of a company involved in producing and selling its product, generating revenues, as well as general administrative and maintenance activities.

- Investing activities in accounting refers to the purchase and sale of long-term assets and other business investments, within a specific reporting period.

-

Question 3

5 / -1

Securities Premium can not be applied:

Solution

The correct answer is FOR PAYING DIVIDEND TO MEMBERS.

- Securities premium can not be applied for paying dividend to members.

- Securities premium can be utilised for the purposes prescribed in Section 78, which are:

- issuing full paid bonus shares

- writing off preliminary expenses

- writing off expenses such as share issue expenses, commission, discount allowed on issue of debentures.

- providing for the preliminary payable on redemption of debentures or preference shares

- in buying-back its own shares

Key Points

- Buy-back Shares: It implies the act of purchasing its own shares by a company.

- Bonus Shares: Those shares are additional shares given to the current shareholders without any additional cost, based upon the number of shares that a shareholder owns. These are the company's accumulated earnings that are not given out in the form of dividends but are converted into free shares.

- Preliminary expenses: All expenses incurred before a company is formed i.e. cost incurred before the start of business operations.

- Writing off: It is the amount which is a reduction in the recorded amount of an asset.

- Share: It is the capital of a company that is divided into units of small denominations.

- Debenture: It refers as a medium for long-term debt financing (usually 5 or more years of financing), that is used by large companies to borrow money. It is the most common type of long-term loan and thus, considered as long-term funds.

- Preference Share: These are those shares that carry preferential right as to dividend at fixed rate; and preferential right as to repayment of capital.

-

Question 4

5 / -1

A method used in a comparative analysis of financial statement is:

Solution

The correct answer is Common size analysis.

- Common size analysis also referred to as vertical analysis, is a tool that financial managers use to analyze income statements.

- It evaluates financial statements by expressing each line item as a percentage of the base amount for that period.

- The analysis helps to understand the impact of each item in the financial.

- This method used in a comparative analysis of the financial statements.

Key Points

- Returning analysis is a statistical technique used in finance to deconstruct the returns of investment strategies using a variety of explanatory variables. The model results in a strategy's exposures to asset classes or other factors interpreted as a measure of a fund or portfolio manager's style.

- Preference analysis holds a clear advantage in marketing actionability and new product creativity.

- Graphical Analysis allows us to quickly learn about the nature of the process, enables clarity of communication, and provides a focus for further analysis. It is an important tool for understanding sources of variation in the data and thereby helping to better understand the process and where root causes might be.

-

Question 5

5 / -1

Cherry join as a partner in Mango’s company. As per the partnership deed, interest on drawing is charged at 24% p.a. During the year ended 31st December 2020, he drew as follows:

Date | Rupees |

Mar-01 | 5,000 |

Jun-01 | 5,000 |

Sep-01 | 5,000 |

Dec-01 | 5,000 |

Calculate the amount of interest on drawings

Solution

Given:

Cherry’s account details are given.

Formula Used:

Simple Interest = (Principal × Rate of Interest × Time)/100

Calculation:

Money withdraw on March 1 = Rs. [5000 × 24 × (10/12)]/100 = Rs. 1000

Money withdraw on June 1 = Rs. [5000 × 24 × (7/12)]/100 = Rs. 700

Money withdraw on September 1 = Rs. [5000 × 24 × (4/12)]/100 = Rs. 400

Money withdraw on December 1 = Rs. [5000 × 24 × (1/12)]/100 = Rs. 100

Total interest on drawing the money = Rs. 1000 + Rs. 700 + Rs. 200 + Rs. 100 = Rs. 2200.

∴ The amount of interest on drawings is Rs. 2200.

-

Question 6

5 / -1

P&L statement is also known as:

Solution

The correct answer is Statement of income.

- The income statement also called a profit and loss statement is a report made by company management that shows the revenue, expenses, and net income or loss for a period.

- The income statement is one of the main four financial statements that are issued by companies: balance sheet, income statement, statement of owner’s equity, and statement of cash flows.

- Profit & Loss A/c is meant for recording all the expenses, losses, incomes, profit, and gain; to ascertain the net profit or net loss during a financial year.

Additional Information

Key Points

- Revenue: It means the amount, which as a result of operations, is added to the capital. It is an inflow of assets, which results in an increase in the owner's equity. Examples- revenue from sale of goods, rent, commission, etc.

- Income: It is the profit earned during a period of time. It is the difference between revenue and expense.

- Expense: It is the amount spent in order to produce and sell the goods and services which produce the revenue.

- Loss: It is an excess of expenses of a period over its related revenues that may arise from normal business activities.

-

Question 7

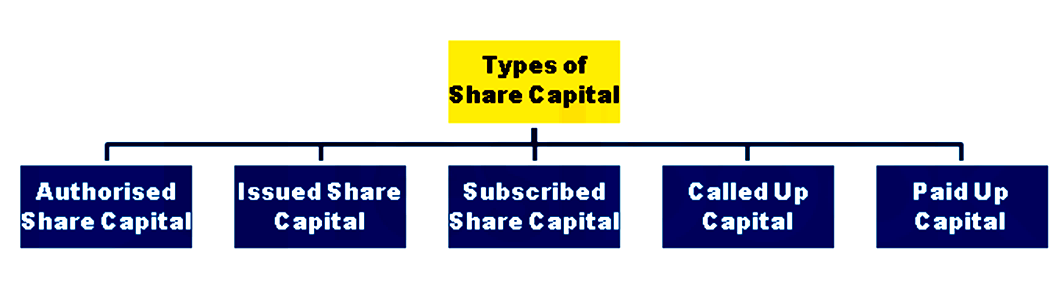

5 / -1

Subscribed Capital means capital __________ by the public

Solution

The correct answer is Actually Paid.

Key PointsSubscribed capital:

- Subscribed Capital is that capital which has actually accepted by the public.

- It is the portion of the issued capital for which the corporation has received an application.

- Example - If a company issues 16000 shares of one hundred rupees each and the public only applies for 12000, the issued capital is Rs 16 lakh and the subscribed capital is Rs 12 lakh.

-

Question 8

5 / -1

X and Y are partners sharing profit in the ratio of 3 ∶ 2 Z is admitted for 1/5 share in the firm. Z acquires his share from X and Y equally. The new profit sharing ratio of the partners will be

Solution

Key Points

Old Share of X : Y :: 3 : 2 (Given)

Z is admitted for 1/5th share.

Let the total share of the firm be 1.

Total share of X and Y after Z's admission = 1 - 1/5 = 4/5

Sacrifice made in favor of Z:

X = 1/5 x 1/2 = 1/10

Y = 1/5 x 1/2 = 1/10

New ratio of X : Y : Z is -

X = 3/5 - 1/10 = 5/10

Y = 2/5 - 1/10 = 3/10

Z = 1/5 or 2/10

X : Y : Z :: 5 : 3 : 2

Therefore, the new profit sharing ratio of the X : Y : Z will be 5 : 3 : 2.

-

Question 9

5 / -1

Cash Flow Statement is a statement that shows the inflows and the outflows of ___________ during the period.

Solution

The correct answer is Cash and Cash Equivalents.

- A Cash Flow Statement is a statement that shows the inflows and the outflows of Cash and Cash Equivalents during the period.

- In other words, a Cash flow statement is a statement showing the changes in the financial position of a business concern during different intervals of time in terms of cash and cash equivalents.

- Inflows are those transactions that increase the Cash and Cash Equivalents and outflows are those transactions that decrease the Cash and Cash Equivalents.

- Such a statement is prepared in accordance with the Accounting Standard-3 (Revised) on the Cash Flow Statement.

Key Points

- Cash Flows: Cash flows are inflows and outflows of cash and cash equivalent. It implies movement in and moves out of cash and cash equivalents.

- Receipt of cash from a non-cash item is termed as ‘cash inflow’, while cash payment in respect of such item is termed as ‘cash outflow’.

- Cash: Cash comprises cash in hand and demand deposits with the bank.

- Cash Equivalents: Cash equivalents are ‘short-term highly liquid investments that are readily convertible into known amounts of cash and which are subjected to an insignificant risk of change in value’.

-

Question 10

5 / -1

For Non profit organisations, small donation amounts which are not earmarked for any specific purpose may be treated as ________.

Solution

The correct answer is revenue receipts.

Key Points

- Donations are the amounts received by not–for–profit organizations as a gift. It may be a general donation or a specific donation.

- Donations could be used for meeting capital or revenue expenses.

- If donations are received for a special purpose, the amount is credited to a fund from which the amounts are disbursed.

- The fund may be invested in specified securities.

- Income from such investments is credited to the fund Account only.

- Small donation amounts that are not earmarked for any specific purpose may be treated as revenue receipts.

Additional Information

- Revenue Receipts: Any income received from the activities carried out by the organization is termed revenue receipts. Examples include Subscription from members, General Donations, Rent Received, etc.

- Revenue Expenditure is an expenditure, the benefits of which expire within the accounting period. In the case of an NPO, such expenditure means expenditure incurred for social or charitable activities carried on by the NPO. Examples include Materials used, rent, insurance, salaries, honorariums paid, etc.

- Capital Expenditure: It is an expenditure, which benefits the organizations for more than one accounting period. It results in the acquisition of assets that are used for the furtherance of activities carried on by the NPO. Examples include the cost of land, building, furniture, and any addition thereto.

- Capital Receipts: Receipts other than revenue receipts are termed as Capital Receipts. Receipts from donors for the specified purpose are also termed Capital Receipts. Examples include Life Membership Fee, Corpus Donations, Furniture Fund, etc.

-

Question 11

5 / -1

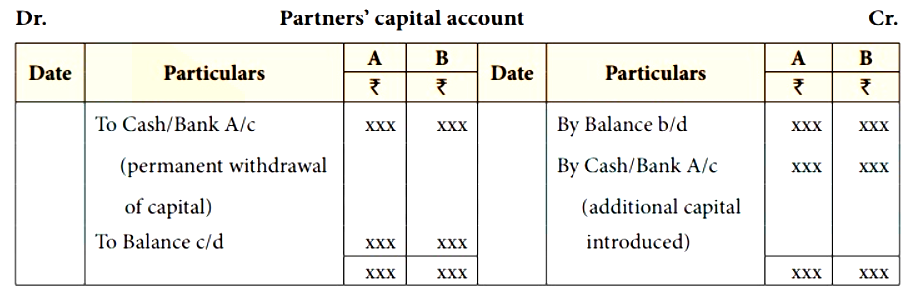

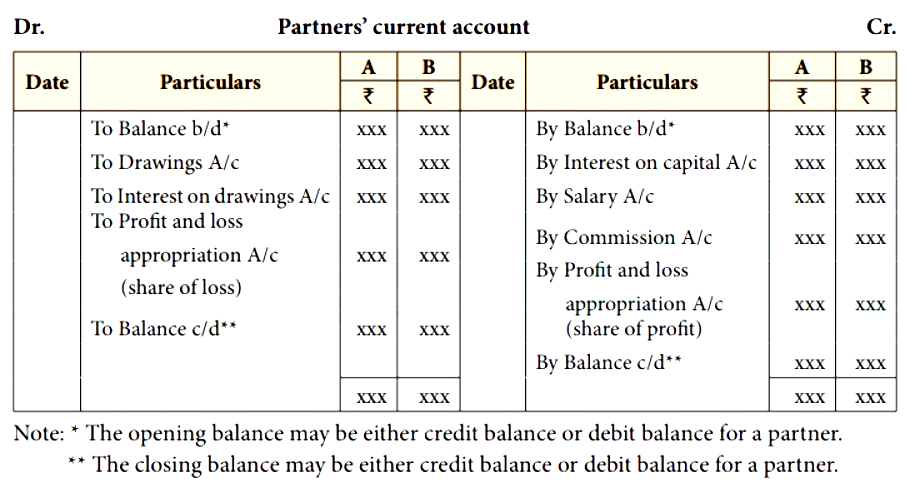

Partner's current account is opened when their capital accounts are ______

Solution

The correct answer is Fixed

Key Points There are two types of methods to account for partners' capitals in case of partnership:

- Fixed Capital

- Fluctuating Capital

Important Points1. Fixed Capital Accounts:

Important Points1. Fixed Capital Accounts:

- Under this system the original capitals invested by the partners remain constant, less and additional capital is introduced by the agreement.

- When fixed capital method is adopted all entries related to drawing, interest on capitals, interest on drawings, salary to partner, share of profit or loss etc, are made in a newly opened account for each partner this account is called current account.

- All the entries related to withdrawing of capital or introducing further capital is recorded in the capital of the partner.

2. Fluctuating Capital:

- When the capitals need not be fixed, the balances of the capital accounts go on changing from time to time.

- The reason is that no separate accounts for current and capital are prepared but all the entries related to drawings, interest on capital, interest on drawings, salary to partner, share of profit and loss etc, are recorded in the capital accounts itself.

Additional Information

-

Question 12

5 / -1

On forfeiture, which of the following accounts are debited?

Solution

The correct answer is Share Capital A/c.

Key Points

- Forfeiture of shares means cancelling the shares for non-payment of calls due as a final action against the defaulting shareholders (s).

- If any shareholder does not pay the amount of the call, the company may exercise the power of the forfeit those shares.

- Shares, however, can be forfeited only if the Articles of Association permit it.

- The company must first give a clear 14 days’ notice to the defaulting shareholders that unless he pays the amount due together with interest, if any, by the specific date, the shares are liable to be forfeited.

- If the shareholder still does not pay, the company may forfeit them by passing an appropriate resolution.

- On forfeiture, the shares are cancelled; to that extent the share capital is reduced but the amount already paid by the shareholders is not returned to him-it is forfeited.

- Of course, the account showing the unpaid call is also cancelled by a credit.

Important Points

The entry passed on forfeiture of shares is

Share capital A/c …Dr.

To Forfeited Shares A/c

To Various Unpaid Calls A/c

Or Calls-in-Arrears A/c

-

Question 13

5 / -1

The balance of ‘Sinking Fund Account’ after the redemption of debentures is transferred to :

Solution

The correct answer is GENERAL RESERVE ACCOUNT.

- The balance of ‘Sinking Fund Account’ after the redemption of debentures is transferred to 'general reserve a/c'.

- Redemption of debentures means repayment of debentures.

- General Reserve A/c: It is the account where all the general reserves or amount of general profits are maintained.

Additional Information

- General Reserve: It is the amount set aside out of profits for no specific purpose. It is available for any future contingency or expansion of the business. It is also known as "Contingency Reserve". Its purpose is to strengthen the financial position of the business.

- Profit and loss account: It is the account where all the incomes, gains, expenses, profits, and losses are recorded. Hence, the loss on the sale of an asset is considered as a loss to the firm so, it is debited to the profit and loss account because all the expenses and losses are recorded in the debit side of the profit and loss account.

- Sinking Fund A/c: It is an account into which a person or company deposits money on a regular basis in order to repay some debt or other liability that will come due in the future.

- Profit & Loss Appropriation A/c: It is a special account that a firm prepares to show the distribution of profits/losses among the partners or partner’s capital. It helps to show a clear distinction between the capital contribution of each partner and the changes thereafter. It includes items such as interest on capital, interest on drawings, interest on partner’s loan, salaries to partners, commission, reserves, and profit share. It doesn’t include drawings made by partners

Key Points .

- Debenture: It refers to a medium for long-term debt financing (usually 5 or more years of financing), that is used by large companies to borrow money. It is the most common type of long-term loan and thus, considered as long-term funds.

-

Question 14

5 / -1

Calls in advance is shown under which head in the balance sheet on the company?

Solution

The correct answer is current liabilities.

Key Points

- Calls-in-Advance is the amount not called up by the company, but paid by the shareholders.

- Interest is allowed on Calls-in-Advance @ 6% p.a.

- A company may accept Calls-in-Advance only if Article of Association authorise to do so.

- Its amount is shown as a separate item, under the head current liabilities.

Additional Information

- Calls-in-Arrears is the amount called by the company, but not paid by the shareholders.

- Interest is charged on Calls-in-Arrears @ 5% p.a.

- Articles of Association does not have any clause to this effect as non-payment is beyond the company’s control.

- Its amount is shown by way of deduction from the called-up capital in the Balance Sheet.

-

Question 15

5 / -1

In the absence of any provision in the partnership agreement, profits and losses are shared by the partners

Solution

The correct answer is option 2 i.e. equally.

Partnership Deed -

- A partnership Deed is a contract between partners in a partnership which sets out the terms and conditions of the relationship between the partners.

- It includes Percentages of ownership and distribution of profits and losses.

- Description of management powers and duties of each partner.

- Partnership registration is optional; it is up to the partners to decide whether to register the partnership firm. However, if a partnership firm is not registered, it would be unable to obtain legal benefits.

Important Points Clauses of Partnership Deed:

A partnership deed normally contains the following clauses:

1. Name of the firm.

2. Nature of the firm’s business

3. The principal place of business.

4. Duration of partnership, if any

5. Names and addresses of partners

6. Amount of capital to be contributed by each partner

7. The amount which can be withdrawn by each partner.

8. The profit-sharing ratio.

9. Rate of interest, if any

10. Amount of Salary or commission payable to partners.

11. Allocation of work among partners.

12. Mode of valuation of goodwill.

13. Procedure for admission, retirement, etc. of a partner.

14. Procedure for maintaining accounts and getting them audited.

15. Procedure to be followed in the event of the dissolution of the firm and settlement of accounts.

16. The arbitration clause in case of disputes among partners.

17. Loans and advances by partners and rate of interest payable on them.

But In the absence of any provision in the partnership agreement, profit and losses are shared equally. Hence, option 2 is correct.

-

Question 16

5 / -1

The formula for valuing goodwill under the capitalization of super profit method is

Solution

The correct answer is Super profit made by the firm divided by the normal rate of return

Key Points

Goodwill:

- Goodwill is the value of a company's reputation earned through time in terms of expected future profits over and above normal profits.

- Goodwill is an intangible real asset that cannot be seen or felt but can be bought and sold.

Important Points

Capitalization of Super Profits method of valuation of goodwill:

- Under this method, Goodwill is calculated by capitalizing the super profits directly.

- Under capitalization of super profit method is Super profit made by the firm is divided by the normal rate of return to get an estimate of goodwill.

- Formula: Goodwill = Super Profits x (100/ Normal Rate of Return)

Additional Information Example: With a capital of Rs. 4,00,000, M/s Mehta and Sons earn an average profit of Rs. 60,000. The average rate of return is 10%. Calculate the firm's goodwill using the capitalization of super profits method.

Solution:

Goodwill = Super profits x (100/ Normal Rate of Return)

Goodwill = 20,000 x 100/10 = 2,00,000.

-

Question 17

5 / -1

M/s Mevo and Sons.; a bamboo pens producing company, purchased machinery for Rs. 9,00,000. It received a dividend of Rs. 70,000 on investment in shares. The company also sold an old machine with the book value of Rs. 79,000 at a loss of Rs. 10,000. Compute the amount of Cash flow/used from/in Investing Activities

Solution

The correct answer is Rs. 7,61,000.

Key PointsCash flow from investing activities:

- The cash generated (or spent) on non-current assets that are expected to generate a profit in the future is referred to as cash flow from investing activities.

- Capital expenditures, lending money, and the sale of investment securities are examples of possible activities.

Important Points

Solution:-

| Particulars | Amount |

| Inflows: | |

| Dividend Received | 70,000 |

| Sale of Old machinery | 69000 |

| Outflows: | |

| Purchase of machinery | (9,00,000) |

| Net Cash Outflow From investing Activities | (7,61,000) |

-

Question 18

5 / -1

Which among the following is a type of Profitability Ratio?

Solution

The correct answer is GROSS PROFIT RATIO.

- Gross Profit Ratio- This ratio indicates the relationship between gross profit and net sales. It can be computed as:

- Gross Profit Ratio = Gross Profit/Net Sales * 100

- Liquidity Ratios- It is also known as "short-term solvency" as it is measured the firm's ability to pay its current dues.

- Total Assets to Debts Ratio- This ratio measures the safety margin available to the suppliers of long-term debts. It is computed as:

- Total Assets to Debts Ratio = Total Assets/Long-term Debts

- Stock Turnover Ratio- This ratio measures how fast the stock is moving through the firm and generating sales.

Key Points

- Profitability Ratios- It measures the overall efficiency in business. Profitability is of utmost importance for a concern.

-

Question 19

5 / -1

On taking responsibility of payment of a liability of ₹ 20,000 by a partner, the account credited will be

Solution

The correct answer is Capital Account of the Partner

Key Points Dissolution of partnership firm:

- According to Section 39 of the Indian Partnership Act 1932, the dissolution of a partnership firm among all the partners is the Dissolution of the Partnership Firm.

- The organisation ceases to exist when a partnership firm dissolves.

- After this, the partnership firm cannot enter into any transaction with anybody. It can only sell the assets to realize the amount, pay the liabilities of the firm and discharge the claims of the partners.

Important Points When the responsibility of payment of liability is taken over by a Partner, the Capital Account of the concerned Partner is credited.

The Journal Entry for a liability which a partner takes responsibility to discharge is given below

Realisation A/c Dr.

To Partner’s Capital A/c

-

Question 20

5 / -1

Income and Expenditure Account is ________ account in nature.

Solution

The correct answer is Nominal.

Key Points

- Income and expenditure account is a summary of income and expenditure of a not–for–profit organization prepared at the end of an accounting year.

- It is prepared to find out the surplus or deficit pertaining to a particular year.

- It is a nominal account in nature in which items of revenue receipts and revenue expenditure, relating to the current year alone are recorded.

- It is prepared following the accrual basis of accounting.

- It is just like preparing a profit and loss account. In this account, incomes are shown on the credit side and expenses are shown on the debit side.

- Apart from cash items, non-cash items such as income accrued but not received, loss or gain on sale of fixed assets, depreciation, etc. will also be recorded.

- It helps to enable the members to know the working of the organization and to know whether its income is sufficient to meet its expenses.

Additional Information

- Accounts that relate to the expenses, losses, incomes, and gains of the business concern are known as nominal accounts.

- For example, Rent Account, Salary Account, Commission Account, etc.

- These accounts are also known as temporary accounts because depending upon their nature (direct or indirect), these accounts are transferred to the Trading or Profit and Loss Account at the end of the financial year.

-

Question 21

5 / -1

Subscription of shares should not be less than ______ % of the issue shares.

Solution

The correct answer is 90%

Key Points Minimum Subscription:

- Minimum subscription refers to the minimum number of shares that a company needs to get subscribed by the public of the entire issue by the date of closure. This amount is mentioned in the prospectus.

- If this limit is not met by the company, then it has to refund all the applications made together with interest thereon and has to make a fresh issue.

Important Points Minimum Subscription clause as per SEBI guidelines is given below:

- For Non-underwritten Public Issues: " If the company does not receive the minimum subscription of 90% of the issued amount on the date of closure of the issue, or if the subscription level falls below 90% after the closure of the issue on account of cheques having being returned unpaid or withdrawal of applications, the company shall forthwith refund the entire subscription amount received. If there is a delay beyond 8 days after the company becomes liable to pay the amount, the company shall pay interest as per Section 73 of the Companies Act 1956."

- For Underwritten Public Issues: "If the company does not receive the minimum subscription of 90% of the net offer to publicly including devolvement of Underwriters within 60 days from the date of closure of the issue, the company shall forthwith refund the entire subscription amount received. If there is a delay beyond 8 days after the company becomes liable to pay the amount, the company shall pay interest prescribed under Section 73 of the Companies Act 1956."

-

Question 22

5 / -1

Which of the following would not be considered a cash flow from operating activities?

Solution

The correct answer is payment of interest on debentures.

- Operating activities are the activities that constitute the primary or main activities of an enterprise.

- For example, for a company manufacturing, operating activities are procurement of raw material, the incurrence of manufacturing expenses, sale of goods, etc.

- These are the principal revenue-generating activities (or the main activities) of the enterprise and these activities are not investing or financing activities.

Additional Information

- Cash Inflows from operating activities

- cash receipts from the sale of goods and the rendering of services.

- cash receipts from royalties, fees, commissions, and other revenues.

- Cash Outflows from operating activities

- Cash payments to suppliers for goods and services.

- Cash payments to and on behalf of the employees.

- Cash payments to an insurance enterprise for premiums and claims, annuities, and other policy benefits.

- Cash payments of income taxes unless they can be specifically identified with financing and investing activities.

- Thus payment for the purchase, wages, and tax payments are operation activities but payment of interest on debentures is a financing activity.

-

Question 23

5 / -1

P and Q are partners sharing profits in the ratio of 3 ∶ 2. P surrenders \(\frac{1}{6}\)th of his share and Q surrenders \(\frac{1}{4}\)th of his share in favour of R, a new partner. What is the sacrificing ratio?

Solution

The correct answer is 1 : 1

Key PointsSacrificing Ratio:

- Whenever there is an admission of a partner, old partners have to surrender some of their old shares in favour of the new partner. The ratio in which they surrender their profits is called sacrifice ratio.

- Goodwill is paid to the old partner's in their sacrifice ratio because the goodwill is the amount of compensation to be paid by the new parties to the old partner for acquiring their share of profits which they have surrendered in the favour of the new partner.

Important Points Calculation of Sacrifice Ratio:

Old Ratio: P : Q = 3 : 2

Part of profit sacrificed by P = \(3 \over 5\) x \(1\over6\)= \(3\over30\) = \(1 \over 10\)

Part of profit sacrificed by Q = \(2 \over 5\) x \(1\over4\)= \(2\over20\) = \(1 \over 10\)

Sacrifice Ratio = 1 : 1

-

Question 24

5 / -1

A company issued and allotted shares to a selected group of persons. Which concept is indicated in this statement?

Solution

The correct answer is Private placement of share

Key Points Private placement of share:

- A private placement is when capital is raised through a small group of selected investors rather than issuing shares to the general public.

- It is an alternative to an initial public offering (IPO) for a company seeking to raise capital for expansion.

Additional Information

- Right Issue: A rights issue is a company's offering of rights to existing shareholders, allowing them to purchase additional shares.

- Employee Stock Option Plans (ESOPs) or Employee Stock Ownership Plans (ESOPs) are employee benefit plans that allow employees to buy company stock. Employees buy these shares at a discount, or at a price below market value.

-

Question 25

5 / -1

Assertion (A): Operating cycle of business signifies the time required by the company's operations to convert it into cash

Reason (R): The operating cycle of the service industry is smaller than the operating cycle of manufacturing industries.

Solution

The correct answer is Both (A) and (R) are correct but (R) is not the right explanation of (A)

Key PointsAnalysing the statements:

Assertion (A): Operating cycle of business signifies the time required by the company's operations to convert it into cash

- An Operating Cycle refers to the days required for a business to receive inventory, sell the inventory, and collect cash from the sale of the inventory.

- This cycle plays a major role in determining the efficiency of a business.

- Therefore, this statement is correct.

Reason (R): The operating cycle of the service industry is smaller than the operating cycle of manufacturing industries.

- This is correct because the number of steps involved in manufacturing is spread over a wide range starting from manufacture to final selling.

- Production takes longer than the hiring of service personnel.

Important PointsThere is no causal connection between the two statements. Therefore Reason (R) is not the correct explanation of Assertion (A).

-

Question 26

5 / -1

X Ltd., has a current ratio of 3.5:1 and quick ratio of 2:1. If excess of current assets over quick assets represented by inventories is Rs. 24,000, calculate current assets and current liabilities.

Solution

The correct answer is Current Liabilities = Rs. 16000 and Current Assets = Rs. 56000.

Current Ratio = 3.5:1

Quick Ratio = 2:1

Let Current liabilities = x

Current assets = 3.5x and Quick assets = 2x

Inventories = Current assets – Quick assets

24,000 = 3.5x – 2x 24,000

1.5x x = Rs.16,000

Current Liabilities = Rs.16,000

Current Assets = 3.5x = 3.5 × Rs. 16,000 = Rs. 56,000.

Verification :

Current Ratio = Current assets : Current liabilities

= Rs. 56,000 : Rs. 16,000

= 3.5 : 1

Quick Ratio = Quick assets: Current liabilities

= Rs. 32,000 : Rs. 16,000

= 2 : 1

-

Question 27

5 / -1

P, Q, and R entered into a partnership with a capital ratio of 11 ∶ 12 ∶ 13, ratio of their time for investment is 1 ∶ 2 ∶ 3. If the profit of Q at the end of the partnership is Rs. 4800. Then, find the total profit.

Solution

The correct answer is Rs. 14800

Important Points

Given:

Investment ratio = 11 ∶ 12 ∶ 13

Ratio of Time = 1 ∶ 2 ∶ 3

Formula:

Profit = Investment × Time

Calculation:

Ratio of their profit = (11 × 1) ∶ (12 × 2) ∶ (13 × 3) = 11 ∶ 24 ∶ 39

⇒ Profit of Q = 24 unit = Rs. 4800

⇒ 1 unit = 200

∴ Total profit = 74 unit = 74 × 200 = Rs. 14800

-

Question 28

5 / -1

X and Y are partners in a firm. They do not have any partnership agreement. What should be done in the given case?

X wants to introduce his son Z into his business. Y objects to his proposal.

Solution

The correct answer is Z WILL GET ADMISSION INTO PARTNERSHIP WITHOUT Y'S CONSENT.

- No person can be introduced as a partner without the consent of the partners. Therefore, Z cannot be admitted into the partnership because of Y objects to it.

As per Section 4 of the Indian Partnership Act, 1932, "Partnership is defined as the relation between persons who have agreed to share the profits of a business carried on by all or any one of them acting for all".

-

Question 29

5 / -1

Find out operating Ratio:

Cost of goods sold - 350000

Selling and distribution Expenses - 20,000

Administrative & office Expenses - 30,000

Net sales - 5,00,000.

Solution

The correct answer is 80%.

Key Points Operating Ratio:

- The operating ratio is the ratio of a company's operating expenses to its revenue.

- This financial ratio is most typically utilized in businesses where a substantial percentage of revenues is required to keep the business running.

- By comparing operating expenses to net revenues, the operating ratio can be used to assess the efficiency of a company's management.

- The lower the ratio, the more profitable the company will be.

Important Points

Operating Costs = Cost of goods sold + Administrative & office Expenses + Selling and distribution Expenses

Operating Costs = 3,50,000 + 20,000 + 30, 0000 = 4,00,000

Operating Ratio = (Operating Costs / Net sales) × 100

Operating Ratio = (4,00,000 / 5,00,000) × 100 = 80%

Additional Information

- Operating ratio establishes the relationship between cost of goods sold and other operating expenses on the one hand and the sales on the other.

- Operating Ratio = Operating Cost / Net Sales × 100 = Cost of goods sold + operating expenses / Net sales × 100

- Operating ratio indicates the percentage of net sales that is consumed by operating cost.

- Operating expenses = Selling and distribution expenses + Administrative & office expenses.

-

Question 30

5 / -1

Out of the following items, which is shown in the ‘Receipts and Payments A/c’ of a not for profit organization?

Solution

The correct answer is all of the above.

Key Points

- Subscription is a regular payment made by the members of the organization. It is generally contributed annually.

- It is one of the main sources of income of non-profit organizations.

- Subscriptions received during the year are shown on the debit side i.e. Receipts side of the Receipts and Payments Account.

- Apart from the amount for the current year, it may include the amount pertaining to the previous year or advance payment for the next year.

Additional Information

- Receipts and payment is an account that shows the summary of all cash and bank transactions that occurred during an accounting period.

- It starts with the opening balances of cash and bank and ends with the closing balances of cash and bank.

- This account is a Real Account and lays the basis for the preparation of the Income and Expenditure Account and the Balance Sheet.

-

Question 31

5 / -1

Proprietary Ratio = ?

Solution

The correct answer is SHAREHOLDERS' FUNDS/TOTAL ASSETS.

- Proprietary Ratio- This ratio shows the extent to which the total assets have been financed by the proprietor. It can be computed as:

- Proprietary Ratio = Shareholders' funds or Proprietary funds/Total Assets

- It is a type of "Solvency Ratio".

Key Points

- Solvency Ratios- It is also known as "long-term solvency" as it is measured the firm's ability to meet its long-term indebtedness and thus, conveys an enterprise's ability to meet its long-term obligations.

-

Question 32

5 / -1

Varsha and Monica are partners sharing profit and losses in the ratio of 3 : 2 having the capital of Rs. 80,000 and Rs. 50,000 respectively. They are entitled to 9% p.a. interest on capital before distributing the profit. During the year firm earned Rs. 7,800 after allowing interest on capital. Profit apportioned among Varsha and Monica is :

Solution

Profit of Firm = Rs.7800

Profit sharing ratio = 3:2

Profit for Varsha = 7800*3/5 = 4680

Profit for Monica = 7800*2/5 = 3120

Hence Option1 is the correct answer.

- In accordance with the provisions of the partnership deed, the profits and losses made by the firm are distributed among the partners.

- However, sharing of profit and losses is equal among the partners, if the partnership deed is silent.

- However, certain adjustments such as interest on drawings & capital, salary & commission to partners are required to be made.

- For this purpose, it is customary to prepare a Profit and Loss Appropriation Account of the firm.

- The final figure of profit and loss to be distributed among the partners is ascertained by the Profit and Loss Appropriation Account.

-

Question 33

5 / -1

The excess amount paid over the called up value of a share is known as _______

Solution

The correct answer is calls in advance.

Important Points

- The excess amount paid over the called up value of a share is known as calls in advance. It is the excess money paid on application or allotment or calls.

- Such excess amount can be returned or adjusted towards future payment.

- If the company decides to adjust such amount towards future payment, the excess amount may also be transferred to a separate account called calls in advance account.

- Calls in advance does not form part of the company’s share capital and no dividend is payable on such amount.

- In the balance sheet, it should be shown under current liabilities.

- As per Section 50 of the Indian Companies Act, 2013, the company can accept calls in advance only if it is authorised by its Articles of Association. As per Table F of the Indian Companies Act, 2013, interest may be paid on calls in advance if Articles of Association so provide not exceeding 12% per annum.

Key Points

- Calls in arrears is the situation when the shareholder fails to pay the called money in the allocated time by the company.

- Forfeiture of share means the cancellation of the shares for non-payment of calls due.

- Paid-up capital is the amount of money a company has received from shareholders in exchange for shares of stock.

- The amount of share capital shareholders owe, but have not paid, is referred to as called-up capital.

-

Question 34

5 / -1

From the following information, calculate the cash flow from financing activities:

| Particulars | 31st March, 2019

(Rs.) | 31st March, 2020

(Rs.) |

Equity Share Capital 10% Debentures Securities Premium | 4,00,000 1,50,000 40,000 | 5,00,000 1,00,000 50,000 |

Additional Information: Interest paid on debentures Rs. 10,000.

Solution

The correct answer is 50,000.

Calculation of net cash flow from financing activities:

| Particulars | Rs. |

Cash proceeds from the issue of shares (including premium) Interest paid on Debentures Redemption of Debenture Net cash flow from financing activities | 1,10,000 (10,000) (50,000) 50,000 |

- Note: Cash proceeds from the issue of shares (including premium) = Increase in equity share capital of Rs.1,00,000 from previous year to current year + Increase in securities premium of Rs.10,000 from previous year to current year.

- Net cash flow from financing activities = Cash proceeds from the issue of shares (including premium) - Interest paid on Debentures - Redemption of Debenture.

-

Question 35

5 / -1

In respect of partnership business, LLP stands for

Solution

The correct answer is Limited Liability Partnership.

- LLP stands for limited liability partnership, which signifies a type of business structure.

- Most states require that limited liability partnerships have either "Limited Liability Partnership" or "LLP" as part of the company's name.

Additional Information

- Limited Liability Partnership:

- Limited Liability Partnership (LLP) is an alternative form of business organisation.

- It not only provides the benefits of limited liability but also allows its members the flexibility of organising their internal affairs as a partnership based on a mutually arrived agreement.

- Liability of the partners is not as limited as that of a shareholder in a company.

-

Question 36

5 / -1

X Ltd. forfeited 20 shares of Rs.10 each, Rs. 8 called up, on which John had paid application and allotment money of Rs. 5 per share, of these, 15 shares were reissued to Parker as fully paid up for Rs. 6 per share. What is the balance in the share Forfeiture Account after the relevant amount has been transferred to Capital Reserve Account?

Solution

The correct answer is Rs 25

Important Points

| Date | Particulars | Dr. (Rs) | Cr. (Rs) |

| a) | Share Capital a/c (20 shares x 8) Dr To Share Forfeited a/c(20 shares x5) To Calls in arrears a/c (20 shares x3) (Being 20 shares of 10 each, Rs 8 called up forfeited for the non-payment of call) | 160 | 100 60 |

| b) | Bank a/c (15 shares x 6) Dr Share Forfeiture a/c (15 shares x4)Dr. To Share Capital a/c (15 shares x10) (Being 15 shares were reissued as Rs 10 paid up for Rs. 6 per share) | 90 60 | 150 |

| c) | Share Forfeiture a/c Dr To Capital reserve (Being transfer of Profit on Reissue of 15 shares) | 15 | 15 |

Working note:-

| Profit on 20 Shares (20 x 5) | Rs. 100 |

| Profit on 20 Shares (15 x 5) | Rs. 75 |

| Less:- Loss on Reissue (15 x 4) | Rs. 60 |

| Amount to be transferred to Capital Reserve | Rs. 15 |

Amount Left in Share Forfeiture = No. of shares not reissued x Amount paid by John Per share

Amount Left in Share Forfeiture = 5 x 5 = Rs. 25

-

Question 37

5 / -1

Unpaid dividends are shown under which head in the balance sheet of the company?

Solution

The correct answer is other current liabilities.

Key Points

The amounts under other current liabilities shall be classified as:

- Current maturities of long-term debt;

- Current maturities of finance lease obligations;

- Interest accrued but not due on borrowings;

- Interest accrued and due on borrowings;

- Income received in advance;

- Unpaid dividends;

- Application money received for allotment of securities and due for refund and interest accrued thereon.

- Share application money includes advances towards the allotment of share capital.

-

Question 38

5 / -1

The balance in the Investment Fluctuation Reserve, after meeting the loss on revaluation of investments, at the time of admission of a partner will be transferred to :

Solution

The correct answer is Old Partners' Capital Accounts

Key Points Investment Fluctuation Reserve:

An Investment Fluctuation Reserve is a fund reserved from profits to cover losses in the market value of investments. It is created to compensate for the difference between an investment's book value and market value.

Treatment of Investment Fluctuation Reserve:

If the price of investments falls during revaluation, the loss is removed from the investment fluctuation reserve and the balance is distributed among the old partners according to their old profit sharing ratio.

The Journal Entry is given below:

| Particulars | Amount Dr. | Amount Cr. |

| Investment Fluctuation Reserve A/c Dr. | xxx | |

| To Partner's Capital A/c | | xxx |

-

Question 39

5 / -1

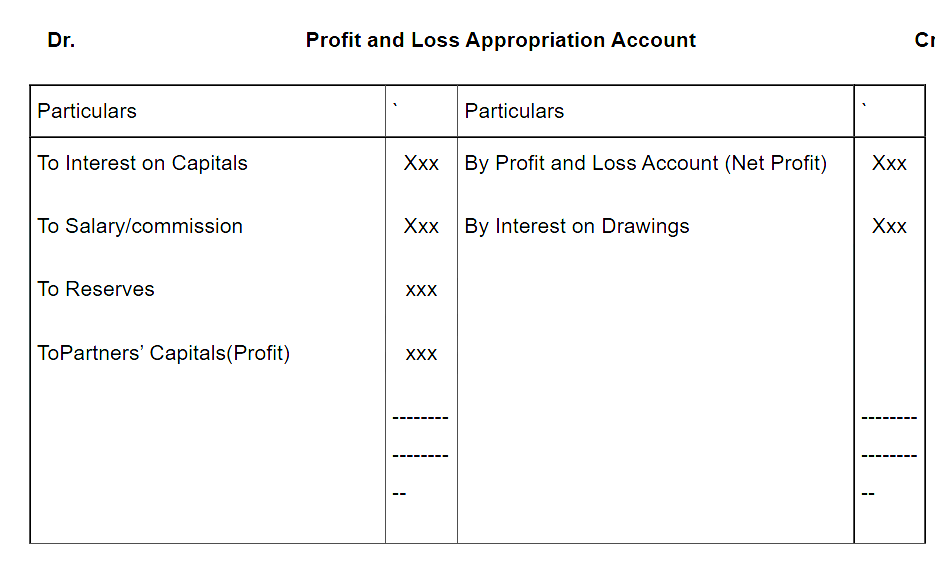

The Journal Entry to transfer interest on capital to Profit and Loss Appropriation Account would be :

Solution

The correct answer is Option 2

Key PointsProfit and Loss Appropriation Account

- Profit and Loss Appropriation Account is a nominal account prepared for the purpose of distributing profits/losses among the partners after making all the adjustments relating to Interest on Capitals, Interest on Drawings, Salary/commission to partners and transfer to Reserve.

- It is an extension of Profit and Loss Account.

- It contains the items relating only to the partners’ claim.

Important Points Journal Entries for Interest on Capital transferred to Profit and Loss Appropriation Account

Interest on Capital A/c Dr.

To Partner’s Capital/Current A/c

Additional Information

Profit and Loss Appropriation Account Format

-

Question 40

5 / -1

A club received Rs. 20,000 as subscriptions during the year 2014-15 of which Rs.3,000 relate to year 2013-14 and Rs.2,000 to 2015-16, and at the end of the year 2014-15 Rs.6,000 are still receivable. What is the amount to be shown in Receipts and payments Account?

Solution

The correct answer is Rs. 20,000.

Key Points

- Subscription is a membership fee paid by the member on annual basis.

- This is the main source of income for non-profit organizations.

- Subscription paid by the members is shown as a receipt in the Receipt and Payment Account and as income in the Income and Expenditure Account.

- It may be noted that the Receipt and Payment Account shows the total amount of subscriptions actually received during the year.

- However, the amount shown in the Income and Expenditure Account is confined to the figure related to the current period only irrespective of the fact whether it has been received or not.

- A club received Rs. 20,000 as subscriptions during the year 2014-15 of which Rs.3,000 relate to the year 2013-14 and Rs.2,000 to 2015-16, and at the end of the year 2014-15 Rs.6,000 are still receivable.

- In this case, the Receipt and Payment Account will show Rs.20,000 as a receipt from subscriptions.

- But the Income and Expenditure Account will show Rs. 21,000 as income from subscriptions for the year 2014-15, the calculation of which is given as below:

Subscriptions received in 2014-15 20,000

Less: Subscriptions for the year 2013-14 3,000

Less: Subscription for the year 2015-16 2,000

Add: Subscriptions outstanding for the year 2014-15 6,000

Income from subscriptions for the year 2014-15 21,000

-

Question 41

5 / -1

How will you treat payment of ‘Interest of Debentures’ while preparing a Cash Flow Statement ?

Solution

The correct answer is cash flow from financing activities.

- Financing activities relate to long-term funds or capital of an enterprise, e.g., cash proceeds from the issue of equity shares, debentures, raising long-term bank loans, repayment of bank loans, payment of interest, etc.

- Thus interest paid to debentures is a cash flow from financing activities.

Additional Information

- Investing activities are the acquisition and disposal of long-term assets and other investments not included in cash equivalents. Investing activities relate to the purchase and sale of long-term assets or fixed assets such as machinery, furniture, land, and building, etc.

- Operating activities are the activities that constitute the primary or main activities of an enterprise. For example, for a company manufacturing, operating activities are procurement of raw material, the incurrence of manufacturing expenses, sale of goods, etc.

- As per AS-3, ‘Cash’ comprises cash in hand and demand deposits with banks, and ‘Cash equivalents’ means short-term highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value.

-

Question 42

5 / -1

A director of a company invited application for 25,000 shares of ₹100 each at a premium of ₹10 per share. Total application money received was ₹6,00,000 at the rate of application ₹20 per share. Find number of shares applied by public.

Solution

The correct answer is 30,000

Important Points Total number of shares applied by public = Total application money received / rate of application

Total number of shares applied by public = 6,00,000 / 20 = 30,000

Additional Information

Oversubscription of shares:

- Oversubscription of shares is a situation that occurs when a company receives more applications to purchase their shares compared to the number of shares that they have issued.

- It is a situation in which buyers show so much interest in a new stock that demand exceeds supply.

-

Question 43

5 / -1

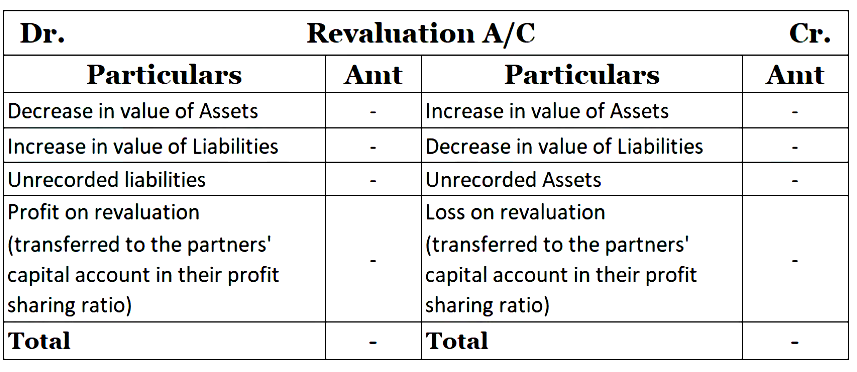

A, B and C are partners sharing profits and losses equally. D is admitted as a new partner. The value of machinery has increased by ₹5,000 and creditors by ₹2,000. The share of profit on revaluation of each partner is:

Solution

The correct answer is ₹1000.

Important Points Solution

Revaluation Account

| Particulars |

Amount |

Particulars |

Amount |

| To Increase in Creditors |

2000 |

By Increase in Machinery |

5000 |

| To Profit on Revaluation (Transferred to Capital A/c) |

|

|

|

| A: 1000 |

3000 |

|

|

| B: 1000 |

|

|

| C: 1000 |

|

|

| Total |

5000 |

Total |

5000 |

Therefore, each partner's share is ₹1000.

Additional Information Revaluation Account:

- The revaluation account is a nominal account used to distribute and transfer profits and losses resulting from changes in the book value of assets and liabilities, such as admission of a partner, retirement of a partner, and death of a partner.

Format of Revaluation account

-

Question 44

5 / -1

Calculate the Trade receivables turnover ratio from the following information:

Total Revenue from operations = Rs. 4,00,000

Cash Revenue from operations = 20% of Total Revenue from operations

Trade receivables as at 1.4.2014 = Rs. 40,000

Trade receivables as at 31.3.2015 = Rs. 1,20,000

Solution

The correct answer is 4 times.

Trade Receivables Turnover Ratio = Net Credit Revenue from Operations /Average Trade Receivables

Credit Revenue from operations = Total revenue from operations – Cash revenue from operations

Cash Revenue from operations = 20% of Rs. 4,00,000

= Rs. 4,00,000 20 100

= Rs. 80,000

Credit Revenue from operations = Rs. 4,00,000 – Rs. 80,000

= Rs. 3,20,000

Average Trade Receivables = Opening Trade Receivables + Closing Trade Receivables /2

= Rs. 40,000 + Rs. 1,20,000 /2

= Rs. 80,000

Trade Receivables Turnover Rations = Net Credit Revenue Form Operations /Average Inventoary

Trade Receivables Turnover Ratio = Rs. 3,20,000/ Rs. 80,000

= 4 times.

-

Question 45

5 / -1

What would be the accounting entry for a partner’s withdrawal of cash in lieu of salary ?

Solution

Partners current account:

- In the case of a partnership type of ownership in a business, the partner's current account is prepared when capital is fixed.

- Transactions such as drawings, salary, and interest on capital and drawings are recorded.

- The balance of this account fluctuates every year.

- The balance can be both credit or debit.

- Partners can take money out of the business whenever they want.

- Partners are typically not considered employees of the company and may not get paychecks.

- When the partners take money out of the business, it is recorded in the Withdrawals or Drawing account thereby it decreases the Partner's current account.

3 Golden Rules:

- debit the receiver, credit the giver

- debit what comes in, credit what goes out

- debit all the expenses and losses, credit all the incomes and gains

Reason for debit and credit:

- Partners Current A/c - Personal A/c, the debtor is liable to receive the money. He is the receiver therefore it's debited

- Cash A/c - Real account, cash is going out of the firm.

Journal Entries:

Dr Partner’s Current A/c

To Cash A/c

-

Question 46

5 / -1

As per the format of Balance sheet prescribed as per Schedule III of Companies act 2013, Capital Work in progress is shown under the heading of

Solution

The Correct Answer is Fixed Assets

Important Points

- Capital Work in progress: The cost incurred on the assets of a company that is still under construction at the time of preparation of the Balance Sheet is called Capital Work in progress.

- For Example- The cost incurred on the construction of a new building would be termed as Capital Work in Progress.

- As per Schedule III of Companies act 2013, Capital Work in progress is mentioned under subhead Fixed Assets, under Head Non-Current Assets.

Additional Information

- Intangible assets: These are the assets of the business that do not have a physical existence. For example- Goodwill, Patents, Trademarks, etc.

- Current assets: These assets are those assets of the business which are expected to convert to cash within a period of one year.

- Fixed Assets: These assets are those assets of the business which are of permanent nature. These assets are expected to last more than one year. Fixed assets are assets that a business intends to utilize in the long run to create revenue.

- Loans and advances: These are the sources of finance of the business both for long-term and short term. Primarily, Loans are intended for long-term finance and Advances are intended for short-term finance needs.

-

Question 47

5 / -1

The following information is provided of M/s Raj Petro for the year enced on 31st December 2018:

(i) Actual Salaries paid Rs. 1,02,000

(ii) Prepaid Salaries as on 31.12.2017 is Rs. 12.000

(ii) Prepaid Salaries as on 31.12.2018 is Rs. 6,000

(iv) Outstanding Salaries as on 31.12.2017 is Rs. 9,000

(v) Outstanding Salaries as on 31.12.2018 is Rs. 7,500

Calculate the amount of Salaries chargeable to Income and Expenditure account for the year ending on 31 December 2018.

Solution

Key Points

Statement of Salaries for the year ended December 31, 2018

| Particulars | Rs. |

| Amount paid for Actual Salaries | 1,02,000 |

| Add: Prepaid Salaries as on 31.12.2017 | 12,000 |

| Less: Prepaid Salaries as on 31.12.2018 | 6,000 |

| Less: Outstanding Salaries as on 31.12.2017 | 9,000 |

| Add: Outstanding Salaries as on 31.12.2018 | 7,500 |

| Total | 106500 |

Salaries chargeable to Income and Expenditure account = Rs. 1,06,500

-

Question 48

5 / -1

The capital redemption reserve account on redemption of preference shares may be applied by the company, in paying

Solution

The correct answer is bonus shares.

Key Points

- When a company purchases its own shares out of free reserves or securities premium account, a sum equal to the nominal value of the shares so purchased shall be transferred to the capital redemption reserve account and details of such transfer shall be disclosed in the balance sheet.

- The capital redemption reserve account may be applied by the company, in paying up unissued shares of the company to be issued to members of the company as fully paid "bonus shares".

Additional Information

- Bonus shares are additional shares given to the current shareholders without any additional cost, based upon the number of shares that a shareholder owns. These are the company's accumulated earnings that are not given out in the form of dividends but are converted into free shares.

- Sweat equity shares mean equity shares issued by a company to its employees or directors at a discount or for consideration, other than cash for providing know-how or making available rights in the nature of intellectual property rights or value additions, by whatever name called.

- Under rights shares, new shares are offered to the existing shareholders. These shares are issued in proportion to the shares held by the existing shareholders.

-

Question 49

5 / -1

Assertion: Dissolution of the firm means the discontinuation of partnership among partners.

Reason: Dissolution of a firm and Dissolution of a partnership is one and the same thing.

Solution

The correct answer is A IS TRUE BUT R IS FALSE.

Key Points

- Dissolution of a firm means dissolution of a partnership between all the partners of a firm. In this case, the business of the firm is closed, the assets are realized, and the liabilities are paid.

- Dissolution of partnership refers to the change in the existing relations of the partners. In this case, the firm continues its business.

Important PointsKey differences between Dissolution of a firm and Dissolution of a partnership

| Basis | Dissolution of Partnership | Dissolution of Partnership Firm |

| Termination of business | The business is not terminated. | The business of the firm is closed. |

| Settlement of assets and liabilities | Assets and liabilities are revalued and a new balance sheet is drawn | Assets are sold and

liabilities are paid-off. |

Court's

intervention | Court does not intervene

because partnership is

dissolved by mutual

agreement. | A firm can be dissolved by

the court's order. |

Economic

relationship | Economic relationship

between the partners

continues though in

exchanged form. | Economic relationship

between the partners

comes to an end. |

| Closure of books | Does not require because

the business is not

terminated. | The books of account are

closed. |

-

Question 50

5 / -1

Which of the following represents accounting equation?

Solution

The correct answer is Assets= Liabilities+ Capital

Accounting equation:

- The recording of business transactions in the books of account is based on a fundamental equation which is called the Accounting Equation.

- Whatever business possesses in the form of assets is financed by the owner or by outsiders.

- The accounting equation expresses the equality of assets on the one side and equity on the other side i.e., the claims of an outsider [liabilities] and owners or proprietors funds on the other side. If an asset is introduced in the business, a corresponding liability also emerges.

- It is represented as:

- Assets = Equity

- Equity = Liabilities + Capital

- Assets= Liabilities+ Capital

Effects of business transaction on accounting equation:

- Sunil started the business with cash 3,00,000 as Capital.

- In this transaction, an asset in the form of cash is created for the business.

- Cash (Asset) Capital (Equity)

- 3,00,000 = `3,00,000

×

×

Sign in

Sign in

Profile

Profile Signout

Signout