-

Question 1

5 / -1

______ capital account always shows positive or credit balance.

Solution

The correct answer is Fixed.

Key Points

Key Points

- In fixed capital method two accounts namely capital and current a/c are prepared.

- All transactions related to capital introduction and withdrawals by partners are recorded in Capital A/c and other adjustments like interest on capital, interest on drawings, commission, salary, share of profit or loss are recorded in Current A/c.

- As the name suggests, 'fixed capital account' this account shows a fixed capital balance and always shows positive or credit balance.

Important Points

Important Points

- Credit Balance - When credit side of an account exceeds debit side, the balancing figure is known as credit balance.

- Capital Account - Capital account is prepared to show introduction, withdrawal and balance of capital by partners in a partnership firm. Capital Accounts can be prepared by fixed and fluctuating capital method.

| Particulars | Fixed Capital Method | Fluctuating Method |

|---|

| Accounts prepared | Two - Capital A/c and Current A/c | One - Capital A/c |

| Balancing figure | Credit | Debit or capital |

| Nature of Capital balance | Does not change | Changes |

| Disclosure in Partnership deed | Specifically stated in partnership deed | Not needed |

| Adjustments | Only in current A/c | In capital A/c |

-

Question 2

5 / -1

The most commonly used tools for financial analysis are

Solution

The correct answer is All of the above.

Key Points

Financial analysis means analysis and interpretation of financial statements. Financial analysis helps to know financial position, operational efficiency, future prospectus of business and also helps to make decisions in future.

Important Points

The most common financial tools are:

- Comparative statement

- Common size statement

- Trend analysis

- Ratio analysis

- Cash flow analysis

Additional InformationComparative statement- an item compared with itself in the previous year to know whether it has increased or decrease.

Additional InformationComparative statement- an item compared with itself in the previous year to know whether it has increased or decrease.

Common size statement- an item compared with itself in the previous year to know whether it has increased or decreases in percentage ratio.

Trend analysis- determines the direction upwards or downwards and involves the computations in the percentage.

Ratio analysis-describe profitability, solvency and efficiency of an enterprise by finding relationship of items in balance sheet and Profit & Loss statement.

Cash flow analysis- analysis of actual movement of cash into and out of an organization.

-

Question 3

5 / -1

Debit Balance of Profit and Loss account is shown under the sub head __________ of the Balance Sheet as per Revised Schedule III of Companies Act, 2013.

Solution

The correct answer is Reserves and Surplus

Key PointsProfit and Loss Statement:

- A profit and loss (P&L) statement is a financial statement that summarizes all of a company's expenses and revenues over a period of time.

- It helps in examining a company's financial performance.

- A profit and loss account's debit balance indicated a loss. The profit and loss account's debit balance demonstrates that expenses exceeded revenues. It is deducted from the Capital Account.

- The Credit balance of Profit and Loss Account shows profit as, here, revenues are more than expenses. It is added to the Capital Account.

Important Points As per Revised Schedule III of Companies Act, 2013:

- Debit balance of statement of profit and loss shall be shown as a negative figure under the head ―'Surplus'.

- Similarly, the balance of ―'Reserves and Surplus', after adjusting the negative balance of surplus, if any, shall be shown under the head ―'Reserves and Surplus' even if the resulting figure is in the negative

Additional Information Reserves and Surplus:

Reserves and Surplus shall be classified as:

- Capital Reserve

- Capital Redemption Reserve

- Securities Premium Reserve

- Debenture Redemption Reserve

- Revaluation Reserve

- Share Options Outstanding Account

- Other Reserves–(specify the nature and purpose of each reserve and the amount in respect thereof)

- Surplus i.e., balance in Statement of Profit and Loss disclosing allocations and appropriations such as dividend, bonus shares and transfer to/ from reserves, etc.

-

Question 4

5 / -1

The opening balance of Prize Fund was ₹32,800. During the year, donations received towards this fund amounted to ₹15,400; amount spent on prizes was ₹12,300 and interest received on prize fund investment was ₹4,000. The closing balance of Prize Fund will be :

Solution

The correct answer is ₹39,900.Key Points

Non Profit organization – institutions which function without any profit motive. These organizations are welfare of society. Such organization is clubs, schools, trade unions, charitable institutions.

For financial statement of non-profit organisation, the following accounts are prepared:

- Receipt and payment A/c

- Income and expenditure A/c

- Balance sheet

Important Points

Receipt and Payment of prize fund A/c

Dr. Cr.

Receipts | ₹ | Payments | ₹ |

The balance b/d | 32,800 | Amount paid for prize | 12,300 |

Donation received | 15,400 | The balance c/d (Balancing Fig) | 39,900 |

Interest received | 4,000 | | |

| Total | 52200 | Total | 52200 |

Alternate Method Prize fund closing balance = opening balance+ donation received +interest received on prize fund – amount paid for prizes

Alternate Method Prize fund closing balance = opening balance+ donation received +interest received on prize fund – amount paid for prizes

=32,800+15,400+4,000-12,300

=39,900

-

Question 5

5 / -1

A and B are partners in a firm sharing profits and losses in the ratio of 3 ∶ 1. On 31st March 2021 they decided to share future profits and losses equally. On that date, Goodwill of the firm was Rs. 40,000 and Workmen Compensation Reserves was Rs. 80,000 appears in the Balance sheet. For writing off goodwill amount distributed in _____(i)_____ and for adjustment of Workmen compensation reserve in amount distributed in _________(ii)_________.

Solution

The correct answer is (i) Old Profit-Sharing Ratio and (ii) Old Profit-sharing Ratio.

Key Points

Goodwill - The established reputation of a business, regarded as a quantifiable asset and calculated as part of its value. The fictitious assets of the firm.

Workmen Compensation Reserve - Reserve created out of firm’s profits to pay compensation to employees.

Important Points When there is change in partnership between the partners, then treatment of goodwill and reserve can be made in two methods:

- When partners decide to write off goodwill and reserves completely from balance sheet-Amount of goodwill and reserves will distributed between among partners in old ratio.

- When partners decide to retain goodwill and reserves in balance sheet- adjusted amount of goodwill and reserves will distributed between among partners in sacrifice ratio/gain ratio to partner’s capital account.

Thus, decision for writing off goodwill will be distributed in old profit sharing ratio of partners and for the adjustment of Workmen compensation Reserve, it will be distributed in Old profit sharing ratio.

Additional Information When there is change in P&L ratio among the partners, it will be sacrifice for some partner on the other gain for some partner.

Here sacrifice ratio/gain ratio will be :

Sacrifice ratio= old ratio - new ratio

A = 3/4 - 1/2 = 1/4

B= 1/4 -1/2 = -1/4((minus means here Bis gaining)

-

Question 6

5 / -1

Salary paid for the year ended 31st March 2010 amounted to ₹75,000. How much amount will be recorded in Income and Expenditure Account in the following case?

| | 31-3-2009 | 31-3-2010 |

| Outstanding Salary | 6500 | 6000 |

| Prepaid Salary | 1200 | 1000 |

Solution

The correct answer is ₹74,700

Key Points

Outstanding expenses: expenses due for the year but not paid. These are liabilities for the organization.

Prepaid Expenses: expenses which are paid in advance. These are assets to the organization.

Important Points Calculation for salary paid for the year 2010 -

| Particulars | ₹ |

| Salary paid for the year | 75000 |

| Less: Outstanding salary for 2009 | (6500) |

| | 68500 |

| Add: Outstanding Salary for 2010 | 6000 |

| Add: Prepaid salary for 2009 | 1200 |

| | 75700 |

| Less: Prepaid Salary for 2010 | (1000) |

| | 74700 |

Additional InformationSalary is an expense for the Non-Profit organization. So, it is recorded on the expenditure side i.e. debit side of the Income and Expenditure A/c.3

Hint

Hint

| Opening balance | Closing balance |

Outstanding expenses | - | + |

prepaid expenses | + | - |

-

Question 7

5 / -1

A cash flow statement does not show :

Solution

A cash flow statement does not show whether a credit limit is breached

Key Points Cash Flow Statement:

- A cash flow statement (CFS) is a financial statement that shows how much cash and cash equivalents are coming in and going out of a business.

- The CFS assesses a company's ability to manage its cash position, or how successfully it generates cash.

- The CFS is a useful addition to the balance sheet and income statement.

- Cash is the most important component of the CFS, and it comes from three sources: operating, investing, and financing activities.

Important Points A cash flow statements accounts for the Cash Inflows and Outflows of the Cash and Cash equivalents in the business. Since, credit limit is used to take loans, it will only take into account the amount of loan availed, as it is an inflow of Cash and Cash equivalent. It will not show whether the credit limit is breached or not.

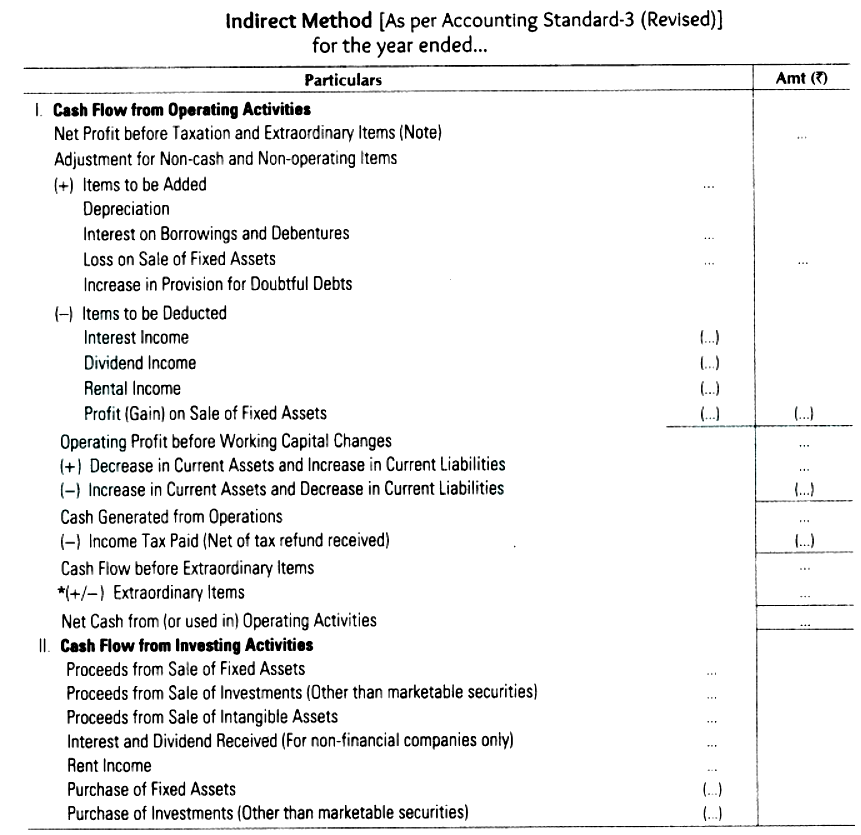

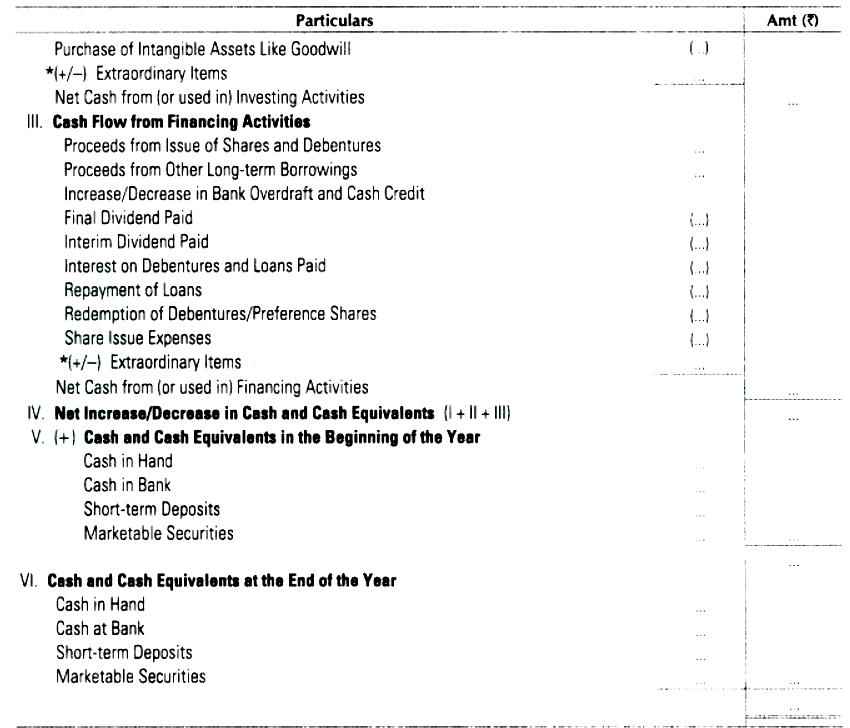

FORMAT OF CASH FLOW STATEMENT

-

Question 8

5 / -1

What will be the amount of gross profit of a firm if its average inventory is Rs. 1,60,000, inventory turnover ratio is 6 times, and the selling price is 25% above cost?

Solution

The correct answer is Rs. 2,40,000

Key Points Inventory Turnover ratio:

- The inventory turnover ratio is the number of times a company's inventory has been sold and restocked in a certain period of time.

- This ratio can also be used to determine how long it will take to sell the current inventory.

- A high ratio tends to point to strong sales.

Formula:

Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

Important Points Calculation of gross profit:

Average inventory = Rs. 1,60,000 (Given)

Inventory turnover ratio = 6 times (Given)

selling price is 25% above cost (Given)

Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

6 = Cost of Goods Sold / 160000

Cost of Goods Sold = 1,60,000 x 6

Cost of Goods Sold = 9,60,000

Gross profit = 25% of Cost of Goods Sold

Gross profit = 25% x 960000

Gross profit = 2,40,000

Additional Information Cost of Goods Sold (COGS) - The direct costs of producing goods (including raw materials) to be sold by the company are referred to as COGS.

Average Inventory (AI) - Average inventory smooths out the amount of inventory on hand over two or more specified time periods. (Beginning Inventory + ending inventory) / number of months in the accounting period

-

Question 9

5 / -1

Deep Ltd. issue 1,00,000 7 % debentures of 100 Rs. each at a discount of 4%, redeemable after 5 years at a premium of 6%. Loss issue of debentures is :

Solution

The correct answer is ₹ 10,00,000.

Key Points Debentures – marketable security (a type of Loan) issued by a business or other organization to raise money for long-term activities and growth and yielding a fixed rate of interest. Debentures can be issued at par, at premium and at discount.

Important Points Entry on issue & redemption of debenture -

| Particulars | | Amount Dr. | Amount Cr |

| Debenture Application & Allotment A/c Dr. | (1,00,000 x 96) | 96,00,000 | |

| Loss on Issue of Debentures A/c Dr. | (1,00,000 x 4 + 1,00,000 x 6) | 10,00,000 | |

| To Debentures A/c | (1,00,000 x 100) | | 1,00,00,000 |

| To Premium on Redemption of Debentures A/c | (1,00,000 x 6) | | 6,00,000 |

Hint Loss on Issue of Debentures = amount on discount of issue + amount on premium of redemption.

-

Question 10

5 / -1

Vanya Ltd. forfeited 20,000 equity shares of 100 each for non-payment of first and final call of ₹40 per share. The maximum amount of discount at which these shares can be re-issued will be :

Solution

The correct Answer is12,00,000.

Key Points- Equity shares - Equity shares of a company are the shares in which a shareholder enjoys the fractional ownership of the company. Equity Shareholder receives dividend only when the company earns sufficient profits.

- Calls in Arrears - If the amount is called by the company for allotment or first and subsequent calls, and the shareholder has not paid that amount, it is called Calls in Arrears

- Forfeiture - If AOA (Articles of Association) of a company allows, a company has the power to forfeit shares of those shareholders who have not paid the amount due on Allotment or calls after giving 14 days prior notice to the defaulting shareholder.

Important Points

Discount on Reissue of Forfeited Shares - There can be two cases

- If shares are originally issued at par or at premium - the Maximum amount of discount at which forfeited shares can be re-issued will be the actual amount received by the company from the defaulting shareholder.

- If shares are originally issued at discount - the Maximum amount of discount at which forfeited shares can be re-issued will be the actual amount received by the company from the defaulting shareholder + Discount allowed at the time of issue of share.

Explanation -

- Vanya ltd. received (₹100-₹40) i.e. ₹60 from the defaulting shareholder as ₹40 is calls in arrears.

- The company has forfeited 20000 shares, So the total amount received from defaulting shareholders is 20000\( {\times}\) ₹60 i.e. 12,00,000 which is the maximum amount of discount at which forfeited shares can be re-issued.

-

Question 11

5 / -1

At the time of dissolution of the firm, “Loan of partners” (Loans given by partners to the firm) is paid out of the amount realised on sale of assets :

Solution

The correct answer is After making the payment of loans given by third party.

Key Points Dissolution of a firm- According to Section 39 of the partnership Act 1932, the dissolution of a partnership between all the partners of a firm is called the dissolution of the firm. This brings an end to existing business firm. On dissolution of firm,

- The business of the firm permanently closed.

- The partnership between partners comes to end.

- The books of account are closed.

- All Assets are sold and liabilities are paid-off.

- A firm can be dissolved by the court’s order.

Important Points Steps for payment of Liabilities when Amount realized from assets are paid to:

- Creditors or outsiders or creditors or third party’s debt.

- After payment of creditors any loans or advances of any partner

- And last settlement of partner’s capital account.

Thus, payment of loan of partners will only paid after making the payment of loans given by third party.

-

Question 12

5 / -1

Rohit and Govind were partners in a firm in the ratio of 1 ∶ 2. They admitted Ravi for 1/4 th share in profits. He brought Rs. 2,00,000 for capital but could not bring any amount for goodwill. The goodwill of the firm was valued at Rs. 3,60,000. What Journal Entry will be passed for the treatment of goodwill?

Solution

The correct answer is option 4

Key PointsGoodwill

- Goodwill is the value of a company's reputation earned through time in terms of predicted future profits over and above typical profits.

- Goodwill is an intangible real asset that cannot be seen or felt, but may be bought and sold in real.

Premium for goodwill:

The premium for goodwill is a sum paid by the new partner to compensate the existing partners for the portion of profit that he has acquired.

Important PointsWhen new partner does not bring his share of goodwill in cash:

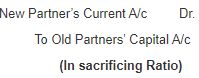

- When a new partner is unable to contribute his share of goodwill in cash, the goodwill account is adjusted through the capital account of the previous partners.

- The new partner's portion of goodwill is debited from his or her Capital Account or Current Account, and the partners who sacrifice their share in favour of the new partner are credited in their sacrificing ratio.

The following Journal entry is passed in the books of accounts.

Therefore, According to the given question

The sacrificing ratio = 1 : 2

(When the share of new or incoming partner is giving without giving the details of the sacrifice made by the old or existing partners. In this case, we will assume that old partners will make the sacrifice in their old profit sharing ratio. Therefore, sacrificing ratio will always be the old profit sharing ratio)

The following Journal Entry will be passed for the treatment of goodwill

| Particulars |

Amount Dr. |

Amount Cr. |

| Ravi's Current A/c Dr |

90,000 |

|

| To Rohit's Capital A/c |

|

30,000 |

| To Govind's Capital A/c |

|

60,000 |

-

Question 13

5 / -1

Main objective of Trend Analysis is

Solution

The correct answer is All of the Above.Key Points Trend Analysis

- Trend analysis determines the direction upwards or downwards and involves the computations in the percentage relationship that each item bears to the same item in the base year for two or more than two years.

- Trend analysis is one of tool of financial statement. In trend analysis, we learn about the behaviour of the same item over a given period like sales in last 5 years and first year considered as a base period. Trend analysis is calculated in % to the base year.

- Trend analysis can be prepared for various items.

Important Points Trend percentage =present year value /base year value x 100

-

Question 14

5 / -1

When debentures are issued as collateral security, which entry has to be passed ?

Solution

The correct answer is Either (1) or (2).Key Points A collateral security is defined as an additional security besides the primary security when a company obtains a loan from a bank or any other financial Institution.

Important Points There are two methods when debentures are issued as collateral security:

1.When company decides not to create liability - No entry will be made in the books of accounts since no liability is created on such issue.

2.When company decides to create liability - Debenture suspense account will be debited on issue of debenture as security.

Entry on issue of debenture as collateral security-

|

Particulars

|

Amount Dr

|

Amount Cr

|

| Debenture Suspense A/c Dr. |

xxxxx |

|

|

To Debentures A/c

|

|

xxxxx

|

-

Question 15

5 / -1

Aman and Bimal are equal partners in a firm. Aman drew regularly Rs. 1,000 at the end of every month. Year is ended on 31st March every year. Calculate interest on drawings @ 6% p.a.

Solution

The correct answer is Rs 330

Key Points

Interest on Drawing : Drawings are the funds taken out by the partners for personal purposes. It's the amount taken out against profit. It is the temporary withdrawal made, which the partners are required to return with interest.

The amount of interest paid by the partners on drawings is determined using the time period for which the money was withdrawn.

It is attributed to the Profit and Loss Appropriation Account since it is a profit for the company.

It is a partner expense, hence it is debited to the Partner's Capital Account.

If it is stated in the Partnership Deed, the partners will be charged interest on the drawing.

Important Points

When equal amounts are withdrawn at the end of every month throughout the year:

Average Period= (no. of months left after first drawings + no. of months left after last drawing)

Average Period = (11+ 0)/2 = 5.5 months

Average Period = (11+0)/2

Interest on drawing = Total Drawings x Rate/ 100 x 5.5/12

Interest on drawing=12000 x 6/100 x 5.5/12 = 330

Hence, Interest on Drawing = 330

Additional Information

Methods of calculating Interest on Drawing

Simple Method :

Interest on drawings is calculated separately on each amount of drawing from the date of drawing to the end of the accounting period under this technique. Formula of this method are as follows:

Interest on Drawing = Amount of Drawings x Rate of Interest /100 x Months / 12

Product Method :

(a) When unequal amounts are withdrawn at unequal interval of time, this method is used.

First, the products are computed by multiplying each set of drawings by its duration. After then, the various products are added together, and interest is calculated on the entire amount of products for one month. The benefit of this system is that it eliminates the need for independent calculations each time. The formula of this method is as follows:

Interest on Drawing = Total of Products * Rate of interest /100 * 1/12

(b) When an equal amount are withdrawn at equal interval of time, then interest on drawing can be calculated by following formula:

Interest on drawing = Total amount of drawings * Rate/100 * Average Period /12

Average Period = (no. of months left after first drawing + no. of months left after last drawings )/2

-

Question 16

5 / -1

If net revenue from operations of a firm are ₹1,20,000; cost of revenue from operations is ₹66,000 and operating expenses are ₹21,600, what will be the percentage of operating income on net revenue from operations?

Solution

The correct answer is 27%.

Important Points Net revenue from operations (net sales) - ₹1, 20,000

Cost of revenue from operations - ₹66,000

Operating expenses - ₹21,600

Operating cost = cost of revenue from operations+ operating expenses

=₹66,000+₹21,600

=₹87,600

Operating ratio= (Operating cost/net sales) x 100

=87600/120000*100

=73%

Operating Profit Ratio = 100 - Operating ratio

=100-73

=27%

Alternate Method Operating profit = net sales –operating expenses

=1,20,000-87,600

=32,400

Operating Profit Ratio= operating profit/ net sales x 100

=32,400/1,20,000*100

=27%

Hint Operating income on net revenue from operations means operating profit.

-

Question 17

5 / -1

On dissolution of a firm, a partner paid 700 for firm’s realisation expenses. Which account will be debited?

Solution

the correct answer is Realisation Account.

Key PointsDissolution of a firm- According to Section 39 of the partnership Act 1932, the dissolution of a partnership between all the partners of a firm is called the dissolution of the firm. This brings end to existing business firm.

Realization expenses – expenses incurred for the process of dissolution of a firm. These expenses can be realized in cash or credit.

Important Points Amount paid by partner for firms realization expenses –

Particulars | Dr. | Cr. |

Realization A/c Dr. | 700 | |

To Partner’s Capital A/c | | 700 |

| (amount of realization expenses paid by partner) | | |

Additional InformationIf realisation expenses paid by partner himself (partner taking responsibility for those) then no journal entry will be made in books of accounts.

-

Question 18

5 / -1

Match the items given in Column I with the headings/subheadings (Balance sheet) as defined in Schedule III of Companies Act 2013.

| Column I | Column II |

| (I) | Creditors | (a) | Intangible fixed assets |

| (II) | trademarks | (b) | Other current assets |

| (III) | Accrued Interest | (c) | Long term Borrowings |

| (IV) | Debentures | (d) | Current Liabilities |

| (V) | Premises | (e) | Tangible Fixed assets |

Choose the correct option:

Solution

The correct answer is (I) - (d), (II) - (a), (III) - (b), (IV) - (c), (V) - (e)

Key Points The correct match is given below:

| Column I | Column II |

| (I) | Creditors | (d) | Current Liabilities |

| (II) | trademarks | (a) | Intangible fixed assets |

| (III) | Accrued Interest | (b) | Other current assets |

| (IV) | Debentures | (c) | Long term Borrowings |

| (V) | Premises | (e) | Tangible Fixed assets |

Important Points Creditors - Current Liabilities

- The term 'creditor' is used in accounting to describe the party who has given a product, service, or loan and is owed money by one or more borrowers. Debts of current creditors are payable within one year. The debts are reported under current liabilities of the balance sheet.

trademarks - Intangible fixed assets

- A trademark is an intangible asset legally preventing others from using a business's logo, name, or other branding. Assets are classified intangible assets, therefore are recorded under Intangible fixed assets in company's balance sheet.

Accrued Interest - Other current assets

- In accounting, accumulated interest is the amount of interest that has accrued on a loan or other financial obligation as of a given date, but has not yet been received yet. It is recorded as Other current assets in balance sheet of company

Debentures - Long term Borrowings

- Bonds or Debentures are debt or loan instruments that are borrowed from the market at a fixed interest rate.

- Bondholders are just concerned with interest repayment; they are unconcerned about the company's revenues or losses.

- They are generally repayable after 12 months.

- These are recorded under Long term Borrowings in balance sheet of company

Premises - Tangible Fixed assets

- Premises refer to the building that the business or owner owns; it usually refers to the location where the business is conducted.

- They are considered as fixed assets and, hence, are recorded under the head of Tangible Fixed assets in company's balance sheet.

-

Question 19

5 / -1

According to the partnership Act, (Sec. 37) the interest payable to the deceased partner on the amount left by him will be:

Solution

The correct answer is 6%

Key PointsRight to Subsequent Profits

As per section 37 of the Indian Partnership Act, 1932, where a partner dies and the surviving partners continue carrying the business of the firm without settling the accounts of the deceased partner, his legal representative has a right to the subsequent profits.

The amount related to the utilisation of his share of the firm's property by a deceased partner or his legal representative in subsequent profits of the firm. Alternatively, he can choose to receive interest at a rate of 6% each year.

Important Points

Section 37 in The Indian Partnership Act, 1932:

Where any member of a firm has died or otherwise ceased to be a partner, and the surviving or continuing partners carry on the business of the firm with the property of the firm without any final settlement of accounts as between them and the outgoing partner or his estate, then, in the absence of a contract to the contrary, the outgoing partner or his estate is entitled at the option of himself or his representatives to such share of the profits made since he ceased to be a partner as may be attributable to the use of his share of the property of the firm or to interest at the rate of six per cent per annum on the amount of his share in the property of the firm:

Provided that whereby in contract between the partners an option is given to surviving or continuing partners to purchase the interest of a deceased or outgoing partner, and that option is duly exercised, the estate of the deceased partner, or the outgoing partner of his estate, as the case may be, is not entitled to any further or other share of profits, but if any partner assuming to act in exercise of the option does not in all material respects comply with the terms thereof, he is liable to account under the foregoing provisions of this section.

-

Question 20

5 / -1

Which of the following is not an item of the Profit and Loss Appropriation Account?

Solution

The correct answer is Interest allowed to Partner Loan

Key Points

- Profit and Loss Appropriation Account is a nominal account which is prepared to show profit and losses which is to be distributed among partners such as interest on drawings, interest on capital, salary, commission, reserves etc.

Important Points

- Interest allowed to Partner Loan is a charge against profits, hence, such interest is allowed whether there are profits or not. It is debited to Profit & Loss A/c and not to Profit and loss Appropriation A/c.

Additional Information

Profit & Loss Account : Profit and Loss Account is prepared to determine net profit or Loss of an organization for a given financial year. Expenses debited to this account are charge against profit and matching principle is used while preparing this account.

Profit & Loss Appropriation A/c : It is prepared after preparation of profit & loss a/c, and it is maintained to distribute the profits to partners. The amount debited to this account are appropriation of profits.

-

Question 21

5 / -1

On dissolution of a firm, its Balance Sheet revealed total creditors 50,000; Total Capital 48,000; Cash Balance 3,000. Its assets were realised at 12% less. Loss on realisation will be :

Solution

The correct answer is 11,400

Key Points

Dissolution of firm:

- The dissolution of a partnership firm is the process of the firm's partners' relationship being dissolved or terminated.

- The term "firm dissolution" refers to the breakup of a partnership between all the business's participants. When a firm's partnership dissolves, the firm ceases to exist.

Important Points Ascertainment of Assets

Total Capital 48,000 (Given)

Total creditors 50,000 (Given)

Capital = Total Assets - Total Liabilities

48000 = Total Assets - 50000

Total Assets = 48000 + 50000 = 98000

Since Cash does not constitute in assets transferred to realisation account

Net assets = 98000 - 3000 = 95000

Assets were realised at 12% less

Therefore,

Loss on realisation = 12% x Net assets

Loss on realisation = 12% x 95000 = 11,400

Loss on realisation will be Rs. 11,400

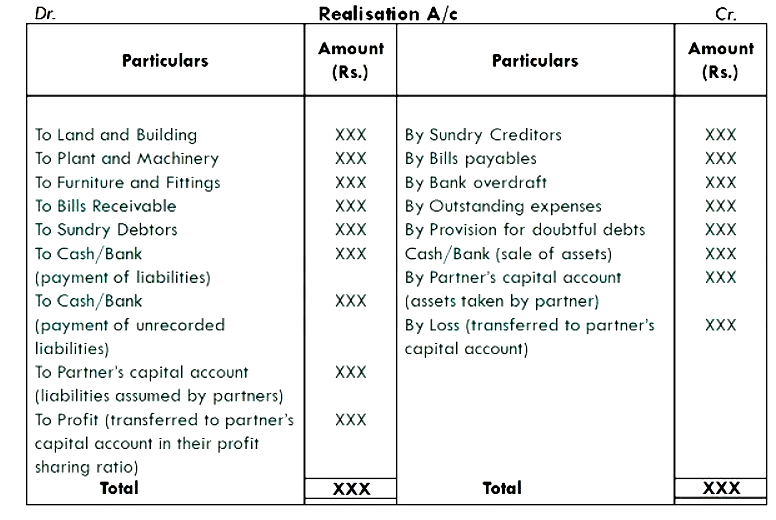

Additional Information Realisation account:

- Realisation account is an account opened during the dissolution of partnership firm.

- The objective of preparation of realization account is to calculate profit or loss on dissolution of partnership firm.

- The transactions related to realization of assets and settlement of liabilities are recorded in this account.

- Excess of credit over debit results in Profit on dissolution of partnership firm and excess of debit over credit results in loss on dissolution of partnership firm.

Following is the specimen of Realisation Account.

-

Question 22

5 / -1

Arun and Vimal are partners in a firm sharing profits and losses in the ratio of 4 ∶ 1.

Balance Sheet (Extract)

| Liabilities | Rs. | Assets | Rs. |

| | | Furniture | 1,20,000 |

If the value of furniture reflected in the balance sheet is undervalued by 40%, find out the value of Furniture to be shown in the Revaluation Account:

Solution

The correct answer is Credit, Rs. 80,000

Key Points

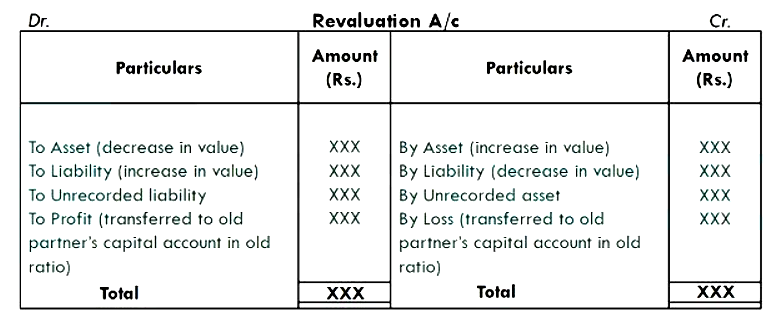

Revaluation account

- A Revaluation Account is created to calculate net profit or loss from revaluation of assets and liabilities, as well as unrecorded items in the books.

- A revaluation account is created when a new partner is admitted, as well as when a partner dies or retires.

- The revaluation profit or loss is transmitted to all partners' capital accounts in their old profit sharing ratio, including deceased or retired partners (PSR).

Important Points According to the question

The value of furniture reflected in the balance sheet is undervalued by 40%. This means that actual value of furniture is higher than what has been reflected in the balance sheet.

So to increase the value of the furniture, the revaluation account must be credited.

The actual value of Furniture is

= 1,20,000 x 100/(100-40)

= 1,20,000 x 100/60

= 2,00,000

Value of Furniture to be shown in the Revaluation Account = 2,00,000 - 1,20,000 = 80,000

Therefore, the Revaluation account must be credited with 80,000.

Additional Information

The journal entry should be

| Particulars | Amount Dr. | Amount Cr. |

| Furniture A/c Dr. | 80,000 | |

| To Revaluation A/c | | 80,000 |

-

Question 23

5 / -1

On dissolution of a firm, unrecorded furniture of the value of 5,000 was taken up by a partner for 4,300. Which Account will be credited and by how much amount? :

Solution

The correct answer is Realisation Account by 4,300

Key Points

Realisation Account:

- The profit gained from the sale of assets and the loss experienced on the settlement of liabilities are recorded in the realisation account, which is opened by the company when it is about to dissolve.

- When a partnership firm dissolves, the account books are closed, and the profit or loss realised on the sale of assets and payment of liabilities is calculated. To do so, a realisation account is created, which identifies the net profit or loss, which is then transferred to all partners' capital accounts in the proportion in which profit and loss are shared.

Important Points Unrecorded assets

Unrecorded assets is an asset, the value of which has been written off in the books of accounts, but the asset is still in usable position.

When the unrecorded asset of Rs. 5000 is taken over by any partner at Rs 4300, the following journal entry is passed

| Particulars |

Amount Dr. |

Amount Cr. |

| Partner's Capital A/c Dr. |

4300 |

|

| To Realisation A/c |

|

4300 |

-

Question 24

5 / -1

In a common size Statement of Profit & Loss, the amount of net revenue from operations is assumed to be equal to

Solution

The correct answer is 100

Key Points Common Size Statement

- A common size statement is a type of financial statement analysis and interpretation.

- It is also called Vertical Analysis.

- This method examines financial statements by calculating each line item as a percentage of the base amount for the accounting period in question.

Important Points Common Size Statement of Profit & Loss

This is a common size statement in which the sales/Revenue from operations are used as the starting point for all calculations. As a result, each line item's computation will use sales as a starting point (considered as 100), and each item will be expressed as a percentage of sales.

-

Question 25

5 / -1

At the time of reconstitution of partnership firm, what will be the effect of the following information?

Balance in Workmen Compensation Reserve: Rs. 40,000.

Claim for Workmen Compensation: Rs. 45,000.

Solution

The correct answer is ₹5,000 Debited to Revaluation Account.

Key Points Workmen Compensation Reserve:

- Workmen Compensation Reserve is a fund set aside from a company's profits to cover the possibility of having to pay compensation to employees in the future.

- It signifies that a claim could emerge or not. It also suggests that the claim could be more than the reserve.

- The Treatment of Workmen Compensation Reserve, which represents compensation due to employees, is an external responsibility, while any remaining balance, if any, is an internal liability due to partners.

Important Points Accounting Treatment for Workmen Compensation Claim:

Balance in Workmen Compensation Reserve: Rs. 40,000.

Claim for Workmen Compensation: Rs. 45,000.

As the claim for Workmen Compensation is Rs. 5000 higher than the balance in Workmen Compensation Reserve, the excess Rs. 5000 is the loss. Therefore, it is transferred to Revaluation account.

Hence, ₹5,000 Debited to Revaluation Account.

-

Question 26

5 / -1

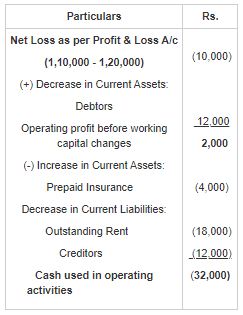

Compute the cash flow from operating activities from the following details by the indirect method:

| Particulars |

2021

Rs.

|

2020

Rs.

|

|

Profit and Loss A/c

Debtors

Outstanding Rent

Goodwill

Prepaid Insurance

Creditors

|

1,10,000

50,000

24,000

80,000

8,000

26,000

|

1,20,000

62,000

42,000

76,000

4,000

38,000

|

Solution

The correct answer is (32,000).

Key Points Cash Flow Statement:

A cash flow statement is a financial statement that shows the total amount of money coming in and going out. In other terms, a cash flow statement is a financial statement that estimates the amount of cash generated or utilised by a company over a given period of time.

Elements of the Cash Flow Statement

- Cash flow from operating activities

- Cash flow from investing activities

- Cash flow from financing activities

Important Points

Cash Flow from Operating Activities:

- The operations of a firm directly engaged with providing its commodities and services to the marketplace are known as operating activities.

- Producing, assigning, selling, and promoting a good or service are examples of the enterprise's primary trading pursuits.

- Operating activities are a company's primary source of revenue and expenditure.

Calculation of cash flow from operating activities (Indirect Method)

Working Note: 4,000 have been paid for the purchase of a fixed asset, i.e., goodwill. It will not be considered while computing cash from operating activities because the purchase of fixed asset does not affect cash from operating activities. It will be taken into consideration while calculating the net cash flow from investing activities.

Cash used in operating activities = Net Loss as per Profit & Loss A/c + Decrease in Current Assets - Increase in Current Assets - Decrease in Current Liabilities.

-

Question 27

5 / -1

In the Balance Sheet of a Common Size Statement

Solution

The correct answer is Figure of total assets is assumed to be 100

Key Points

Common Size Statement

- A common size statement is a type of financial statement analysis and interpretation.

- It is also called Vertical Analysis.

- This method examines financial statements by calculating each line item as a percentage of the base amount for the accounting period in question.

Important Points Common Size Balance Sheet

- The total assets value is typically used as the base value (considered as 100) in the balance sheet common size analysis.

- The value of total assets on the balance sheet equals the value of total liabilities and shareholders' equity.

- The common size analysis is used by a financial management or investor to compare a company's capital structure to that of competitors.

- They can draw key conclusions by comparing individual line items to the total assets.

-

Question 28

5 / -1

If Total sales is Rs. 50,000 and credit sales is 25% of Cash sales. The amount of credit sales is:

Solution

The correct answer is 10,000

Important Points Let cash sales = x

Credit sales is 25% of Cash sales

Credit sales = 25% of x

Total sales = Cash sales + credit sales

50000 = x + 25% of x

50000 = 125% of x

x= 50000 x 100/125

x = 40000

cash sales = x = 40000

Credit sales = 50,000 - 40,000 = 10,000

-

Question 29

5 / -1

On dissolution of a firm, partners’ capital accounts balance was 63,000; creditors balance was 12,000 and profit & loss account debit balance was 6,000. Profit on realisation of assets was 7,800. The total amount realized from assets was:

Solution

The correct answer is Rs. 76800

Key Points

Dissolution of firm:

- The dissolution of a partnership firm is the process of the firm's partners' relationship being dissolved or terminated.

- The term "firm dissolution" refers to the breakup of a partnership between all the business's participants. When a firm's partnership dissolves, the firm ceases to exist.

Important Points

Calculation of Total assets

Total Assets = Total Liabilities + Total Capital

Total Assets = 12000 + (63000 - 6000)

Total Assets = 69000

Calculation of total amount realised from assets

Total amount realised from assets = Total Assets + Profit on realisation of assets

Total amount realised from assets = 69000 + 7800 = 76800

The total amount realised from assets was Rs. 76800

-

Question 30

5 / -1

A firm's profits for the last three years are Rs. 5,00,000 Rs. 4,00,000 and Rs. 6,00,000. Calculate value of firm's goodwill based on four years' purchase of the average profits for the last three years:

Solution

The correct answer is 20,00,000

Important Points

Average profits = Sum of Profits of last 3 years/ 3

Average profits = (500000 + 400000 + 600000)/ 3

Average profits = 1,50,000 / 3

Average profits = ₹5,00,000

Value of Goodwill = Average profit x Number of Years Purchase

Value of Goodwill = 5,00,000 x 4

Value of Goodwill = ₹20,00,000

Key Points Goodwill:

- Goodwill is the value of a company's reputation earned through time in terms of predicted future profits over and above typical profits.

- Goodwill is an intangible real asset that cannot be seen or felt but may be bought and sold in reality.

-

Question 31

5 / -1

In case of issue of debentures as a collateral security for loan from the bank which account will be debited :

Solution

The correct answer is Debentures Suspense Account

Key Points Debentures:

- A debenture is a written instrument that accepts a debt under the enterprise's general certification.

- It includes an agreement for the repayment of principal after a set amount of time, at intervals, or at the enterprise's discretion, as well as the payment of interest at a specified rate, usually yearly or half-yearly on fixed dates.

- According to section 2(30) of the Companies Act, 2013, a 'debenture' is defined as: Debenture Inventory, Bonds, and any other securities of a company, whether or not they include a charge on the enterprise's assets.

Important Points Issue of Debentures as Collateral

- Debentures offered as collateral security serve as a backup or supplement to the company's original loan.

- If the borrower fails to repay the original loan, the lender can seize the collateral security.

There are the following two methods for recording this kind of debentures:

- Method 1: The company makes no entry when issuing these debentures using this manner. It reveals them in the 'Notes to Accounts' section of the Balance Sheet as a note under the liability secured by the issue of debentures and outstanding.

- Method 2: Under this method, a journal entry to record the issue of such debentures:

- Debentures Suspense A/c Dr

To Debentures A/c

In the second case, we will show the debentures account on the liabilities side of the Balance Sheet. While we will show the Debentures Suspense A/c on the assets side of the Balance Sheet under Other Non-Current Assets.

Additional Information Collateral Security:

Collateral is a term used to describe an asset that a lender accepts as security for a loan. Collateral may take the form of real estate or other kinds of assets, depending on the purpose of the loan.

-

Question 32

5 / -1

At the time of admission of new partner Z, Old partners X and Y had debtors of Rs. 3,20,000 and a provision for doubtful debts of Rs. 20,000 in their books. As per terms of admission, assets were revalued, and it was found that debtors worth Rs. 18,000 had turned bad and hence should be written off. Which journal entry reflects the correct accounting treatment of the above situation.

(A) | Bad Debts A/c | Dr. | 18000 | |

To Sundry Debtors | | | 18000 |

Provision for Doubtful Debts A/c | Dr. | 18000 | |

To Bad Debts A/c | | | 18000 |

(B) | Bad Debt A/c | Dr. | 18000 | |

To Sundry Debtors | | | 18000 |

Revaluation A/c | Dr. | 18000 | |

To Provision for Doubtful Debts A/c | | | 18000 |

(C) | Revaluation A/c | Dr. | 18000 | |

To Sundry Debtors A/c | | | 18000 |

(D) | Bad Debts A/c | | | |

Dr. To Revaluation A/c | | | 18000 |

Solution

The correct answer is option A. Key Points

Provision for Doubtful Debts :

- Provision for doubtful debts is established as a safeguard against bad debt.

- According to the company's credit policy and other information, a proportion is set aside as a provision for various debtors.

Important Points

In this question sundry debtor balance is 3,20,000 and provision for doubtful debt is 20,000, but after admission of new partner bad debts occurred 18,000, and it should be written off. So, firstly journal entry will be passed for the bad debt occurred and later entry will be passed for writing off.

| Particulars | | Amount Dr. | Amount Cr. |

| Bad debts A/c | Dr. | 18,000 | |

| To Sundry Debtors A/c | | | 18,000 |

| (Bad Debts Recorded) | | | |

| Provisions for Doubtful Debts A/c | Dr. | 18,000 | |

| To Bad Debts A/c | | | 18,000

|

| (Bad Debts Written off) | | | |

-

Question 33

5 / -1

The profit amount received for sale of old sports materials by a Non-profit organisation is shown in which of the following?

Solution

The correct answer is Credit side of Income and Expenditure Account

Key Points

Non-profit-organisation:

- Not-for-profit organisations are those that are established for the benefit of society or to promote art and culture in society.

- These are usually established as a philanthropic organisation with a service mission.

- These organisations are managed by trustees. The trustees are chosen by the members of the organisation.

- Non-profit organisations raise donations from their members as well as the wider public to achieve their goals.

- These organisations' primary goal is to give service.

- These organisations do not typically create, purchase, sell, or provide services.

- As a result, they are relieved of the necessity to compile trading and profit and loss accounts. They deposit the money in the Capital Fund or the General Fund A/c.

Not-for-profit organisations must also prepare final accounts or financial statements according to accounting rules at the conclusion of the accounting year. These financial statements consist of :

- Receipt and Payment A/c : The account statement is a summary of all cash and bank transactions. It aids in the preparation of the income and expense account as well as the balance sheet. We must also file it with the Registrar of Societies, along with the Income and Expenditure Account and the Balance Sheet.

- Income & Expenditure A/c : It is comparable to the Profit and Loss A/c in that it determines if there is a surplus or deficit.

- Balance Sheet : We prepare it in the same way that profit-oriented enterprises construct their balance sheets.

Important PointsThe profit amount received for sale of old sports materials by a Non-profit organisation is income for the firm, which is shown on credit side of Income & Expenditure Account.

-

Question 34

5 / -1

From the following information, calculate net increase in cash and cash equivalents:

Net Cash from operating activities - 4,800

Net Cash from investing activities - 2,000

Opening balance of equity share capital - 80,000

Closing balance of equity share capital - 90,000

Opening balance of 12% preference share capital - NIL

Closing balance of 12% preference share capital - 10,000

Interest paid on Debentures - 1800

Solution

The correct answer is 25,000

Important Points

Net Cash from operating activities - 4,800 (A)

Net Cash from investing activities - 2,000 (B)

Cash flow from financing activities:

Cash proceeds from issue of Equity Shares - 10,000 (i)

Cash proceeds from issue of 12% Preference Shares - 10,000 (ii)

(-) Interest on Debentures Paid - (1800) (iii)

Net Cash from financing activities (i + ii - iii) - 18,200 (C)

Net increase in cash & cash equivalents (A + B + C) - 25,000

Key Points

- Investing activities refer to earnings or expenditures on long-term assets, such as equipment and facilities.

- Financing activities are the cash flows between a company and its owners and creditors from activities such as issuing bonds, retiring bonds, selling stock or buying back stock.

- Investing activities include purchases of physical assets, investment in securities, or the sale of securities or assets.

- However, negative cash flow from investing activities might be due to significant amounts of cash being invested in the long-term health of the company, such as research and development.

- Net increase in cash & cash equivalents = Net Cash from operating activities + Net Cash from investing activities + Net Cash from financing activities.

-

Question 35

5 / -1

At the time of admission, if the profit-sharing ratio among the old partners does not change then sacrificing ratio will be:

Solution

The correct answer is their old profit - sharing ratio.

Important Points At the time of admission, sacrificing ratio is calculated using the following formula, i.e.,

Sacrificing Ratio = Old Ratio - New Ratio

In the given question, the profit sharing ratio of old partners does not change which means ( old ratio - new ratio ) = zero, means sacrificing ratio is null.

Hence, there is no sacrifice made by the old partners and that's why the profit sharing ratio will remain same even the new partner is admitted.

Additional Information Sacrificing Ratio : The sacrificing ratio is calculated when a new partner is admitted. It is the portion where the old partners sacrifice their share to the new partner.

For Example : X, Y and Z are partners in a firm sharing profit in the ratio 5:3:2 . They admitted A into partnership. The new profit sharing ratio is 3: 2: 2: 3. Calculate sacrificing ratio.

Sacrificing Ratio = old ratio - New ratio

X will sacrifice 5/10 - 3/10 = 2/10

Y will sacrifice 3/10 - 2/10 = 1/10

Z will sacrifice 2/10 - 2/10 = 0

hence, sacrifice ratio of X and Y = 2: 1.

-

Question 36

5 / -1

High price to earning ratio shows company's

Solution

The correct answer is High Growth prospect.

Important Points High price to earning ratio shows the company's High growth prospect , because growth stocks are frequently defined as companies having a high Price Earnings Ratio. This indicates that future performance will be favourable, and investors will be prepared to pay more for future earnings growth.

Additional Information Price/ Earning Ratio :This ratio indicates how much money should be invested in this company's stock in order to achieve a profit on each share. The ratio is used to determine whether a stock's market price is high or low. It is computed by dividing the market price of an equity share by the earning per share.P. E. Ratio = Market Price of the equity share / Earning Per Share ( E.P.S.)

For Example : If the EPS of X ltd. is Rs. 10 and market price is Rs. 100, the price earning ratio will be 10 (100/10). It reflects investors expectation about the growth in the firm's earnings and reasonableness of the market price of its shares. P/E Ratio vary from industry to industry and company to company in the same industry depending upon investor's perception of their future.

-

Question 37

5 / -1

Rahim, Ram and Robert are partners sharing profits and losses in the ratio 5 ∶ 4 ∶ 1. Rahim guaranteed a minimum profit of Rs. 25,000 to Robert. The profit of the firm for the year ending 31st March, 2021 was Rs. 1,42,000. Rahim share in the profits of the firm will be:

Solution

The correct answer is 60200

Key Points Guarantee of Profit to a Partner:

- Guarantee means the assurance of a specific amount of profits by one or more partners, and in some situations, the firm, with the burden of guarantee borne by the person offering the guarantee.

- In other words, it is a set amount that must be paid by the partner who is provided such a guarantee.

- If the actual share in profits is less than the guaranteed amount, then the deficit amount shall be borne either by the firm or by any partner, as the case may be.

- If the actual share in profits is more than the minimum guarantee amount, then the firm will provide the actual profits to the partner.

Important Points Since the guarantee is provided by Rahim to Robert, all the deficiency in profit to Robert shall be borne by Rahim alone.

| Particulars | Rahim | Ram | Robert |

| Profit Sharing Ratio | 5/10 | 4/10 | 1/10 |

| Actual Profit shared | 71000 | 56800 | 14200 |

| Minimum Guarantee to Robert | | | 25000 |

| Deficiency borne by Rahim | (10800) | | 10800 |

| Final share of profit | 60200 | 56800 | 25000 |

Therefore, the final share of Rahim = Rs. 60,200

Working note:

Deficiency borne by Rahim = Robert's minimum guarantee - Actual share of Robert

Deficiency borne by Rahim = 25000 - 14200 = 10800

-

Question 38

5 / -1

Comparative statements are also known as :

Solution

The correct answer is Horizontal Analysis.

Key PointsComparative Statements:

- The most frequent method for examining financial statements is to prepare comparative financial statements. This method compares financial accounts for two or more time periods to determine a company's profitability and financial situation.

- As a result, this method is also known as Horizontal Analysis.

- To conduct such an examination, income statements and balance sheets are often created in a comparative format.

Additional Information Comparative Statement :

- Comparative statements, often known as comparative financial statements, are statements of a company's financial situation over time.

- By comparing financial data from two or more accounting periods, these statements aid in determining the profitability of a corporation.

- The benefit of such an analysis is that it allows investors to spot business patterns, track a company's success, and compare it to that of competitors.

- Only when the financial data is prepared using the same set of accounting rules will the financial data be considered comparable.

Horizontal Analysis:

- It refers to the comparison of an item of the financial statement of one period to its corresponding item of the base accounting period.

- In horizontal analysis, change in the items is expressed either in absolute figures or in percentage or in both terms.

- Its purpose is to determine the change in an item during an accounting period

Vertical Analysis:

- It refers to the comparison of items of the financial statement to the common item of the same accounting period.

- In vertical analysis, change in item is shown either in ratio form or percentage form.

- Its purpose is to determine the proportion of items to the common item of the same accounting period.

-

Question 39

5 / -1

A company’s working capital is Rs.10 Lakh (negative balance) in the year 2018. It became Rs.15 Lakh (positive balance) in the year 2019. What is the percentage of change?

Solution

The correct answer is 250%.

Important Points

In above question, a company's working capital of two year is given i.e.,

In 2018, the working capital is 10,00,000 (negative balance)

In 2019, the working capital is 15,00,000

So, for calculating the percentage of change, firstly difference is to be calculated:

Difference = 15,00,000 - (- 10,00,000)

= 15,00,000 + 10,00,00 = 25,00,000

hence, the difference is 25,00,000

Percentage Change = (25,00,000 / 10,00,000 )x 100

= 250 %

Hence, the answer is 250%.

Key Points Working capital:

- Working capital or current capital is the capital invested in current or working assets such as stock of materials and finished goods, accounts receivable, bills receivable, short-term securities, and cash or bank balance to cover day-to-day expenses.

- It signifies an investment for a limited time.

- Working capital = Current Asset – Current Liabilities

-

Question 40

5 / -1

A and B are partners in a firm having capitals of Rs. 15,000 each. C is admitted for 1/3 share, for which he has to bring Rs. 20,000 for his share of capital. The amount of goodwill of the firm will be

Solution

The correct answer is Rs. 10,000

Key Points Case of Hidden Goodwill:

- The value of goodwill that is not specified at the time of a partner's admission is referred to as hidden goodwill.

- If the new partner requires bringing a portion of the company's goodwill, we must assess the value of the company's goodwill.

- The difference between the capitalized value of the firm and the net worth of the firm is treated as the value of Hidden Goodwill.

- This is not given in question, but is implied from brought in capital by the new partner for his share in the firm.

- Value of Goodwill = Capitalised Value of Firm – Net Worth

Important Points

Capitalised Value of Firm = C’s Capital × Reciprocal of his Share

Capitalised Value of Firm = 20,000 × 3/1

Capitalised Value of Firm = 60,000

Net Worth = Total Capital (including C’s Capital)

Net Worth = 15,000 + 15,000 + 20000

Net Worth = 50,000

Value of Goodwill = Capitalised Value of Firm – Net Worth

Value of Goodwill = 60,000 - 50,000 = 10,000

The amount of goodwill of the firm will be 10,000

-

Question 41

5 / -1

Discount on issue of Debentures is in the nature of:

Solution

The correct answer is Capital Loss.

Important Points

- The shortage amount is known as discount on issuance of debentures when debentures are issued at a lower price than the nominal value.

- Suppose, debenture of nominal value of Rs. 100 is issued at discount rate of 10% which is Rs. 10.

- Hence, Rs 10 is discount on issue of debenture, which is capital loss to the company that's why it should be shown on asset side of balance sheer as "Miscellaneous Expenditure" as fictitious assets.

Key Points Capital Loss:

- When the value of a capital asset, such as an investment or real estate, drops, a capital loss occurs.

- This loss will not be realised until the asset is sold for less than it was originally purchased for.

- A capital loss is the difference between the asset's purchase price and its selling price, where the latter is lower. For example, if an investor buys a house for Rs 25 lakh and sells it for Rs 20 lakh five years later, the investor loses Rs 5 lakh in capital.

Additional Information

Revenue Loss : When a company's revenue is less than predicted owing to external and internal variables, revenue loss occurs. Potential client loss, business constraints, and market shifts might all result in severe income loss.

Abnormal Loss: The loss suffered by a corporation that exceeds the regular/normal loss threshold is referred to as abnormal loss. In other words, it is a loss that a corporation suffers that is more than the regular loss that is expected to occur.

Deferred Revenue Expenditure : Deferred revenue expenditures are expenses that will be made in the current accounting period, but whose benefits will be spread out over subsequent accounting periods. For example, Expenditure on marketing for the debut of a new product.

-

Question 42

5 / -1

A and B contribute Rs. 1,00,000 and Rs. 60,000 respectively in a partnership firm by way of capital on which they agree to allow interest @ 8% p.a. Their profit and loss sharing ratio is 3 ∶ 2. The profit at the end of the year was Rs. 2,800 before allowing interest on capital. If there is a clear agreement that interest on capital will be paid even in case of loss, then B's share will be:

Solution

The correct answer is Loss Rs. 4,000.

Key Points In this question, it is given that in agreement it is clearly mentioned that interest on capital will be paid even in case of loss, it means interest on capital will be treated as ''Charge against Profit".

Hence, for calculating interest on capital P&L A/c will be prepared which are as follows:

P&L A/C

| Particulars | Amount | Particulars | Amount |

To interest on capital ; A: 1,00,000*8/100 B: 60,000*8/100 | 8,000 4,800 12,800 | By Profit for the year By Loss transferred to: A's capital A/c B's capital A/c | 2,800 6,000 4,000 12,800 |

Working Note:

Profit for the year is given in the question, i.e., 2,800

and, interest on capital is calculated according to the given rate i.e., 8%

but there is difference on credit side of Rs 10,000 i.e., loss, and it will be distributed according to the profit and loss sharing ratio which is given in the question i.e., 3 : 2

Hence, loss transferred to A's capital a/c = 10,000*3/5 = 6,000

Loss transferred to B's capital A/c = 10,000* 2/5 = 4,000.

-

Question 43

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) : Goods costing ₹8,000 are sold for ₹10,000 and it will reduce stock by ₹10,000.

Reason (R) : The value of stock would be reduces by ₹8,000.

In the context of the above two statements which of the following is correct ?

Solution

The correct answer is Assertion (A) is false, but Reason (R) is true.

Key Points

- Stock- Stock or inventory are the goods which are available for sale. Some stocks are also used by the company for further production as a raw material.

- As Per AS2 Inventory should be valued at lower of cost and net realizable value.

Important Points

In the given question cost of goods sold is 8000 and selling price is 10000. So in inventory we will record as 8000 as the lower of the two.

As the goods are sold, so the inventory will be reduced by 8000

The Assertion is false because the inventory will be reduced by 8000 and The Reason is True

-

Question 44

5 / -1

Cash flow arising from interest paid in case of a financial enterprise is a cashflow from

Solution

Cash flow refers to an increase or decrease in the amount of money a business or institution has. In financial terms, it is used to describe the amount of cash that is generated or consumed in a given time period.

Operating activities:

- Cash flow from operating activities indicates the amount of money a company brings in from its daily, ongoing business activities like manufacturing and selling products or providing services to a customer.

- It does not include long-term capital expenditures or investment revenue or expense.

- It focuses only on the core business and is also known as operating cash flow (OCF) or net cash from operating activities.

- In the case of a financial enterprise, cash flow arising from interest paid and interest & dividend received is a cash flow from operating activities.

- There are two methods for depicting cash from operating activities on a cash flow statement: the indirect method and the direct method.

Therefore, cash flow arising from interest paid in the case of a financial enterprise is a cash flow from operating activities.

Financing activities:

- Cash flow from financing activities indicates the company's cash flow statement that shows the net flow of cash that is used to fund the company.

- The financing activities include transactions involving debt, equity, and dividends.

- The debt and equity financing are reflected in the cash flow from the financing section that varies with different capital structures, dividend policies, or debt terms that companies may have.

Investing activities:

- Cash flow from investing activities indicates the company's cash flow statement that reports how much cash flows have been done relating to investment activities in a specific period.

- It includes purchase or sale of assets, purchase or sale of securities, etc.

- Negative cash flow indicates the company's poor performance but it might be due to a significant amount of money invested in the long-term health of the company.

-

Question 45

5 / -1

In the absence of partnership deed, a partner is entitled to an interest on the amount of opening capital introduced by him in the firm at a rate of:

Solution

The correct answer is not entitled for any interest on their capitals.

Key Points According to Indian Partnership Act 1932, no interest on capitals shall be allowed to the partners. If there is provision regarding interest on capitals in the partnership deed, it will be allowed only when there is profit.

Important Points According to Indian Partnership Act 1932, there are provisions relating to interest on capital which are as follows:

Case 1: When the partnership deed is silent about the interest on capital, then no interest will be allowed on capital.

Case 2: When the partnership deed provides for interest on capital but is silent in treating as a charge or appropriation then interest on capital will be allowed only when there is profit in the firm.

Case 3: When the partnership deed provides for treating interest as a charge, then full interest will be allowed whether there is profit or loss in the firm.

-

Question 46

5 / -1

Subscription received in cash during the year amounted to ₹60,000; subscription received in advance for next year was ₹3,000 and received in advance during the previous year was ₹2,000. Subscription in arrears at the end of the current year was ₹5,400. The amount credited to Income & Expenditure Account will be :

Solution

The correct answer is ₹64,400

Key Points Income & Expenditure Account:

- Non-trading entities prepare an income and expenditure account to determine whether there is a surplus or deficit of income over expenses for a given time period.

- The accumulated or accrual concept of accounting is rigidly pursued while preparing income and expenditure a/c of non-trading concerns.

- It is prepared as a portion of final accounts of non-trading entities and is equal to the profit and loss account outlined by for-profit business entities.

Format of Income and Expenditure account:

Important Points Calculation of amount of Subscription:

| Particulars |

Amount |

| Subscription Received during the year |

60000 |

| Less: Advance for next year |

(3000) |

| |

57000 |

| Add: Subscription received in Previous year |

2000 |

| |

59000 |

| Add: Subscription in arrears at the end of the current year |

5400 |

| Amount of Subscription credited to Income & Expenditure Account |

64,400 |

-

Question 47

5 / -1

The following information are given:

Trade Receivables Turnover Ratio: 8 times

Average Debtors: 3,60,000

Cash Revenue from Operations: 25% of Revenue from Operations.

What is the revenue from operations?

Solution

The correct answer is

Key Points Trade Receivables Turnover Ratio:

- The trade receivables turnover ratio, also known as the accounts receivable turnover ratio or the debtors turnover ratio, is a crucial accounting number.

- It is used to assess the efficiency with which the company manages the credit it extends to its customers and how long it takes the company to collect the outstanding debt within the accounting period.

- A high receivables turnover ratio shows that the company's collection method is extremely effective, and that the company has a high proportion of customers that pay their bills fast in order to avoid debt collection.

- Low receivables, on the other hand, suggest that the company lacks a clear collection process as well as a defined credit policy.

Trade Receivables Turnover Ratio Calculation

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

Important Points Trade Receivables Turnover Ratio: 8 times (Given)

Average Debtors: 3,60,000 (Given)

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

8 = Net Credit Sales / 360000

Net Credit Sales = 28,80,000

Cash Revenue from Operations = 25% of Revenue from Operations.

Therefore, Net credit Revenue from Operations = 100-25 = 75% of Revenue from Operations

Net credit Revenue from Operations = 75% of Revenue from Operations

28,80,000 = 75% of Revenue from Operations

Revenue from Operations = 28,80,000 x 100/75

Revenue from Operations = 38,40,000

-

Question 48

5 / -1

R and S are partner, sharing profit & losses equally. They Admitted K as new partner for \(\frac{1}{4}\)th share in profit. On this occasion, Goodwill of the firm valued at Rs. 1,20,000 and K brought Rs. 60,000 for his capital and Rs. 20,000 for goodwill in cash. What entry will be passed for the receipt of capital and goodwill at the time of admission-

|

Option

|

Particulars

|

|

L.F.

|

Amount (Rs.)

|

Amount (Rs.)

|

|

(A)

|

Cash A/c

|

Dr.

|

|

80,000

|

|

|

To K's Capital A/c

|

|

|

|

80,000

|

|

(B)

|

Bank/Cash A/c

|

Dr.

|

80,000

|

|

|

|

To Premium for Goodwill A/c

|

|

|

|

20,000

|

|

To K's Capital A/c

|

|

|

|

60,000

|

|

(C)

|

Cash A/c

|

Dr.

|

|

90,000

|

|

|

To Premium for Goodwill A/c

|

|

|

|

20,000

|

|

To K's Capital A/c

|

|

|

|

60,000

|

|

To K's Current A/c

|

|

|

|

10,000

|

|

(D)

|

No Entry

|

|

|

|

|

Solution

The Correct answer is Option 2

Key Points

Goodwill

- Goodwill is the value of a company's reputation earned through time in terms of predicted future profits over and above typical profits.

- Goodwill is an intangible real asset that cannot be seen or felt, but may be bought and sold in real.

Premium for goodwill:

The premium for goodwill is a sum paid by the new partner to compensate the existing partners for the portion of profit that he has acquired.

Important Points

When new partner brings a part of his share of goodwill in cash:

- When a new partner is brings a part of his share of goodwill in cash, the goodwill account is adjusted through the capital account of the previous partners.

- Premium for goodwill account is credited only with the amount of goodwill brought in cash.

- The new partner's remaining portion of goodwill is debited from his or her Capital Account or Current Account, and the partners who sacrifice their share in favour of the new partner are credited in their sacrificing ratio.

The following Journal entry is passed in the books of accounts.

On the receipt of goodwill and capital

Therefore, According to the given question

On the receipt of goodwill and capital

| Particulars |

Amount Dr. |

Amount Cr. |

| Bank/Cash A/c Dr |

80,000 |

|

| To Premium for Goodwill A/c |

|

20,000 |

| To K's Capital A/c |

|

60,000 |

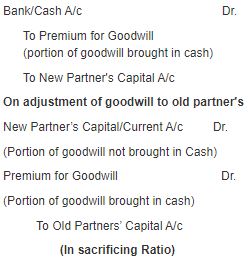

On adjustment of goodwill to old partner's

| Particulars |

Amount Dr. |

Amount Cr. |

| Premium for Goodwill A/c Dr |

20,000 |

|

| K's Capital/Current A/c Dr. |

10,000 |

|

| To R's Capital A/c |

|

15,000 |

| To S Capital A/c |

|

15,000 |

Additional Information Working Note:

K's Share in goodwill =Total Firm's Goodwill x K's Share

K's Share in goodwill =1,20,000 x 1/4

K's Share in goodwill = 30,000

Since new Profit sharing ratio is not given, Sacrificing ratio will be equal to old ratio

-

Question 49

5 / -1

A and B are partners in a partnership firm without any agreement. A has given a loan of ₹50,000 to the firm. At the end of the year, a loss was incurred in the business. The following interest may be paid to A by the firm :

Solution

The correct answer is 6% p.a.

Key Points According to Indian Partnership Act 1932, Interest at the rate of 6% p.a. is to be allowed on loan to the firm. Such interest shall be paid to the Partner's Loan even if there are losses to the firm, because it is treated as ''Charge against profit''.

Important Points Interest on Loan : According to provisions of Indian Partnership Act 1932, if any partner apart from his share capital advances money to the firm as loan, he is entitled to interest on such amount at the rate of 6 %, because it is treated as Charge Against Profit. Even if there is absence of partnership deed, it is to be paid to the partners.

Additional Information

Charge against Profit : In Accounting, charge against profit means the expenses that have to pay whether there is profit or loss.

-

Question 50

5 / -1

Shares can be forfeited:

Solution

The correct answer is For non-payment of call money

Key Points Share Forfeiture:

- The situation in which the allotted shares are cancelled by the issuing firm due to the shareholder's failure to pay the subscription amount as asked by the issuing company is known as forfeiture of shares.

- If shares are forfeited, the shareholders lose their rights and interests as shareholders and are no longer members of the organisation.

Important PointsAccounting Entries on Forfeiture of Share

Case 1: When Forfeiture of shares Issued at Par

| Particulars | Amount Dr. | Amount Cr. |

Share Capital A/c Dr.

(Called up amount) | xxxx | |

To Share Forfeiture A/c

(Paid-up amount) | | xxxx |

| To Share Allotment A/c | | xxxx |

To Share Calls A/c

(individually) | | xxxx |

| (shares forfeited for non–payment of allotment money and calls made) |

Case 2: Forfeiture of Shares issued at Premium

(a) Securities Premium amount has been received

| Particulars | Amount Dr. | Amount Cr. |

Share Capital A/c Dr.

(Called up amount) | xxxx | |

To Share Forfeiture A/c

(Paid-up amount) | | xxxx |

| To Share Allotment A/c | | xxxx |

To Share Calls A/c

(individually) | | xxxx |

| (shares forfeited for non–payment of allotment money and calls made) |

(b) Securities Premium amount has not been received

| Particulars | Amount Dr. | Amount Cr. |

Share Capital A/c Dr.

(Called up amount) | xxxx | |

| Security Premium A/c Dr. | xxxx | |

To Share Forfeiture A/c

(Paid-up amount) | | xxxx |

| To Share Allotment A/c | | xxxx |

To Share Calls A/c

(individually) | | xxxx |

| (shares forfeited for non–payment of allotment money and calls made) |

Note: According to the Section 53 of Companies Act, 2013, a company is prohibited to issue shares at a discount

×

×

Sign in

Sign in

Profile

Profile Signout

Signout