-

Question 1

5 / -1

Current accounts of partners are maintained under which method?

Solution

The current answer is Fixed Capital method

Key Points Partners Capital Account -A partners capital account is a separate account that indicates the equity that is owned by specific partners in a partnership.There are two methods by which the capital accounts of partners can be maintained. These are

Key Points Partners Capital Account -A partners capital account is a separate account that indicates the equity that is owned by specific partners in a partnership.There are two methods by which the capital accounts of partners can be maintained. These are

- Fixed Capital Method

- Fluctuating Capital Method

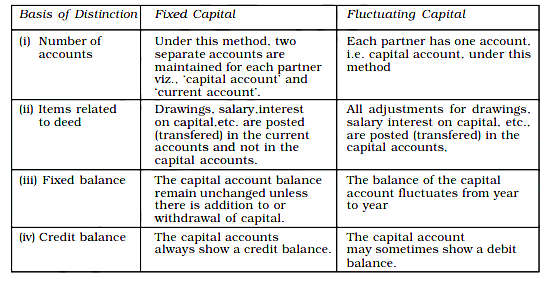

Important PointsFixed Capital Method: Two accounts are maintained i.e capital account & current account for each partners.

Important PointsFixed Capital Method: Two accounts are maintained i.e capital account & current account for each partners.

- In capital account - fixed capital unless their capital introduced and capital withdraw are recorded.

- In current account - share of profit or loss, interest on capital, drawings, interest on drawings, etc. are recorded in a separate accounts, called Partner’s Current Account.

Fluctuating Capital Method: Under the fluctuating capital method, only one account, i.e. capital account is maintained for each partner.

Thus, Current accounts of partners are maintained under Fluctuating Capital method.

Additional Information Distinction between Fixed and Fluctuating Capital Accounts:

Additional Information Distinction between Fixed and Fluctuating Capital Accounts:

-

Question 2

5 / -1

Match the following items in NPO

| | Description | | Options |

| 1 | Legacy donation for specific purpose is shown in Balance Sheet because it is | a | Opening Balance Sheet and Closing Balance Sheet and Income and Expenditure A/c |

| 2 | Entrance Fees is shown in | b | Receipts and Payment A/c |

| 3 | Opening and Closing Cash Balance are shown in | c | Capital Nature Income |

| | | d | Income and Expenditure A/c |

Solution

The correct answer is [1 – c; 2 – d; 3 – b].

The correct match is given below:

| | Description | | Options |

| 1 | Legacy donation for specific purpose is shown in Balance Sheet because it is | c | Capital Nature Income |

| 2 | Entrance Fees is shown in | c | Income and Expenditure A/c |

| 3 | Opening and Closing Cash Balance are shown in | d | Receipts and Payment A/c |

Key PointsNPO(non-profit organisation) - institutions which function without any profit motive. These organizations are welfare of society. Such organization is clubs, schools, trade unions, charitable institutions. For financial statement, following accounts are prepared:

- Receipt and payment A/c

- Income and expenditure A/c

- Balance sheet

Important Points1. Legacy donation for specific purpose is shown in Balance Sheet -

In the financial statements of a non-profit organisation, there are two types of donations.

- General Donations is one of them. This type of donation is not intended for a specific cause. As a result, revenue receipts are considered and recorded in the income and expenditure account.

- Some donations are made with a specific goal in mind. For example, a donation for the construction of a library, a donation for a tournament, and so on. Donations of this nature are classified as capital receipts.

Thus, Legacy donation for specific purpose is shown in Balance Sheet is capital nature.

2. Entrance Fees is shown in - The amount a person pays to become a member of a Not-for-Profit Organisation is known as entrance fees or admission fees. It's a receipt for money. As a result, it is recorded as income and credited to the Income and Expenditure Account.

3. Opening and Closing Cash Balance are shown in- In NPO, Receipts and Payment A/c is the summary of cash and bank transactions. Thus Opening and Closing Cash Balance are shown in Receipts and Payment A/c.

Additional InformationReceipt and Payment Account - is the summary of cash and bank transactions.

Income and expenditure A/c - is similar to Income and Expenditure Account is similar to Profit and Loss Account.

Balance sheet - balance is prepared with the help of Receipt and payment A/c & Income and expenditure A/c.

-

Question 3

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) : Securities premium reserve can not be utilised to pay as dividend to the shareholders.

Reason (R) : Securities premium can be utilised only for the specific purposes stated in companies Act 2013.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

Key Points

Assertion (A) : Securities premium reserve can not be utilised to pay as dividend to the shareholders.

- Assertion is true because Securities premium reserve can not be utilised to pay as dividend to the shareholders.

Reason (R) : Securities premium can be utilised only for the specific purposes stated in companies Act 2013.

- Reason is also true, and it is correct explanation of assertion because it is correct that securities premium reserve cannot be utilised to pay as dividend to the shareholders it can be utilised only for the specific purposes stated in the companies act 2013.

Important Points According to Section 52 of the Act, securities premium can be used for the following purposes:

- For the issue of fully paid bonus share capital.

- For meeting the preliminary expenses incurred by the company.

- For meeting the expenses, commission or discount incurred concerning securities previously issued by the company.

- For ensuring the availability of the premium on the redemption of redeemable debentures or preference share capital of the company.

- For funding a scheme or buy-back of securities which is conducted in compliance with the provisions of Section 68 of the Companies Act.

Additional Information Securities Premium Reserve:

- The additional amount charged on the face value of any share when it is issued, redeemed, or forfeited is known as the Security Premium Reserve.

- According to the Companies Act of 2013, when a security premium must be documented in the balance sheet, it must be done in the Reserve & Surplus section of the Equity & Liabilities section of the balance sheet.

- This item has been added to the Reserve & Surplus category. Furthermore, reserve and excess keep track of all revenues and losses.

-

Question 4

5 / -1

Which key is used to represent the relationship between two relations ?

Solution

The correct answer is option 3.

Concept:

Foreign Key:

A foreign key is used to represent the relationship between two relations.

- A foreign key is an attribute whose value is derived from the primary key of another relation.

- This means that any attribute of a relation (referencing), which is used to refer contents from another (referenced) relation, becomes foreign key if it refers to the primary key of referenced relation.

- The referencing relation is called Foreign Relation.

Hence the correct answer is Foreign Key.

Additional Information

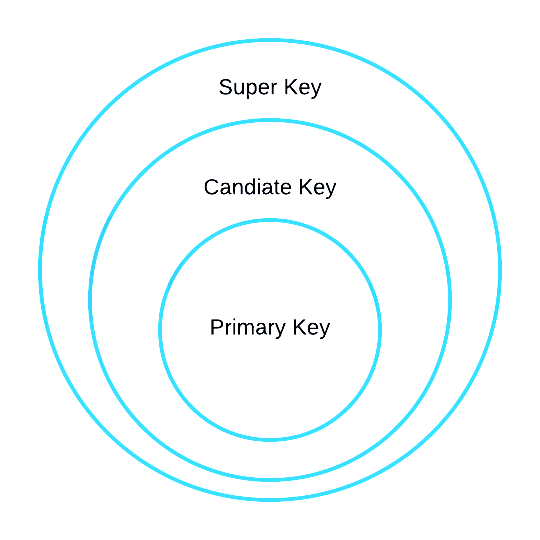

- A superkey is a column combination that identifies an entry in a relational database management system (RDBMS) table. A candidate key is a similar notion in which the superkey is lowered to the bare minimum of columns necessary to uniquely identify each row.

- A candidate key is a specific type of field in a relational database that can identify each unique record independently of any other data.

- A primary key is a column in a database table that uniquely identifies each row/record. Primary keys must have distinct values. NULL values are not allowed in a primary key column.

Relation between super key and candidate key and primary key:

-

Question 5

5 / -1

A,B and C are partners sharing profits in the ratio of 3:2:1. They agree to admit D into the firm. A, B and C agreed to give 1/3rd,1/6,1/9th share of their profit. The share of Profit of D will be:

Solution

The correct answer is 13/54.

Key PointsProfit & Loss ratio - ratio in which profit or loss of partner's share are calculated.Important Points To calculate D's share of Profit when share taken by each Partner is given -

D receives from A's share =1/3 x 3/6 = 3/18 D receives from B's share= 1/6 x 2/6 = 1/18

D receives from C's share=1/6 x 1/9 =1/54

D's share of profit = 3/18+ 1/18+ 1/54

=(9+3+1)/54

=13/54

Additional Information New Profit ratio = Old ratio - Sacrifice Ratio

A = 3/6 -3/18= (9-3)/18=6/18=18/54

B=2//6 - 1/18=(6 -1)/18 =5/18 =15/54

C=1/6 - 1/54 =(9-1)/54=8/54

D =13/54

New Profit ratio = A:B:C:D

=18:15:8:13

-

Question 6

5 / -1

What is the role of the Primary key in MS Access?

Solution

The correct option is All of the above.

Key Points

- A primary key is a field or set of fields with values that are unique throughout a table.

- Values of the key can be used to refer to entire records because each record has a different value for the key.

- Each table can only have one primary key.

- Access can automatically create a primary key when we create a table.

- We can create our own primary key by selecting the fields that we want to use as the primary key.

- Primary key quickly associates data from multiple tables and combine that data in a meaningful way.

- We can include the primary key fields in other tables to refer back to the table that is the source of the primary key.

- There this field is called foreign keys.

- In this example Customer Id in the First table is the Primary key snd in another table it is the Foreign key

Additional Information

- Features of Good Primary Key

- There can only be one primary key for a table.

- The primary key consists of one or more columns.

- The primary key enforces the entity integrity of the table.

- All columns defined must be defined as NOT NULL.

- The primary key uniquely identifies a row.

- Primary keys result in CLUSTERED unique indexes by default.

Important Points

- How to add a Primary Key

- step 1: Open the database that you want to modify.

- Step 2: In the Navigation Pane, right-click the table in which you want to set the primary key and, on the shortcut menu, click Design View.

- Select the field or fields that you want to use as the primary key.

- To select one field, click the row selector for the field you want.

- Step 3: To select more than one field to create a composite key, hold down CTRL, and then click the row selector for each field.

- Step 4: On the Design tab, in the Tools group, click Primary Key.

-

Question 7

5 / -1

Indicate the item which appears under the sub head, short-term provisions:

Solution

The correct answer is Provision for doubtful debts.

Key PointsProvisions - Provisions in accounting relate to the amount set aside from profits in order to cover a potential future expense or asset value drop, even if the exact amount is unclear. Provisions are two types -

- Short term Provisions

- Long Term Provisions

Important PointsShort Term Provision - The amount of provision settled within 12 months from balance sheet date or within operating cycle period from date of its recognition is classified as short term provisions. It is shown under current liabilities on the face of balance sheet. Short term provisions are :

- Provision for doubtful debts

- Provision for Discount on debtors

- Provision for taxes etc.

Thus, Provision for doubtful debts will be shown under the sub head, short-term provisions and under the head of current Liabilities.

Additional Information

Long term Provisions - Other than short term provisions are depicted as long-term provisions under non-current liabilities in balance sheet. Long Term provision are for more than one years periods. Shown under the head of non-current liabilities in balance sheet.

Provision for gratuity - Gratuity is a monetary benefit given by the employer, but not paid as part of the regular monthly salary and provision for gratuity is for long term purpose. These are long-term provisions.

Employee's Provident fund - Employees' Provident Fund (EPF) is a social programme established to ensure that employees have a brighter future. It is a legislative benefit provided to personnel after they retire or leave the military. These are also long term provisions.

Securities Premium Reserve - The additional amount levied on the face value of any share when it is issued, redeemed, or forfeited is known as the Security Premium Reserve. Shown under the head of Reserve & Surplus in balance sheet.

-

Question 8

5 / -1

The company issued 5,000 12% Debentures of Rs 100 each at 10 % Discount and Repayable at 10 % Premium. Interest on Debentures are payable half-yearly on which Tax deducted at source of 10% p.a. what will the amount of tax for a year :

Solution

The correct answer is Rs 6,000.

Key PointsDebentures - Debenture is a written instrument acknowledging a debt under the common seal of the company. It contains a contract for repayment of principal after a specified period or at intervals or at the option of the company and for payment of interest at a fixed rate payable usually either half-yearly or yearly on fixed dates.

Interest on Debentures- Interest on debenture is a charge against the profit of the company and must be paid whether the company has earned any profit or not. According to Income Tax Act, 1961, a company must deduct income tax at a prescribed rate from the interest payable on debentures if it exceeds the prescribed limit. It is called Tax Deducted at Source (TDS) and is to be deposited with the tax authorities. Of course, the debenture holders can adjust this amount against the tax due from them.

Important Points Interest on Debentures is always calculated on nominal value/book value of Debentures.

Debentures issued = 5000

Debenture par value = 100

Debenture book value = 5000 x 100 = Rs.5,00,000

Interest rates on Debentures = 10% p.a

Interest amount on debentures yearly = Rs.500000 x 12/100 = 60,000

Rate of TDS = 10%

TDS Amount = Amount of interest x TDS rate

=Rs.60000 x 10/100

=Rs.6000 a year

Additional InformationJournal Entries for interest of debentures & TDS

| Date | Particulars | Dr. | Cr. |

| 30 Sept | Debenture Interest A/c Dr. | 30,000 | |

| To Debentureholders A/c | | 27,000 |

| To Income Tax Payable A/c | | 3,000 |

| (Interest due for 6 months and tax deducted at source) | | |

| 30 Sept | Income Tax payable A/c Dr. | 3000 | |

| To Bank A/c | | 3000 |

| (Tax deducted at source paid to the government) | | |

| 31 March | Debenture Interest A/c Dr. | 30,000 | |

| To Debentureholders A/c | | 27,000 |

| To Income Tax Payable A/c | | 3,000 |

| (Interest due for 6 months and tax deducted at source) | | |

| 31 March | Income Tax payable A/c Dr. | 3000 | |

| To Bank A/c | | 3000 |

| (Tax deducted at source paid to the government) | |

-

Question 9

5 / -1

X and Y are partners sharing profits in the ratio 5 : 3. They admitted Z for 1/5th share in profits, for which he paid Rs. 1,20,000 as Capital and Rs. 60,000 as Goodwill. Capitals for each partner, taking Z's capital as base capital will be:

Solution

The correct answer is 3,00,000, 1,80,000 and 1,20,000.

Key PointsGoodwill- the established reputation of a business regarded as a quantifiable asset and calculated as part of its value. The fictitious assets of the firm.

Partner's Capital Account - which all the transactions between the partners and the firm are recorded. Normally, the partner's capital account have credit balance.

Important Points Sometime partners decide to adjust firm capital on the basis of new partner's capital. Such capital shall be calculated as follows :

Z's capital = Rs.1,20,000

Z's share in profit =1/5 th

Firm's capital as per new partner's capital = inverse of Z's share of profit x Z's capital

=5/1 x 1,20,000

=Rs.6,00,000

Thus, Firm's capital should be Rs.6,00,000 as basis of new partners capital. New Firm's capital of each partner will be according to new profit share ratio.

Calculation of New profit sharing ratio :

Z's share = 1/5

Remaining share = 1 - 1/5 = 4/5

X's share = 4/5 x 5/8 = 1/2 = 5/10

Y's share = 4/5 x 3/8 = 3/10

Z's share = 1/5 = 2/10

New Profit sharing ratio X:Y:Z is 5:3:2.

Thus,

X's new capital = 6,00,000 x 5/10 = Rs.3,00,000

Y's new capital = 6,00,000 x 3/10 = Rs.1,80,000

Z's Capital = 1,20,000.

-

Question 10

5 / -1

Golden Firework Ltd. is authorised to issue share 5,00,000 of Rs. 100 each. Company raised the capital by issue of 2,00,000 shares through e-IPO. As per the decision of Managing Board of Directors of the company, company issued 75,000 shares to their parent company and 40,000 shares to existing employees of the company as per their choice and option at a price below than the market price.

"Company issued 75,000 shares to their parent company" is an example of _____

Solution

The correct answer is Private Placement.

Key Points"Company issued 75,000 shares to their parent company" is an example of a Private Placement of Shares because the company is issuing 75,000 shares to their parent company without offering them to the public or employees, and according to section 42 of the Companies Act 2013, "Any Offering of a company's securities for a select group of persons other than by way of a public issue through a private placement offer letter is categorised under Private placement by companies."

Important Points Section 42 of Companies Act 2013:

- A firm can make a private placement to a small group of people under Section 42 of the Companies Act, 2013 ('Act').

- A private placement offer letter is a letter in which a company offers its shares or invites a select group of people to subscribe to its securities in lieu of a public offering.

- Securities can only be sold to selected or specified individuals in a private placement (as identified by the board of the company).

- A firm that makes a private placement cannot advertise its securities publicly or use marketing, media, or distribution agents or channels to notify the public about the offer.

- The offer will be regarded a public offer if it is published or marketed not private placement.

Additional Information Employee stock option plan (ESOP):

- The Employee Stock Option Plan, or ESOP, is a type of stock option plan in which a corporation issues shares to its employees at a lower price than the market price.

- With the goal of inspiring employees to perform better and promoting a sense of ownership, employees are given the option to execute the offer.

-

Question 11

5 / -1

MS Access supports which of the following database?

1. Flat File Database

2. Relational Database

Solution

The correct answer is option 4.

Concept:

Microsoft Access:

Microsoft Access is a relational database management application that allows you to save information for reference, reporting, and analysis. Access can also help you get beyond the constraints that come with using Excel or other spreadsheet programs to manage huge volumes of data.

- MS Access supports both flat-file databases and relational databases.

- The database management system (DBMS) Microsoft Access is used to store and manage data. Access is a commercial and enterprise application that is part of the Microsoft 365 package.

- A flat-file database is used to store data in a single table structure. A relational database is used to store data in a multiple-table structure. A flat-file database can be accessed by a variety of software applications like MS access.

Hence the correct answer is Both 1 and 2.

-

Question 12

5 / -1

The area of interest for a creditor while analysing financial statement will be:

Solution

The answer is Solvency.

Key PointsFinancial statements - Financial statements are written documents that describe a company's operations and financial performance.

Important PointsSolvency Ratio- Solvency of business is determined by its ability to meet its contractual obligations towards stakeholders, particularly towards external stakeholders, and the ratios calculated to measure solvency position are known as ‘Solvency Ratios’. These are essentially long-term in nature.

Before approving any loan, the creditor performs an investigation to determine the borrower's credit risk and repayment potential and solvency ratio shows business credit risk and capacity to payback. Thus, the area of interest for a creditor while analysing financial statement is solvency.

Additional InformationLiquidity Ratio- The ability of the business to pay the amount due to stakeholders as and when it is due is known as liquidity, and the ratios calculated to measure it are known as ‘Liquidity Ratios’. These are essentially short-term in nature.

Profitability Ratio- It refers to the analysis of profits in relation to revenue from operations or funds (or assets) employed in the business and the ratios calculated to meet this objective are known as ‘Profitability Ratios’

Proprietary Ratio- The proprietary ratio compares how much money investors have put into a company's capital to how much money the company needs to run its operations.

-

Question 13

5 / -1

Company's liquid assets are Rs. 5,00,000 and its current liabilities are Rs. 3,00,000. Thereafter, it paid Rs. 1,00,000 to its trade payable. Quick ratio will be:

Solution

The correct answer is 2:1.

Key PointsQuick ratio-The quick assets are defined as those assets which are quickly convertible into cash. It is calculated to serve as a supplementary check on liquidity position of the business and is therefore, also known as ‘Acid-Test Ratio’. Quick assets excludes prepaid expenses, advance tax, inventories etc. from the current assets.

Important PointsLiquid assets= Rs. 5,00,000 - Rs. 1,00,000(payment to creditors in cash)

=Rs.4,00,000

Current liabilities = Rs. 3,00,000 - Rs. 1,00,000(excludes for payment to creditors)

= Rs.2,00,000

Quick ratio = Quick assets(Liquid assets): Current liabilities

= 4,00000 : 2,00,000

=2:1

Additional Information

- Current Ratio =Current assets : Current liabilities

- Current Ratio & Quick ratio are part of Liquidity Ratios

-

Question 14

5 / -1

Amount paid for stationary purchased Rs 45,000. The creditor for stationary in the beginning and end of the year Rs 4,000 and Rs 6,500. Cash purchase of stationary is Rs 15,000. Calculate the amount of stationary purchased in the current year :

Solution

The correct answer is Rs 62,500

Key PointsCalculation of the amount of stationary purchased in the current year:

| Particulars | Amount |

| Amount paid for stationary purchased | 45000 |

| Add: Cash purchase of stationary | 15000 |

| Add: Difference b/w opening & closing bal. of Creditors for stationary* | 2500 |

| Amount of stationary purchased in the current year | 62500 |

Note: *Closing balance of creditors for stationary is more than opening balance which signifies credit purchase of Stationary.

Important Points Stationary Account

Dr Cr.

| Particulars | Amount | Particulars | Amount |

| To cash | 45000 | | |

| To cash | 15000 | | |

| To creditors for stationary a/c | 2500 | By Profit and Loss A/c | 62,500 |

| Total | 62500 | Total | 62500 |

Creditors for Stationary Account

Dr Cr.

| Particulars | Amount | Particulars | Amount |

| | | By Balance b/d | 4000 |

| | | By purchase of stationary (Bal. Fig) | 2500 |

| To balance c/d | 6500 | | |

| Total | 6500 | Total | 6500 |

-

Question 15

5 / -1

What will be the output of the following MS-Excel formula?

=SUM(3, 2^1^3)

Solution

The correct answer is 11

Key Points SUM function of MS-Excel:

- The sum function of MS-Excel is one of the basic functions performed.

- In the above example, the sum of 3 and 2^1^3 will be equal to 11.

- It is because the numbers are 1 and 3 to the power of 2 and 1 which is ultimately equal to 8.

- The sum function can be used for both continuous and non-continuous data.

Hence, the correct sum of (3, 2^1^3) will be 11.

Alternate Method

Alternate Method

=SUM(3, 2^1^3)

Step 1, 2^1 = 2

2^3 = 8

Then, 2^1^3 = 8

=SUM(3, 2^1^3) means, =SUM(3, 8)

That equals to 3+8 = 11

-

Question 16

5 / -1

On 1st January 2018 company issued shares of Rs.10,00,000 and paid Rs. 10,000 as Share Issue Expense. Amount shown in Financing Activities in cash flow statement

Solution

The correct answer is Rs. 10,00,000 as Inflow and Rs. 10,000 as Outflow.

Key Points Cash Flow Statement:

- A cash flow statement depicts the inflow and outflow of cash and cash equivalents from a company's various activities over a given time period.

- The main goal of a cash flow statement is to provide meaningful information about an enterprise's cash flows (inflows and outflows) over time

- It describes the reasons for cash transactions and payments, as well as changes in cash balances, during the course of an accounting year.

- Cash Flow Statement describes cash inflow and outflow under three main headings:

- Operating Activities

- Financing Activities

- Investing Activities

Important Points Company issued shares of Rs.10,00,000:

- This will result in cash inflow for the company. Since, issue of shares is done for finance purpose, it will be recorded as Cash inflow from Financing Activities.

Paid Rs. 10,000 as Share Issue Expense:

- This will result in cash outflow for the company. Since, these expenses are incurred in relation with issue of shares, it will be recorded as Cash outflow from Financing Activities.

-

Question 17

5 / -1

Which of the following not the limitation of financial statement analysis?

Solution

The incorrect answer is Inter firm comparison.

Key PointsThe incorrect answer is Inter firm comparison because it is not the limitation of financial statement analysis, even it is one of the advantage of financial analysis. And all other options are limitations of financial statement analysis.

Important PointsFinancial Statement Analysis : It is a systematic numerical depiction of the link between one financial fact and another that is used to assess a company's profitability, operational efficiency, solvency, and development potential.

Limitations of Financial Statement Analysis :

- Financial analysis does not consider price level changes.

- Financial analysis may be misleading without the knowledge of the changes in accounting procedure followed by a firm.

- Financial analysis is just a study of reports of the company.

- Monetary information alone is considered in financial analysis while non-monetary aspects are ignored.

- The financial statements are prepared on the basis of accounting concept, as such, it does not reflect the current position.

- The results of financial statement analysis may be deceiving due to window dressing.

- The analyst's personal ability and prejudice have an impact on financial accounts.

Advantages of Financial Statement Analysis:

- It makes the data simpler and more understandable.

- It indicates the trend.

- It indicates the strong points and weak points of the concern.

- It helps to compare the firm's performance with the average performance of the industry or other firm.

- It helps in forecasting.

-

Question 18

5 / -1

At the time of dissolution of a partnership Firm, 50% of the Furniture valued at Rs. 20,000, taken by a Partner at Rs. 18,000, and remaining 50% has been sold at 20% less than the book value, amount transferred to Bank Account will be:-

Solution

The correct answer is Rs. 16000

Key Points 50% of the Furniture valued at Rs. 20,000

Therefore, total value of furniture = 20000 x 100/50 = 40,000

50% of the Furniture valued at Rs. 20,000, taken by a Partner at Rs. 18,000

Book value of the remaining 50% of Furniture = 40000 x 50% = 20,000

Remaining 50% furniture is sold at 20% less

Therefore,

Sale value of 50% = (100-20)% of 40000 = 80% of 20000 = 16,000

Amount transferred to Bank Account will be Rs. 16000

Important Points Journal Entry

| Particulars | Amount Dr. | Amount Cr. |

| Realisation A/c Dr. | 40000 | |

| To Furniture A/c | | 40000 |

| (being furniture transferred to Realisation A/c) | | |

| | | |

| Bank A/c Dr. | 16000 | |

| Partner's Capital Account Dr. | 18000 | |

| To Realisation | | 34000 |

| (50% furniture taken over by Partner and remaining sold) | | |

-

Question 19

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) : Profitability ratios are calculated to analyse the earning capacity of the business which is the outcome of utilisation of resources employed in the business.

Reason (R) : Ratio analysis is helpful to take investment decision.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is Both Assertion (A) and Reason (R) are true, and Reason (R) is not the correct explanation of Assertion (A).

Key PointsAccounting ratio - When the number is calculated by referring to two accounting numbers derived from the financial statements, it is termed as accounting ratio.

Ratio analysis- Ratio analysis is a critical component in interpreting financial statement outcomes. Ratio analysis is a technique for regrouping data using arithmetical correlations.

Profitability Ratios: It refers to the analysis of profits in relation to revenue from operations or funds (or assets) employed in the business and the ratios calculated to meet this objective are known as ‘Profitability Ratios’.

Important PointsAs above per question -

Assertion (A) : Profitability ratios are calculated to analyse the earning capacity of the business which is the outcome of utilisation of resources employed in the business.

Assertion is true because Profitability ratios shows a close relationship between the profit and the efficiency with which the resources employed in the business are utilised. The profitability is mainly summarised in the statement of profit and loss and shows financial performance of company.

Reason (R) : Ratio analysis is helpful to take investment decision.

Reason is true because the ratio analysis helps to understand whether the business firm has taken the right kind of operating, investing and financing decisions. It indicates how far they have helped in improving the performance.

Profitability ratios shows the financial performance of business and resources utilised which helps to make investment decision. Ratio analysis helps in operating, investing and financing decisions.

Thus, Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

This is because Assertion talks specifically about profitability ratio but reason explains the advantage of ratio analysis.

Additional Information Advantages of Ratio Analysis are as following-

- Helps to understand efficacy of decisions

- Simplify complex figures and establish relationships

- Helpful in comparative analysis

- Identification of problem areas

- Enables SWOT analysis and more

-

Question 20

5 / -1

A company issued 4,000 equity shares of Rs. 10 each at par payable as under:

On application Rs. 3, on allotment Rs. 2; on first call Rs. 4 and on final call Rs. 1 per share. Applications were received for 16,000 shares were rejected and pro-rata allotment was made to the applicant for 10,000 shares. How much amount will be received in cash on first call, when excess application money is adjusted towards amount due on allotments and calls:

Solution

The correct answer is Rs. 6,000.

Key Points Over subscription:

- Oversubscription of shares occurs when a firm receives more applications to buy its stock than the quantity of shares it has issued.

- In this case, the company issues shares on pro rata basis.

- Pro-rata allotment refers to the allotment of shares in proportion of the shares applied for.

- When a company makes pro-rata allotment, it adjusts the excess money received at the time of application firstly, towards the allotment and then towards calls.

Important Points

| Particulars | | Amount |

| Application money received | 10000 x 3 | 30000 |

| Less: Application money for 4000 shares | 4000 x 3 | (12000) |

| Excess money received | | 18000 |

| Less: Adjustment for Allotment money | 4000 x 2 | (8000) |

| Adjustment for first call money | | 10000 |

| First Call money due | 4000 x 4 | 16000 |

| Amount to be received on first call | | 6000 |

Hence, amount to be received on first call in cash = Rs. 6000

-

Question 21

5 / -1

Marketable Securities costing Rs. 10,000 sold for Rs. 12,000, Profit on sale of Marketable Securities was credited to Statement of Profit and Loss. Which of the following statement is correct?

Solution

The correct answer is Rs. 2,000 will be deducted from Net Profit under Operating Activity and shown as Extra-ordinary Item under Operating Activities.

Key PointsMarketable securities - are the liquid assets that are readily convertible into cash. Examples: treasury bills, commercial papers, treasury bills, bills receivables and other short term investments.

Cash flows from operating activities-Operating activities are the activities that constitute the primary or main activities of an enterprise. Cash flows from operating activities are primarily derived from the main activities of the enterprise. They generally result from the transactions and other events that enter into the determination of net profit or loss.

Important PointsExtra-ordinary Item - Extraordinary items are non-recurring in nature and hence cash flows associated with extraordinary items should be classified and disclosed separately as arising from operating, investing or financing activities.

Profit/loss on sale of assets are non cash and non operating items. Adjustment of non cash and non operating items are deducted/added from Net profit before taxation and extra ordinary items in cash from operating activities. Then later these adjustments are added/subtracted in Extra-ordinary items under operating activities.

Adjustment of Profit on sale of marketable Securities of Rs.2000 will be as follows :

- Marketable Securities are currents assets for the business.

- Cash flow regarding, these will be recorded in cash flow from operating activities.

- Profit on sale of assets are non cash and non operating items.

- In Cash flow from operating activities by indirect method , profit of Rs.2000 will be deducted from Net profit before taxation and extra ordinary items.

- Then later, profit of Rs.2000 will be added in Extra-ordinary items heading.

Thus, treatment of Profit on sale of Marketable Securities was credited to Statement of Profit and Loss wiil be Rs. 2,000 will be deducted from Net Profit under Operating Activity and shown as Extra-ordinary Item under Operating Activities.

Additional InformationCash Inflows from operating activities-

- cash receipts from sale of goods and the rendering of services.

- cash receipts from royalties, fees, commissions and other revenues.

Cash Outflows from operating activities-

- Cash payments to suppliers for goods and services.

- Cash payments to and on behalf of the employees.

- Cash payments to an insurance enterprise for premiums and claims, annuities, and other policy benefits.

- Cash payments of income taxes unless they can be specifically identified with financing and investing activities.

-

Question 22

5 / -1

X and Y are partners in a firm with capital of Rs. 1,80,000 and Rs. 2,00,000. Z was admitted for 1/3rd share in profits and brings Rs. 3,40,000 as capital. Calculate the amount of hidden goodwill for Z.

Solution

The correct answer is Rs.1,00,000.

Key PointsGoodwill -the established reputation of a business regarded as a quantifiable asset and calculated as part of its value. The fictitious assets of the firm. Sometimes the value of goodwill is not given at the time of admission of a new partner. In such a situation it has to be inferred from the arrangement of the capital and profit sharing ratio.

Important Points Calculation of hidden goodwill-

Z capital = Rs. 3,40,000

z's share =1/3

Total capital of Firm = Rs.3,40,000 x 3/1

= Rs.10,20,000

Total of X,Y & Z capital = Rs.1,80,000 + 2,00,000+ 3,40,000

= Rs.7,20,000

Goodwill of the firm = RS.10,20,000 - Rs.7,20,000

=3,00,000

Z's share of Goodwill = Rs.3,00,000 x 1/3

=Rs.1,00,000

Thus, hidden goodwill Rs.1,00,000 which Z bring with amount of capital.

Additional Information Entries on when Z does not bring his share of goodwill -

| Particulars |

Dr. |

Cr. |

| Bank A/c Dr. |

3,40,000 |

|

| To Z's capital A/c |

|

3,40,000 |

| (amount of brought by Z as capital) |

|

|

| Z's capital A/c Dr. |

1,00,000 |

|

| To X's capital A/c |

|

50000 |

| To Y's capital A/c |

|

50000 |

| (amount transferred to old partners account in sacrificing ratio) |

|

|

-

Question 23

5 / -1

Fixed assets of a company increased from Rs. 3,00,000 to Rs. 4,00,000. The percentage change is:

Solution

The correct answer is 33.33%.

Key PointsFixed Assets -

- A long-term tangible piece of property or equipment that a company owns and utilises in its operations to produce revenue is referred to as a fixed asset.

- Property, plant, and equipment are the most popular terms for fixed assets.

- Fixed assets are objects that a business intends to employ in the long run to create revenue.

- Fixed assets are depreciated to account for the decrease in value as the assets are utilised.

Appreciation of assets - Appreciation is the term used to describe the increase in the value of a fixed asset. In general, appreciation is the increase in the value of an item through time.

Important PointsCalculation of % change in fixed assets :

change in value of fixed assets = 4,00,000 - 3,00,000

Percentage change = change in value of fixed assets/ Book value of Fixed assets x100

Percentage change =(Rs.1,00,000/ Rs.3,00,000) x 100

Percentage change = 33.33 %

-

Question 24

5 / -1

A cell with a highlighted cell boundary is called as a/an __________ in Microsoft Excel.

Solution

The correct answer is Active cell.

Key Points

- The active cell is the current selected cell which has a bold boundary for easy identification.

- By default initially opened a MS-Excel, the first cell is the active cell.

- It can be identified by a bold (typically blue) outline that surrounds the cell.

Important Points

- The cell that is not currently selected is called passive cell or passive state of a cell.

- A mixed cell in MS-Excel is either an absolute column and relative row or absolute row and relative column.

- A cell reference or relative cell reference describes how far away a cell or group of cells is from another cell in the same spreadsheet.

-

Question 25

5 / -1

A and B are in partnership sharing profits in the ratio of 3:2. They take C as new partner. Goodwill of the firm is valued at Rs. 3,00,000 and C brings Rs. 30,000 as his share of goodwill, in cash which is entirely credited to the Capital Account of A. New profit sharing ratio will be.

Solution

The correct answer is 5:4:1.

Key PointsProfit Sharing Ratio - ratio in which profit or loss of partner's share are calculated.

Sacrifice ratio - proportion do existing partners give up their profit share in favor of newly admitted partners. The share that is thus surrendered is frequently given to new partners by one or two or all of the current partners.

Important PointsIn the above question, based on the information provided, C brings Rs. 30,000 as his share of goodwill, in cash which is entirely credited to the Capital Account of A, We can conclude that A makes a entirely sacrifice and distributes a portion of his profit to C.

Calculation of 's share of profit -

C 's Capital = Rs.3,00,000

C's share of Goodwill = Rs.30,000

C's share of profit = C's share of Goodwill/C 's Capital

=Rs.30,000/Rs.3,00,000

=1/10

A's share of sacrifice =1/10

New Profit sharing Ratio = Old Ratio - Sacrifice Ratio

A's share = 3/5 - 1/10 = (6-1)/10 = 5/10

B's share = 2/5 - 0 = 2/5 = 4/10

C's share = 1/10

Thus, New Profit sharing ratio if A:B:C is 5:4:1.

Additional InformationSacrifice Ratio = Old Ratio - New ratio

Gaining ratio = New ratio - Old Ratio

-

Question 26

5 / -1

A company forfeited 3,000 shares of Rs. 10 each (which were issued at par) held by Kishore for non-payment of allotment money of Rs. 5 per share. The called up value per share was Rs. 8. On forfeiture, the amount debited to share capital:

Solution

The correct answer is Rs. 24,000.

Key Points Share Forfeiture:

- The circumstance in which the allotted shares are cancelled by the issuing firm due to non-payment of the subscription amount as requested by the issuing company from the shareholder is referred to as forfeiture of shares.

- If a shareholder's shares are forfeited, the shareholder's rights and interests as a shareholder are lost, and the shareholder ceases to be a member of the organisation.

- Some shareholders may be unable to pay instalments, such as money allocation or call money. In such a case, consider the following:

- Their part will be forfeited, i.e., the shareholder's share would be cancelled.

- Apart from the premium entries already specified in the accounting records, all the entries related with the forfeited stocks must have conversed.

- The amount is deducted from the share capital account.

Journal entry for Share Forfeiture :

Share Capital A/c Dr. (No. of shares forfeited x Called up value per share)

To Calls in Arrears A/c (Amount not received on Allotment and Calls)

To Share Forfeiture A/c (Amount received on application, allotment and Calls so far)

(forfeiture of shares issued at par)

Important Points

| Particulars | Dr. | Cr |

| Share Capital A/c Dr. | 24,000 | |

| To Calls in Arrears A/c | | 15,000 |

| To Share Forfeiture | | 9,000 |

| (3,000 shares forfeited) | | |

Working note:

Share Capital = No. of shares forfeited x Called up value per share = 3,000 x 8 = 24,000

Calls in Arrears = Amount not received on allotments = 3,000 x 5 = 15,000

Share Forfeiture = Amount received on application = (24,000-15,000) = 9,000

hence, share capital account will be debited by 24,000.

-

Question 27

5 / -1

At the time of issue of debentures , debentures account is :

Solution

The correct answer is Credited by nominal value of the debenture.

Key PointsDebentures - Debenture is a written instrument acknowledging a debt under the common seal of the company. It contains a contract for repayment of principal after a specified period or at intervals or at the option of the company and for payment of interest at a fixed rate payable usually either half-yearly or yearly on fixed dates.

Important PointsIssue Price - the price at which shares/bonds are purchased, or the price at which a company's shares are issued in the market.

Nominal Value - The nominal value or book value, of a share, is usually assigned when the stock is issued. Also called the face value or par value.

In debentures, Debentures Account credited in issued at nominal value/Book value/ par value of debentures. Debenture Application/allotment/calls are recorded at issue price of debentures. Cash/Bank account is recorded at amount received.

Thus, at the time of issue of debentures, the debentures account is credited by the nominal value of the debenture.

Additional InformationEntries on issue of Debentures:

| At Par |

| Particulars | Dr. | Cr. |

| Bank A/c Dr. | xxx | |

| To debenture Application & allotment A/c | | xxx |

| (amount of application received ) | | |

| | | |

| Debenture Application & allotment A/c Dr. | xxx | |

| To Debenture A/c | | xxx |

| (amount of application transferred) | | |

| At Discount |

| Debenture Application & allotment A/c Dr. | xxx | |

| Discount on issue of shares A/c Dr. | xxx | |

| To Debenture A/c | | xxx |

| (amount of money due on debentures) | | |

| At Premium |

| Debenture Application & allotment A/c Dr. | xxx | |

| To Debenture A/c | xxx | |

| To Securities Premium Reserve A/c | | xxx |

| (money due on debentures including the premium) | | |

-

Question 28

5 / -1

In MS-Excel software a formula is entered into a cell using______symbol.

Solution

The correct answer is =.

Key Points

- A formula always starts with an equal sign (=),which can be followed by numbers, math operators (such as a plus or minus sign), and functions,which can really expand the power of a formula.

Additional Information

@ | Ampersat, arobase, asperand, at, or at symbol. |

# | Octothorpe, number, pound, sharp, or hash. |

& | Ampersand, epershand, or and symbol. |

-

Question 29

5 / -1

A and B are partners, sharing profits in the ratio of 5 : 3. They admit C for 1/5th share in profits, which he acquires equally from both A and B. New profit sharing ratio will be:

Solution

The correct answer is 21 : 11 : 8.

Key PointsProfit sharing ratio - ratio in which profit or loss of partner's share are calculated.

Important PointsCalculation of share acquired by C from (sacrifice ratio)-

A = 1/5 x 1/2 = 1/10

B = 1/5 x 1/2 = 1/10

Calculation of new profit sharing ratio -

New Ratio = Old Ratio - Sacrifice ratio

A's share = 5/8 - 1/10 = (25-4)/40 = 21/40

B's share = 3/8 - 1/10 = (15-4)/40 = 11/40

C's share = 1/5 = 8/40

Thus, the New Profit sharing ratio A:B:C:D is 21:11:8.

-

Question 30

5 / -1

Rajan Limited issued 50,000 shares at a price lower than the nominal value of the share. The shares issued are called:

Solution

The correct answer is Sweat equity shares.

Key PointsShares - Shares, often known as stocks or shares of stock, indicate a corporation's equity ownership divided into units, allowing multiple persons to control a percentage of the company. Shares can be issue by company in two ways -

- Shares issue at par

- Shares issue at premium

According to Section 53 of Companies Act 2013, a company shall not issue shares at a discount.

Important PointsSweat equity shares -Sweat Equity Shares are an equity-linked instrument issued by a corporation to its employees or directors in exchange for their knowledge and skills, intellectual property rights, or value creation to the company. These shares are sold at a discount or for a non-cash payment.

According to section 54 of Companies Act 2013, only Sweat equity shares can be issued at discount by company.

In the above case, shares at a price lower than the nominal value of the share means shares at discount are issued. Thus, shares issued at discount can only sweat equity shares.

Additional InformationRedeemable Preference shares - Redeemable Preferences shares are preference shares that have a callable option incorporated in them, meaning they can be redeemed by the company at any time.

Equity shares - An equity share, also known as an ordinary share, is a fractional ownership that commences the maximum entrepreneurial obligation associated with a trading firm. In every corporation, these categories of shareholders have the ability to vote.

Bonus Shares - A bonus share is a share that a corporation offers to its shareholders in addition to their regular stock. These shares are available for no cost. It's a win-win situation for both parties, as investors get free stock and corporations gain existing shareholders' confidence in their operations.

-

Question 31

5 / -1

‘A’ one of the Partners was to bear all the Realisation Expenses for which he was given a commission of 3% of net cash realised from Dissolution. Cash realised from Assets was Rs. 25,000. Amount paid for paying off liabilities amounted to Rs. 5,000. The amount of commission will be:-

Solution

The correct answer is Rs. 600

Key Points Realisation expenses - The expenses which are incurred for realisation of assets and discharge of liabilities is called realisation expense.

Important Points Cash realised from Assets was Rs. 25,000 (Given)

Amount paid for paying off liabilities amounted to Rs. 5,000 (Given)

Net Cash Realised = Cash realised from Assets - Amount paid for paying off liabilities

Net Cash Realised = 25000 - 5000 = 20,000

Commission paid to A = 3% of net cash realised from Dissolution

Commission paid to A = 20,000 x 3% = 600

The amount of commission paid to A = 600

-

Question 32

5 / -1

Z limited issued shares of Rs. 100 each at a premium of 10%. Mr. Q purchased 500 shares and paid Rs. 20 on application but did not pay the allotment money of Rs. 30. If the company forfeited his 30% shares, the forfeiture account will be credited by:

Solution

The correct answer is Rs. 3,000.

Key PointsShare Forfeiture:

- The circumstance in which the allotted shares are cancelled by the issuing firm due to non-payment of the subscription amount as requested by the issuing company from the shareholder is referred to as forfeiture of shares.

- If a shareholder's shares are forfeited, the shareholder's rights and interests as a shareholder are lost, and the shareholder ceases to be a member of the organisation.

- Some shareholders may be unable to pay instalments, such as money allocation or call money. In such a case, consider the following:

- Their part will be forfeited, i.e., the shareholder's share would be cancelled.

- Apart from the premium entries already specified in the accounting records, all the entries related with the forfeited stocks must have conversed.

- The amount is deducted from the share capital account.

Journal entry for Share Forfeiture :

Share Capital A/c Dr. (No. of shares forfeited x Called up value per share)

To Calls in Arrears A/c (Amount not received on Allotment and Calls)

To Share Forfeiture A/c (Amount received on application, allotment and Calls so far)

(forfeiture of shares issued at par)

Important Points Company forfeited 30% shares, it means 30% of 500 = 30/100*500 = 150 shares forfeited

hence, the required entry will be

| Particulars | Dr. | Cr. |

| Share Capital A/c Dr. | 7,500 | |

| To Calls in Arrears A/c | | 4,000 |

| To Share Forfeiture A/c | | 3,000 |

| (500 shares forfeited for non-payment of allotment) | | |

Working Note :

Share Capital = 150 x 50 = 7500

Calls in arrears = 150 x 30 = 4500

Share Forfeiture = Share Capital - Calls in Arrears = 7,500 - 4,000 = 3,000

Hence, share forfeiture credited by amount of Rs. 3,000.

-

Question 33

5 / -1

If net revenue from operations of a firm is Rs. 15,00,000, Gross profit is Rs. 9,00,000 and operating expenses are Rs. 75,000. What will be the percentage of operating income on net revenue from operations?

Solution

The correct answer is 55%.

Key PointsOperating income - Operating income is computed by subtracting the cost of goods sold and operating expenses from a company's revenue. Operating income is also called income from operating profit.

Important PointsNet revenue from operations of a firm(Net Sales) = Rs.15,00,000

Gross profit = Rs.9,00,000

operating expenses = Rs.75,000

Operating profit = Gross Profit - Operating Expenses

=Rs.9,00,000 - Rs.75,000

=Rs.8,25,000

operating profit ratio (operating income on net revenue from operations)=

= (Operating profit / Net Sales) x100

= Rs.8,25,000/Rs.15,00,000 x 100

= 55%

Additional InformationFormula's for calculating operating Income -

Operating Income = Gross Profit - Operating Expenses

Operating Income = Revenue - Cost of Goods sold - Operating Expenses

Operating Income = Net Income + Interest + Taxes + Other Income/Losses

-

Question 34

5 / -1

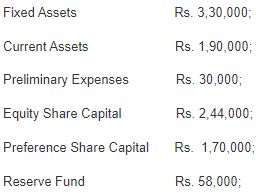

On the basis of the following information received from a firm, its Proprietory Ratio will be:

Solution

The correct answer is 85%.

Key PointsProprietary Ratio :

- The proprietary ratio is a form of solvency ratio that can be used to calculate the quantity or contribution of owners or proprietors to the total assets of a company.

- This ratio also known as the shareholder equity ratio or the net worth ratio, is a measure of a company's financial strength.

- The main goal of this ratio is to figure out what percentage of a company's total assets is supported by the owners.

- The proprietary ratio can be used to assess the stability of a business's or company's capital structure, as well as to demonstrate how a company's assets are produced by issuing a number of equity shares rather than taking loans or debt from outside sources.

Formula: Proprietary Ratio = (Shareholder's Fund / Total Assets) x 100

where,

Proprietor's Fund is also known as Shareholder's Fund and total assets is the summation of current assets and non-current assets.

Total Assets = Non current Assets + Current Assets

Important Points Proprietary Ratio = (Shareholder's Fund / Total Assets) x 100

Hence, Shareholder's Fund = Equity Share Capital + Preference Share Capital + Reserves fund - Preliminary Expenses

Shareholder's fund = 2,44,000 + 1,70,000 + 58,000 - 30,000 = 4,42,000

Total Assets = Fixed Assets + Current Assets = 3,30,000 + 1,90,000 = 5,20,000

Hence, proprietary ratio = 4,42,000 /5,20,000 x 100 = 85%

-

Question 35

5 / -1

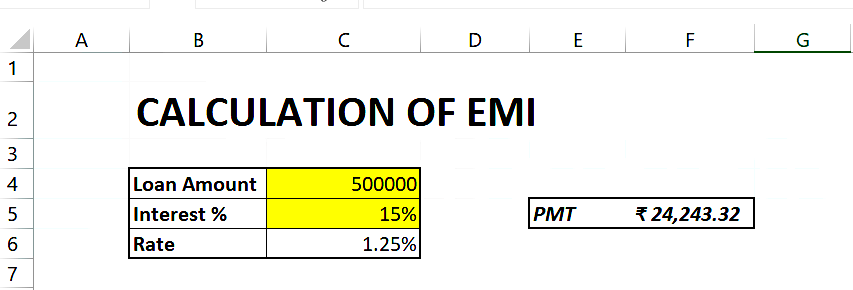

Which cell address will be used for rate, nper, and pv respectively, for the following PMT formula, as per the given data?

Solution

The correct answer is option 2.

The PMT is used to calculate the payment of each month as EMI, for the owned loan. The PMT stands for payment.

The PMT formula is represented as: PMT(rate, nper, pv, [fv], [type])

Where the rate, nper, pv, [fv], [type] are arguments.

The arguments which are in square brackets are optional arguments.

The arguments which are not in square brackets are mandatory arguments.

The arguments are described as:

- rate:- it represents the monthly rate of interest for the loan.

- nper:- it represents the number of payments of months in which the loan will be paid completely with interest.

- pv:- it represents the principal amount that is taken as a loan.

- fv:- it represents the future value or a cash balance a user wants to achieve after the last payment is made.

- type:- it represents the number 0 (zero) or 1 and indicates when payments are due. The 0 represents the due amount at the end of the period, and the 1 represents the due amount at the beginning of the period.

The given excel data as per the formula requirement is described as:

- The principal is 500000, and its cell address is C4. So, the C4 will be taken as argument pv.

- The rate is 1.25% and its cell address is C6. So the C6 will be taken as n argument rate.

- The 24 is the number of payments, hence the argument nper is 24.

-

Question 36

5 / -1

Amount of discount given at the time of reissue of shares should be debited to :

Solution

The correct answer is Share Forfeiture A/c.

Key PointsThe correct answer is Share Forfeiture Account because at the time of reissue of shares, amount of discount is debited to Share Forfeiture Account.

Journal entry for reissue of shares at discount are as follows :

Bank A/c Dr. (the amount received on reissue)

Share Forfeiture A/c Dr. (the amount allowed as discount)

To Share Capital A/c (paid up amount)

Important PointsRe-Issue of Shares: Directors have the authority to reissue the forfeited shares on such terms as they think fit. That is to say that they are at liberty to reissue the forfeited shares at par, at premium or at discount. However, if the shares are re-issued at a discount the amount of the discount cannot exceed the amount previously received on these shares.

For example, if a share of 10, on which 3 has already been received, is forfeited and reissued, minimum 7 must be collected on its reissue. It means that maximum of 3 can be allowed as discount on the reissue of such shares.

Following entries are passed on the re-issue of forfeited shares:

I. If the Forfeited Shares are reissued at par:

| Bank A/c Dr. | | |

| To Share Capital A/c | | |

| Bank A/c Dr. | | |

| To Share Capital A/c | | |

| To Securities Premium A/c | | |

III. If the forfeited shares are reissue at discount:

| Bank A/c Dr. | | |

| Share Forfeiture A/c | | |

| To Share Capital A/c | | |

-

Question 37

5 / -1

P and Q are partners sharing profits and losses in the ratio of 2:1 with capitals Rs. 1,00,000 and Rs. 80,000 respectively. The interest on capital has been provided to them @ 8% instead of 10%. In the adjustment entry, Q will be:

Solution

The correct answer is Credited by Rs. 400.

Key Points Adjustment entry- are journal entries made at the conclusion of an accounting period to correct the accounts to reflect the current period's revenues and expenses.

Treatment of past adjustments: After the final accounts have been prepared, some omission or commissions are noticed say in respect of the interest on capital, interest on drawings, partner’s salary, commission, etc. necessary adjustments required and these past adjustments can be rectifying two ways-

- Through Profit and Loss Adjustment Account

- Directly in Partners’ Capital Accounts

Important Points

Statement showing Net Effect of Omitting Interest on Capitals:

| Particulars | P(Rs.) | Q(Rs.) | Total |

| 1. Amount which should have been credited by way of interest on capital | 10,000 (Cr.) | 8,000 (Cr.) | 18,000 |

| 2. The amount actually credited as way of interest on capital will be debited. | 8,000 (Dr.) | 6,400 (Dr.) | (14,400) |

| 3. Loss to firm distributed in 2:1 in partners account | 2,400 (Dr.) | 1,200 (Dr.) | (3,600) |

Required Adjustment (diff. between 1,2 & 3) | 400 (excess will be debited) | 400(short will be credited) | 0 |

Adjustment entry from Directly in Partners’ Capital Accounts-

| Particulars | Dr. | Cr. |

| P's capital a/c Dr. | 400 | |

| To Q's capital A/c | | 400 |

| (Adjustment for omission of interest on capitals) | | |

Alternate Method Adjustment through Profit and Loss Adjustment Account -

| Particulars | Dr. | Cr. |

| P's capital A/c Dr. | 8,000 | |

| Q's capital a/c Dr. | 6,400 | |

| To Profit and Loss Adjustment A/c | | 14,400 |

| (entry for interest on capital reversed) | | |

| Profit and Loss Adjustment A/c Dr. | 18,000 | |

| To P's capital A/c | | 10,000 |

| To Q's capital a/c | | 8,000 |

| (correct amount of int. On capital credited) | | |

| P's capital A/c Dr. | 2,400 | |

| Q's capital a/c Dr. | 1,200 | |

| To Profit and Loss Adjustment A/c | | 3,600 |

| (loss on adjustment ) | | |

Mistake PointsDon't forget to calculate Profit / loss on Adjustment of firm as a result of rectification

Mistake PointsDon't forget to calculate Profit / loss on Adjustment of firm as a result of rectification

-

Question 38

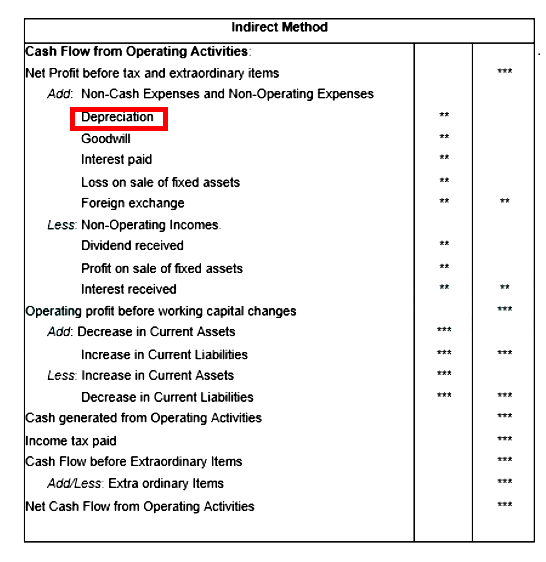

5 / -1

Which of the following will be added to Net Profit before Tax?

Solution

The correct answer is Depreciation.

Key PointsThe correct answer is depreciation because while preparing cash flow statement from indirect method all non cash expenses or non-operating expenses are added back to Net Profit before tax.

Depreciation is a Non-Cash expenses that is why it is added back to Net Profit before tax.

Important Points

-

Question 39

5 / -1

Match the items given in Column I with the heading/subheadings (Balance sheet) as defined in Schedule III of Companies Act,2013.

| | Column I | | Column II |

| (I) | Short term loan | (a) | Other current liabilities |

| (II) | Short term loans and advances | (b) | Short term borrowing |

| (III) | Debentures | (c) | Long term borrowings |

| (IV) | Debentures redeemable during current year | (d) | Current investments |

Solution

The correct answer is I - (b), II - (d), III - (c), IV - (a).

Key Points

| | Column I | | Column II |

| I | Short term Loan | (b) | Short term borrowing |

| II | short term loans and advances | (d) | Current Investments |

| III | Debentures | (c) | Long term borrowings |

| IV | Debentures redeemable during current year | (a) | Other current liabilities |

Important Points

- Short term Loan: As the name suggests, this loan is availed for meeting the short term needs of the business. Therefore, it is considered as short term borrowings.

- Short term loans and advances: These are the loans and advances that the company gives to third party for short term. These are considered as current investments.

- Debentures: Debentures are a debt instrument used by companies and government to issue the loan. The loan is issued to corporates based on their reputation at a fixed rate of interest. These are availed for long term and hence, are considered as long term borrowings.

- Debentures redeemable during current year: Since debentures redeemable are during current year, they are considered as current liabilities and are mentioned in Other current liabilities.

-

Question 40

5 / -1

Zee Ltd issued 15,000 equity shares of Rs. 20 each at a premium of Rs. 5 payable Rs. 5 on application, Rs. 10 on allotment (including premium) and the balance on first and final call. The company received applications for 22,500 shares and allotment was made pro rata. Bittoo to whom 1,200 shares were allotted, failed to pay the amount due on allotment. Identify the number of shares Bittoo applied for.

Solution

The correct answer is 1,800 Shares.

Key PointsPro Data Basis-when the company received over applicants which are offer to the public, then company to decides to proportionate ratio allotment to all applicants is called pro data basis. Excess application money received can be adjusted with allotment or refunded.

Important Points

Total Application received - 22500 shares

Total Application offer- 15000 shares

Bittoo applied for shares= let A

Bittoo allotted shares = 1200 shares

Bittoo share of Application money =1200 x 5= Rs.6000

Shares to be allotted = shares offered/total application received x no. of share applied by Bittoo

Shares allotted to Bittoo = 15000/22500 x A

1200 = 15000/22500 x A

A = 1200 x 22500 /15000

A = 1800 Shares

Thus. Bittoo applied for share are 1800.

Additional Information

Actual Application money of Bittoo =1800 x 2= Rs.9,000

Excess Application Money =Rs.9000 - Rs.6000 =Rs.3000

Excess application money to be adjusted with allotment =Rs.3000.

-

Question 41

5 / -1

A, B and C are equal partners, they wanted to change the profit sharing ratio to 4 : 3 : 2. They raised the goodwill to Rs. 90,000. The effected accounts will be

Solution

The correct answer is A's Capital A/c Dr. 10,000

To C's Capital A/c 10,000.

Key PointsOld Ratio = 1:1:1

New Ratio = 4:3:2

Gain or Sacrifice:

A's Share = 1/3 - 4/9 = -1/9 (Gain)

B's Share = 1/3 - 3/9 = 0

C's Share = 1/3 - 2/9 = 1/9 (Sacrifice)

Since, A has gained he will be debited from 1/9 x 90,000 = 10,000

Since, C has sacrifice he will be credited from 1/9 x 90,000 = 10,000

Adjustment Entry are as follows:

| |

Particulars |

Dr. |

Cr. |

| |

A's Capital A/c Dr. |

10,000 |

|

| |

To C's Capital A/c |

|

10,000 |

| |

( Adjustment for goodwill due to change in profit sharing ratio) |

|

|

-

Question 42

5 / -1

Revenue from Operations Rs. 2,00,000; Inventory Turnover ratio 5; Gross Profit 25%. Find out the value of Closing Inventory, if Closing Inventory is Rs. 8,000 more than the Opening Inventory.

Solution

The correct answer is Rs. 36,000.

Key PointsInventory Turnover Ratio: This ratio indicates the relationship between the cost of revenue from operation during the year and average inventory kept during that year.

Inventory Turnover Ratio = Cost of revenue from operations / Average Inventory = ........times

Cost of Revenue from operations can be calculated by two ways :-

- Cost of Revenue from operations = Opening Inventory + Purchases + Carriage + Wages + Other Direct Charges - Closing Inventory ,or

- Cost of Revenue from Operations = Net Revenue from operations - Gross Profits

- Average Inventory = Opening Inventory + Closing Inventory / 2

Important Points

Inventory Turnover Ratio = Cost of Revenue from Operations / Average Inventory

Gross Profit 25% (given), therefore goods costing Rs. 100 is sold for Rs.125

Hence, if Revenue from Operations is Rs. 125

Cost of Revenue from Operation are Rs. 100

If Revenue from Operations is Rs. 2,00,000

Cost of Revenue from Operations = 100/125 x 2,00,000 = 1,60,000

Inventory Turnover Ratio = 5 (given)

Hence, Inventory Turnover Ratio = Cost of Revenue from Operations / Average Inventory

5 = 1,60,000 / Average Inventory

Average Inventory = 1,60,000/5 = 32,000

Closing Inventory is Rs. 8,000 more than Opening Inventory

Suppose Opening Inventory = x

then, Closing Inventory = x + 8,000

Average Inventory = Opening Inventory + Closing Inventory / 2

Hence, 32,000 = x + x+ 8,000 / 2

32,000 = 2x + 8,000 / 2

64,000 = 2x + 8,000

64,000 - 8,000 = 2x

56,000 = 2x

hence, x = 28,000

opening inventory =28,000

Hence, closing Inventory = 28,000 + 8,000 = 36,000

-

Question 43

5 / -1

These shares which in addition to the fixed preference dividend, carry a right to participate in the surplus profits, if any, after, dividend at a stipulated rate has been paid to the equity share holders are called:

Solution

The correct answer is Participating preference shares.

Key Points

- The correct answer is participating preference share because, these shares allow shareholders to demand a portion of the company's surplus profit if the company is liquidated after dividends have been paid to the other shareholders.

- In other words, these shareholders receive fixed dividends and share a portion of the company's surplus profit with equity shareholders.

Important PointsConvertible Preference Share : Convertible preference shares are a type of share that allows shareholders to convert their preference shares into equity shares at a fixed rate after a specified period, as specified in the memorandum of understanding.

Redeemable Preference shares: Redeemable preference shares are those that can be repurchased or redeemed at a fixed rate and date by the issuing company. These types of shares benefit the company by acting as a buffer during times of inflation.

Cumulative Preference Shares: Cumulative preference shares are a type of share that entitles shareholders to a cumulative dividend payout even when the company is losing money. These dividends will be counted as arrears in years when the company is not profitable and will be paid cumulatively the following year when the business is profitable.

Additional InformationPreference Shares : The funds raised by a corporation by issuing preference shares are known as preference share capital (also known as Preference stock). Even before equity owners, preference shareholders have the first claim to dividends.

There are various types of preference shares which are as follows:

- Cumulative Preference Shares: Cumulative preference shares are a type of share that entitles shareholders to a cumulative dividend payout even when the company is losing money. These dividends will be counted as arrears in years when the company is not profitable and will be paid cumulatively the following year when the business is profitable.

- Non-cumulative Preference Shares: Dividends in arrears are not accumulated in these sorts of shares. In the case of non-cumulative preference shares, the dividend is paid out of the company's profits for the current year. If the company does not generate a profit in a given year, the shareholders are not paid dividends for that year and are not eligible for dividends in subsequent profit years.

- Participating Preference Shares : These shares allow shareholders to demand a portion of the company's surplus profit if the company is liquidated after dividends have been paid to the other shareholders. In other words, these shareholders receive fixed dividends and share a portion of the company's surplus profit with equity shareholders

- Non-Participating Preference Shares: These shares do not provide shareholders with the option of receiving dividends from the company's surplus profits. The stockholders are only paid the fixed dividend in this instance.

- Convertible Preference Shares: Convertible preference shares are a type of share that allows shareholders to convert their preference shares into equity shares at a fixed rate after a specified period, as specified in the memorandum of understanding.

- Non- Convertible Preference Shares: Preference shares of this type cannot be converted into equity shares. These shares will only receive a fixed dividend payout and will receive a preferred dividend payout upon a company's demise.

- Redeemable Preference Shares: Redeemable preference shares are those that can be repurchased or redeemed at a set rate and date by the issuing business. These shares benefit the corporation by acting as a cushion during periods of high inflation.

- Non - Redeemable Preference Shares: Non-redeemable preference shares are ones that cannot be redeemed at any moment throughout the company's lifetime. In other words, these shares can only be redeemed when the firm is wound up.

-

Question 44

5 / -1

_______% will be transferred to Debentures Redemption reserve when redemption is purely out of profit in case of banking company.

Solution

The correct answer is 0%.

Key Points 0 % will be transferred to Debentures Redemption reserve when redemption is purely out of profit in case of banking company, because there is exemption to create Debenture Redemption Reserve to:

- All India Financial Institutions (AIFIs) regulated by RBI

- Banking Companies.

Important Points

Debenture Redemption Reserve : The payment of the amount of debentures by the company is referred to as debenture redemption. Liability on account of debentures is discharged when debentures are recovered. To put it another way, the quantity of capital required to redeem debentures is substantial, therefore economic businesses set aside sufficient profits and accumulate capital to reclaim debentures.

There are four ways of redemption of debentures which are as follows:

- Payment in lumpsum

- Payment in installments

- Purchase in the open market

- By conversion into shares or new debentures.

-

Question 45

5 / -1

U, V and W are partners sharing profits in the ratio of 2:3:5. Their new ratio will be 5:3:2. They also decide to record the effect of the following revaluations and reassessments without affecting the book values of assets and liabilities by passing a single adjustment entry:

| | Book Value | Revised Value (Rs.) |

| Land and Building | 3,00,000 | 3,50,000 |

| Furniture | 1,50,000 | 1,00,000 |

| Sundry Creditors | 60,000 | 20,000 |

| Outstanding Salaries | 10,000 | 15,000 |

Solution

The correct answer is Dr. U and Cr. W by Rs. 10,500.

Key PointsRevaluation account - records change in the value of the firm’s assets & liabilities on admission or retirement or Death of the partner. The profit & loss on Revaluation A/c will be distributed in Old profit & loss ratio among the old partners.

Important Points Calculation of sacrifice ratio -

Sacrifice Ratio= Old Ratio - New Ratio

U's share = 2/10 - 5/10 = - 3/10( here U is gaining)

V's share = 3/10 - 3/10 = 0

W's share = 5/10 - 2/10 = 3/10

Calculation of Profit/loss on revaluation of assets and Liabilities -

| Particulars | Amount |

| Add - Assets appreciated & Liabilities Decreased | |

| Land & building (350000-300000) | 50,000 |

| Sundry creditor (60000 - 20000) | 40,000 |

Subtract -Assets Depreciated & Liabilities increased | |

| Furniture(150000-100000) | (50,000) |

| Outstanding Salaries(15000-10000) | (5,000) |

| Total Profit on revaluation of assets & liabilities | 35,000 |

Partner's share in profit on revaluation of assets and Liabilities without affecting the book values will be distributed on sacrifice/gaining ratio.

U's share = Rs.35,000 x 3/10 = Rs.10,500 (gain)

W's share = Rs.35,000 x 3/10 = Rs.10,500 (sacrifice)

Single adjustment entry will be :

| Particulars | Dr. | Cr. |

| U's Capital A/c Dr. | 10,500 | |

| To W's Capital A/c | | 10,500 |

| (profit on revaluation of assets and Liabilities without affecting the book values is distributed) | | |

-

Question 46

5 / -1

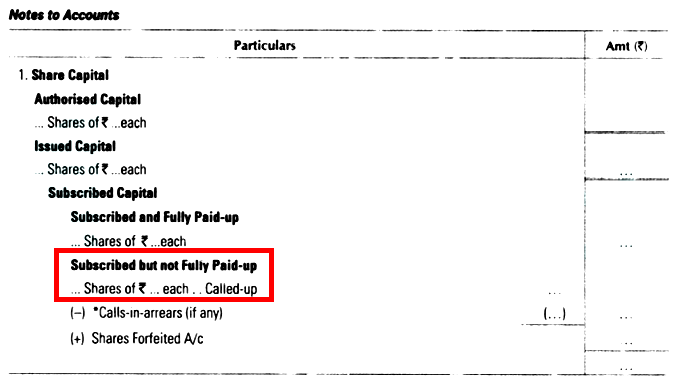

Share Capital of a company consists of 70,000 shares of Rs. 10 each, Rs. 8 called up. All the shareholders have duly paid the called up amount. Share capital will be shown as:

Solution

The correct answer is subscribed but not yet fully paid.

Key PointsThe correct answer is subscribed but not yet fully paid because shareholders have not paid some part of nominal value of shares i.e., Rs. 10.

Important PointsSubscribed but not fully paid up: Shares are said to be "Subscribed but not fully paid-up' under the following two situations:

(a) When the company has called-up the full nominal value of the share, but the shareholder has not paid some part of the nominal value of the share.

(b) When the company has not called-up the full nominal value of the share.

Subscribed and fully paid: When the entire nominal (face) value of a share is called by the company and also paid up by the shareholder, it is said to be 'Subscribed and fully paid-up' Capital.

-

Question 47

5 / -1

Total Assets at the end are Rs.2,25,000. External Liabilities are Rs. 1,00,000. If surplus for the year is Rs. 20,000, Opening Capital Fund will be:`

Solution

The correct answer is Rs. 1,05,000.

Key Points

- Capital fund can be defined as the excess of an organization's assets over its liabilities in the case of a non-profit organisation.

- Any excess or deficit found in the income and expense account is added to (or subtracted from) the capital fund. Accumulated Fund is the name for this type of fund.

Calculation of Capital Fund

| Capital Fund At the beginning of the year | |

| Add: Surplus from Income and Expenditure Account | xxx |

| Add: Subscription Amount (Capitalised Amount) | xxx |

| Add: Life Membership Fee | xxx |

| Less: Deficit from Income and Expenditure Account | (xxx) |

| Capital at the end of the year | xxx |

Important Points Opening Capital Fund = Total Assets - External Liabilities - Surplus

Hence, Opening capital fund = 2,25,000 - 1,00,000 - 20,000 = 1,05,000.

-

Question 48

5 / -1

X, Y and Z are partners sharing profits and losses in the ratio of 5:3:2. from 1st April 2018 they decided to share profit and losses equally. The partnership Deed provides that in the event of any change in the profit sharing ratio, the goodwill should be valued at 2 years purchase of the average profit of the preceding five years. The profit and loss of the preceding years are:

Adjustment entry will be

Solution

The correct answer is Dr. Y's Capital A/c Rs. 3,000, Z's Capital A/c Rs. 12,000, Cr. X's Capital A/c Rs. 15,000.