-

Question 1

5 / -1

Change in the relationship of existing partners which results in coming to an end in agreement and a new agreement coming into effect is:

Solution

The correct answer is Reconstitution of Partnership.

Key PointsPartnership - A relationship between people who have agreed to split the profits of a firm that is run by all of them or by any of them acting on behalf of all of them.

Key PointsPartnership - A relationship between people who have agreed to split the profits of a firm that is run by all of them or by any of them acting on behalf of all of them.

Partnership agreement -refers to a document that outlines the terms of the partnership as agreed upon by the partners.

Important PointsThe term "reconstitution of partnership" refers to a change in the existing partners' relationship. It is a change in partnership, i.e., reconstitution of partnership, because the current agreement has come to an end and a new agreement has taken effect.

Important PointsThe term "reconstitution of partnership" refers to a change in the existing partners' relationship. It is a change in partnership, i.e., reconstitution of partnership, because the current agreement has come to an end and a new agreement has taken effect.

Thus, Change in the relationship of existing partners which results in coming to an end in agreement and a new agreement coming into effect is Reconstitution of Partnership.

Additional InformationRevaluation of Partnership - "Reassessing the value of something" is the definition of revaluation. Such a review is carried out in the case of a change in a business's initial partnership. Only a company's assets and liabilities are revalued, and a "Revaluation Account" is set up to track the profit or loss.

Additional InformationRevaluation of Partnership - "Reassessing the value of something" is the definition of revaluation. Such a review is carried out in the case of a change in a business's initial partnership. Only a company's assets and liabilities are revalued, and a "Revaluation Account" is set up to track the profit or loss.

Realisation of Partnership - A dissolution account is formed when a partnership business dissolves. A realisation account must be constructed to determine profits or losses when the partnership entity is dissolved.

Dissolution of Firm - According to Section 39 of the partnership Act 1932, the dissolution of partnership between all the partners of a firm is called the dissolution of the firm. This brings an end to existing business firm.

-

Question 2

5 / -1

Balance sheet of a company is required to be prepared in the format given in ______

Solution

The answer is Schedule III Part I.

Key PointsFinancial Statement - Financial statements are the basic and formal annual reports that business management uses to communicate financial information to its owners and other external parties such as investors, tax authorities, the government, and employees. Financial statement are prepared at the end of the accounting period-

- Statement of profit and loss

- Cash flow statement

- Balance sheet

Important PointsBalance sheet - On a given date, the balance sheet shows all of the company's assets, all of its commitments or liabilities to outsiders or creditors, and all of the owners' claims. It is one of the most essential expressions describing an organization's financial situation, status, or strength.

As per Section 129 of Companies Act 2013, Financial Statement shall give a true & Fair view of the state of affairs of the company and should comply with accounting standards under section 133 and in form of prescribed format under Schedule III of the Companies Act.

Balance Sheet as per form set out Part 1 of Schedule III and Profit & Loss as per Part II of Schedule III.

It does not apply to

(i) Insurance or Banking Company,

(ii) Company for which a form of balance sheet or income statement is specified under any other Act.

Thus, the Balance sheet of a company is required to be prepared in the format given in Part I of Schedule III of Companies Act 2013.

-

Question 3

5 / -1

Revenue from Operations Rs.4,00,000; Cost of Revenue from Operations 60% of Revenue from Operations; Operating expenses Rs.30,000 and rate of income tax is 40%. What will be the amount of profit after tax?

Solution

The correct answer is Rs.78,000.

Important Points Calculation of Profit After Tax

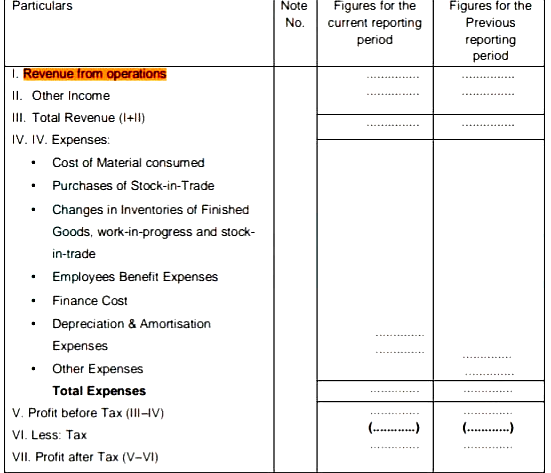

| | Particulars | Amount |

| I | Revenue from Operations | 4,00,000 |

| II | Other Income | --- |

| III | Total Income (I + II) | 4,00,000 |

| IV | Expenses

Cost of Revenue from Operations | 2,40,000 |

| | Operating Expenses | 30,000 |

| | Total Expenses | 2,70,000 |

| V | Profit before Tax (III - IV) | 1,30,000 |

| VI | Less: Income Tax @ 40% | (52,000) |

| VII | Profit after Tax | 78,000 |

Working Note :

Cost of Revenue from Operations = 60% of Revenue from Operations = 60/100 x 4,00,000 = 2,40,000

Income Tax = 40% = 40/100 x 1,30,000 = 52,000

-

Question 4

5 / -1

Match the column I with Column II

| | Column I | | Column II |

| 1. | Cash received against Debentures | a. | Issue of Debentures as collateral security |

| 2. | Assets received against Debentures | b. | Issue of Debentures for cash |

| 3. | Debentures given as secondary security | c. | Issue of Debentures in kind |

Solution

The correct answer is 1-b; 2- c; 3 –a.

| | Column I | | Column II |

| 1. | Cash received against Debentures | b. | Issue of Debentures for cash |

| 2. | Assets received against Debentures | c. | Issue of Debentures in kind |

| 3. | Debentures given as secondary security | a. | Issue of Debentures as collateral security |

Key PointsDebentures - marketable security (a type of investment) issued by a business or other organization to raise money for long-term activities and growth and yielding a fixed rate of interest. Debentures can be issued at par, at premium and at discount.

Important PointsIssue of Debentures for cash - The term "issue debenture for cash" refers to the corporation issuing a debenture to the applicant in exchange for cash.

Issue of Debentures as collateral security - A collateral security is defined as an additional security besides the primary security when a company obtains a loan from a bank or any other financial Institution.

Issue of Debentures in kind - Debentures can be issued for reasons other than cash. It's possible that the company bought assets from vendors or acquired another company. The corporation may then offer debentures to such vendors instead of paying cash. Thus,

- Issue of Debentures for cash received against Debentures

- Issue of Debentures as collateral security for Debentures given as secondary security

- Issue of Debentures in kind for Assets received against Debentures.

Additional InformationMethods for treatment of issue of Debenture as collateral securities -

There are two methods when debentures are issued as collateral security:

1. When company decides not to create liability - No entry will be made in the books of accounts since no liability is created on such issue.

2. When company decides to create liability - Debenture suspense account will be debited on issue of debenture as security.

-

Question 5

5 / -1

A company issued 4,000 equity shares of Rs. 50 each at par payable under: On application 20%, on allotment 40% ; on first call 10% ; on final call-balance Applications were received for 10,000 shares. Allotment was made pro-rata. How much amount will be received in cash on allotment?

Solution

The correct answer is Rs. 20,000.

Key Points

Pro Rata allotment of shares: Pro rata allotment is a situation due to the oversubscription of shares. In this case, the company either returns the extra shares or adjusts the excess shares for future use while refunding the remaining ones. The number of shares granted to the general public is proportional to the number of shares sought for by the general public.

Important Points

| Particulars | | Amount |

| Application money received | 10000 x 10 | 1,00,000 |

| Less: Application money due | 4000 x 10 | (40000) |

| Excess Application money received | | 60000 |

| Less: Allotment money due on allotment | 4000 x 20 | 80000 |

| Amount to be received on allotment in cash | | (20000) |

Working Note:

Application = 20% of 50 = ₹10

Allotment = 40% of 50 = ₹20

-

Question 6

5 / -1

For an IF function to check whether cell B3 contains a value between 15 and 20 inclusively, what condition should you use?

Solution

The correct answer is AND (B3>=15,B3<=20).

Key Points

- In Excel, there can be 2 basic types of multiple conditions - with AND and OR logic. Consequently, your IF function should embed an AND or OR function in the logical test, respectively.

- AND function: If your logical test contains the AND function, Microsoft Excel returns TRUE if all the conditions are met; otherwise, it returns FALSE.

- OR function: In case you use the OR function in the logical test, Excel returns TRUE if any of the conditions are met; FALSE otherwise.

- Here B3 represents the cell, >=15 represents the value greater or equal to 15 and <= 20 represents the value less or equal to 20. The function AND checks, if the value lies between 15 and 20.

-

Question 7

5 / -1

X is admitted into the partnership for 1/4th share. The existing total capital of the firm is Rs. 4,50,000 The amount that X will bring in:

Solution

The correct answer is Rs.1,50,000.

Key PointsPartner's capital A/c- where all the transactions between the partners and the firm are recorded.

Determining or Adjusting Capital -

The capital of the partners may be modified to reflect their new profit sharing ratio. In that instance, the capital of the new partner is usually employed as a starting point for calculating the payout new capitals for the former partners, as well as case-by-case adjustments

Alternatively, funds can be transferred to a partner's current account. Other options may be available as well for determining the capitals of the partners after the new partner's admission such as immediately pooling the complete capital to be in the firm following admittance the new Partner.

Important Points

The existing total capital of the firm= Rs.4,50,000

X's share of Profit = 1/4

Shares of remaining Partner's in new firm= 1-1/4=3/4

Total New firm's capital = Existing capital of Firm /Shares of remaining Partner's in new firm

=Rs.4,50,000 x 4/3

=Rs.6,00,000

X's Share of Capital= X's Share of Profit x Total New firm's capital

= Rs.6,00,000 x 1/4

= Rs1,50,000

Thus, X's Capital will bring Rs.1,50,000 as Capital.

-

Question 8

5 / -1

Subscription received but not yet earned is considered as

Solution

The correct answer is Liability.

Key PointsUnearned revenue - is money you've received but haven't yet earned from your business. When insurance premiums, rent, membership fees, or maintenance contract fees are received before the consumer receives the agreed-upon benefit, they are considered unearned revenue.

Important PointsIncome received in advance is a liability in accounting because the company receiving the money has not yet earned it and has a liability/obligation to supply the relevant goods or services in the future. As a result, subscription fees received in advance is recognized as a obligation of the business.

Thus, Subscription received but not yet earned is considered as Liability of the business.

Additional Information Subscription earned but not received is considered as assets of the business. Income earned but not received are accrued income of the business.

- Accrued Income - Earned but unpaid money is referred to as accrued income. In the balance sheet, it is shown as a current asset. It must be recorded in the accounting period in which it occurs, rather than the period in which it will be received later.

-

Question 9

5 / -1

Daisy Limited forfeited 200 shares Rs. 10 each who had applied for 500 shares, issued at a premium of 10% for non-payment of final call of Rs. 3 per share. Out of these, 100 shares were issued as fully paid up for Rs. 15. The profit on reissue is:

Solution

The correct answer is Rs. 700.

Key Points

Share Forfeiture:

- The circumstance in which the allotted shares are cancelled by the issuing firm due to non-payment of the subscription amount as requested by the issuing company from the shareholder is referred to as forfeiture of shares.

- If a shareholder's shares are forfeited, the shareholder's rights and interests as a shareholder are lost, and the shareholder ceases to be a member of the organisation.

- Some shareholders may be unable to pay instalments, such as money allocation or call money. In such a case, consider the following:

- Their part will be forfeited, i.e., the shareholder's share would be cancelled.

- Apart from the premium entries already specified in the accounting records, all the entries related with the forfeited shares must have conversed.

- The amount is deducted from the share capital account.

Important Points

| | Particulars | L.F. | Dr. | Cr. |

| i. | Share Capital A/c Dr. (200x10) | | 2,000 | |

| | Securities Premium Reserve A/c Dr. (200x1) | | 200 | |

| | To Share Forfeiture A/c | | | 1,600 |

| | To Share Final Call A/c (200 x 3) | | | 600 |

| | (200 shares forfeited due to non-payment of final call) | | | |

| ii. | Bank A/c Dr. (100 x 15) | | 1,500 | |

| | To Share Capital A/c (100 x 10) | | | 1,000 |

| | To Securities Premium Reserve A/c (100 x 5) | | | 500 |

| | (100 shares re-issued @ Rs. 15) | | | |

| iii. | Share Forfeiture A/c Dr. | | 700 | |

| | To Capital Reserve A/c | | | 700 |

| | (Profit on reissue transferred to capital reserve) | | | |

Working Note:-

| Profit on 200 shares (200 x 8) | 1,600 |

| Amount received reissue of 100 shares (100 x 15) | 1,500 |

| Less: Profit received on 100 shares (100 x 8) | 800 |

| Amount of profit on reissue transferred to capital reserve | 700

|

-

Question 10

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R):

Assertion (A): The focus of calculation of working capital revolves around managing the operating cycle of the business.

Reason (R): It is because the concept of operating cycle is required to ascertain the liquidity of assets and urgency of payments to liabilities.

In the context of the above two statements, which of the following is correct?

Solution

The correct answer is Both (A) and (R) are true and (R) is a correct explanation of (A).

Key PointsAssertion (A): The focus of calculation of working capital revolves around managing the operating cycle of the business.

Assertion is true because, the operating cycle is useful for estimating the amount of working capital that a company will need in order to maintain or grow its business. A company with an extremely short operating cycle requires less cash to maintain its operations, and so can still grow while selling at relatively small profit margins. Conversely, a business may have high margins and yet still require additional financing to grow even if its operating cycle is somewhat long.

Reason (R): It is because the concept of operating cycle is required to ascertain the liquidity of assets and urgency of payments to liabilities.

Reason is true because, management decisions can impact the operating cycle of a business. Therefore, it is extremely important for every business to have a handle on its operating cycle, so it can predict how much working capital is either needed or on hand at a particular point. If your operating cycle is too long you may benefit from additional working capital to meet your current obligations. In this way the concept of operating cycle is required to ascertain the liquidity of assets and urgency of payments to liabilities.

Important PointsWorking Capital:-

- Working capital refers to money invested in current assets.

- It is the fund that is required to run the business on a daily basis.

- It circulates throughout the company like blood does in a living body.

- Working capital, in general, refers to a company's current assets that are converted from cash to inventory, inventory to work in progress (WIP), WIP to finished goods, finished goods to receivables, and receivables to cash in the usual course of business.

There are two types of working capital:

- Gross Working Capital

- Net Working Capital

Formula : Working Capital = Current Assets - Current Liabilities

-

Question 11

5 / -1

Debentures are issued as other than cash, number of debentures will be calculated as purchase price dividing by _________ of shares

Solution

The correct answer is Issue Price.

Key PointsWhen debentures are issued as other than cash, number of debentures will be calculated by following formula:-

No. of debentures issued = Purchase Consideration / Issue Price of a Debenture

Important PointsIssue of Debentures for Considerations other than Cash: Sometimes a company purchased assets from vendors and instead of making payment in cash issues debentures for consideration thereof. Such issue of debentures is called debentures issued for consideration other than cash. In that case also, the debentures may be issued at par, at a premium or at a discount then entries made in such a situation are similar to those of the shares issued for consideration other than cash, which are as follows :

1. On purchase of assets

Sundry Assets A/c Dr.

To Vendor’s

2.(a) On issue of debentures At par

(a) Vendors Dr.

To Debentures A/c

(b) At premium

Vendors Dr.

To Debentures A/c

To Securities Premium Reserve A/c

(c) At a discount

Vendors Dr.

Discount on Issue of Debenture A/c Dr.

To Debentures

Additional InformationDebentures : A debenture is a written instrument that bears the company's common seal and acknowledges a debt. It contains a contract for the return of principal after a specified period, at intervals, or at the company's discretion, and for the payment of interest at a fixed rate payable on fixed dates, usually half-yearly or yearly. 'Debenture' includes Debenture Inventory, Bonds, and any other securities of a company, whether or not they constitute a charge on the firm's assets, according to section 2(30) of The Companies Act, 2013.

-

Question 12

5 / -1

Current assets includes only those assets which are expected to be realized within _______

Solution

The correct answer is 1 year.

Key PointsA current asset is one that a business has and that may be easily sold or consumed, resulting in the conversion of liquid cash. A current asset is vital to a business since it allows them to utilise money on a day-to-day basis and clear current business expenses. To put it another way, current assets are assets that are only expected to survive a year or less.

Important PointsCurrent Assets : A current asset is one that a business has and that may be easily sold or consumed, resulting in the conversion of liquid cash. A current asset is vital to a business since it allows them to utilise money on a day-to-day basis and clear current business expenses. To put it another way, current assets are assets that are only expected to survive a year or less.

Additional InformationTypes of Current Assets

- Cash and cash equivalent

- Inventory

- Ongoing projects

- Pre-paid expenses

- Account receivable

- Marketable securities

Formula of Current Assets = Cash +Cash Equivalents+ Inventory+ Accounts Receivable+ Market Securities+ Prepaid Expenses+ Other Liquid Assets

Examples of Current Assets

- Cash and equivalents

- Short-term investments (marketable securities)

- Accounts receivable

- Inventory

- Prepaid expenses

- Any other liquid assets

-

Question 13

5 / -1

Identify the correct sequence of arguments for SLN function:

Solution

The correct answer is: (cost, salvage, life)

Key Points

- The SLN function is used to calculate the depreciation of a product on the basis of a straight line for one period.

- The syntax of the SLN function is like this: =SLN(cost, salvage, life)

- The straight line is the easiest way to calculate the depreciation of a fixed asset.

- The formula used in a straight-line method to calculate SLN is like this: \(SLN=\frac{cost-salvage}{life}\)

The arguments are described as:

- cost: The principal cost of an asset at the point of purchase.

- salvage: The value of an asset after the end of the depreciation.

- life: The life (in periods) of an asset over which the asset will get deprecated.

Example:

If an asset A whose value is 10000 and its salvage cost is 1000 after 24 months, then the formula becomes:

- Formula: =SLN(10000,1000,24)

- Result: 375.00 (Depreciation value of asset A for each month)

-

Question 14

5 / -1

X & Y are partners sharing profits equally. Y draw Rs. 1,000 at the beginning of each month for six months year ended on 31st March, 2019. If interest on drawing is to be charged @ 6% p.a The interest on drawings of Y will be:

Solution

The correct answer is Rs. 105.

Key Point

Interest on Drawing :

- Drawings are the funds taken out by the partners for personal purposes. It's the amount that's been taken out of profit. It is a temporary withdrawal made by the partners, which must be returned with interest.

- The amount of interest paid by the partners, computed with reference to the drawings, is known as interest on drawings. The time frame in which the funds were withdrawn.

- It is attributed to the Profit and Loss Appropriation since it is a profit for the company.

- It is a partner expense, hence it is deducted from the Partner's Capital Account.

- If it is stated in the Partnership Deed, the partners will be charged interest on the drawing.

When unequal amounts are withdrawn at different dates, there are two methods of calculating Interest on Drawings which are as follows:

- Simple Method : Interest on Drawings = Amount of Drawings x Rate/100 x No. of Months/12

- Product Method : Interest on Drawings = Total of Products x Rate/100 * 1/12

When equal amounts are withdrawn at regular interval of time, then Interest on Drawings can be calculated by following formula:-

Interest on Drawings = Total Amount of Drawings x Rate/100 x Average Period/12

Average Period = (No. Of months left after first drawings + No. of months left after last drawings)/2

Important PointsCalculation of Interest on Drawings

Number of Drawings = 6

Amount of each drawing = 1000

Total Drawings = 6x1000 = 6,000

Number of Months = (Time Left after first drawings + Time left after Last Drawings ) / 2

= (6 + 1)/2 =3.5 months

Hence, Interest on Drawings = 6,000 x 6/100 x 3.5/12 =Rs. 105

-

Question 15

5 / -1

From the following information find out the cash flow from financing activities

Liabilities:

Proposed Dividend

31st March 2013 - 20,000

31st March 2014 - 15,000

Additional Information: Equity Share Capital raised 3,00,000 10% Debentures Redeemed 1,00,000 Preference Share capital Redeemed 50,000. Interim Dividend paid during the year 20,000

Solution

The correct answer is Rs. 1,00,000.

Key PointsCash Flow from Financing Activities:

- The cash flow from financing activities (CFF) portion of a company's cash flow statement illustrates the net cash flows used to fund the business.

- Transactions involving debt, stock, and dividends are all examples of financing operations.

- Investors can see a company's financial strength and how well its capital structure is managed by looking at cash flow from financing operations.

Format of Cash Flow From Financing Activities

| Particulars | Details | Amount |

Proceeds from issue of Shares and Debentures | | |

| Proceeds from Other Long-term Borrowings | | |

| Proceeds from Short-term Borrowings: | | |

| (i)Increase in the Balance of Bank Overdraft and Cash Credit | | |

| Less: (ii) Decrease in the Balance of Bank Overdraft and Cash Credit | | |

| Payment of Interim Dividend | | |

| Payment of Proposed Dividend of Foregoing Year | | |

| Interest paid on Short-term and Long-term Borrowings | | |

| Interest paid on Bank Overdraft/Cash Credit | | |

| Repayment of Loans (Whether short-term or long-term) | | |

| Redemption of Debentures/Preference Shares | | |

| Net Cash Flow from Financing Activities | | |

Important PointsCalculation of Net Cash Flow from Financing Activities

| Particulars | Amount |

| Equity Share Capital raised | 3,00,000 |

| 10% debentures redeemed | (1,00,000) |

| Preference Share Capital redeemed | (50,000) |

| Interim Dividend Paid | (20,000) |

| Proposed Dividend (previous year) | (20,000) |

| Interest paid on Debentures | (10,000) |

| Net Cash Flow from Financing Activities | 1,00,000 |

Note: Proposed dividend for the current year is not taken into account as it has been proposed in current year but is paid in next year.

-

Question 16

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) : Equity shares do not carry fixed rate of dividend, and they are the ultimate risk bearer.

Reason (R) : Equity shareholders get dividend from residual part of profits and in the case of winding-up of the company, invested money will be refunded at the last.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Key PointsAssertion (A) : Equity shares do not carry fixed rate of dividend, and they are the ultimate risk bearer.

Assertion is true because, according to Section 43 of The Companies Act, 2013, an equity share is a share which is not a preference share. In other words, shares which do not enjoy any preferential right in the payment of dividend or repayment of capital, are termed as equity/ordinary shares. The dividend on equity shares is not fixed and it may vary from year to year depending upon the amount of profits available for distribution.

Reason (R) : Equity shareholders get dividend from residual part of profits and in the case of winding-up of the company, invested money will be refunded at the last.

Reason is true because, the equity shareholders are entitled to share the distributable profits of the company after satisfying the dividend rights of the preference shareholders and are paid in last.

Important PointsEquity Share : An equity share, also known as an ordinary share, is a fractional ownership of a trading business in which each member is a fractional owner and initiates the maximum entrepreneurial liability. Shareholders of this type have the ability to vote in any organisation.

Features of Equity Shares

- The corporation retains its equity share capital. It is only returned when the company is shut down.

- Equity Shareholders elect the company's management and have voting rights.

- The dividend rate on equity capital is determined by the availability of surplus capital. The dividend rate on the equity capital, on the other hand, is not fixed.

-

Question 17

5 / -1

A, B and C were partners sharing profits and losses in the ratio of 2:2:1. Books are closed on 31st March every year. C died on November 5, 2018. Under the Partnership deed the executors of the deceased partner are entitled to his share of profit to the date of death calculated on the basis of last year’s profit. Profit for the year ended 31st March 2018 was Rs. 2,40,000. C’s share of profit will be

Solution

The correct answer is Rs.25,680.

Key Points In case of Death of Partner, the sum due to decreased Partner is given to legal heir of representative\executor of Decreased Partner. the amount include in Decreased Partner's Capital Account up to the date of death are as Follows-

- credit balance of his capital account

- credit or debit balance of his current account (if any)

- his share of goodwill

- his share in the gains\losses of revaluation of assets and liabilities

- his share of accumulated profits\losses & reserves

- his share of profits\losses up to the date of death

- interest on his capital\ interest on his drawings

- salary/commission, if any etc.

Important PointsC died on November 5, 2018

No of days C's work as partner in Partnership Firm= 30+31+30+31+31+30+31+5

=219 days

C's Share of Profit =1/5

Profit for the year =Rs.2,40,000

C's share of Profit = Profit for the year x Share of Profit x No of days work as partner/total no. of days in year.

=Rs.2,40,000 x 1/5 x 219/365

=Rs.28,800

Thus, C's share of Profit in Year 2018 will be Rs.28,800.

-

Question 18

5 / -1

The formula for calculating Trade payable turnover ratio is:

Solution

The correct answer is Net credit purchases/ Avg trade payables

Key PointsTrade Payable Turnover Ratio :

Trade payables turnover ratio indicates the pattern of payment of trade payable. As trade payable arise on account of credit purchases, it expresses the relationship between credit purchases and trade payable.

It is calculated as follows:

Trade Payables Turnover ratio = Net Credit purchases/Average trade payable

Where Average Trade Payable = (Opening Creditors and Bills Payable + Closing Creditors and Bills Payable)/2

Average Payment Period =No. Of days/month in a year / Trade Payable Turnover Ratio

Important PointsImportance of Trade Payable Turnover Ratio

- It reveals average payment period.

- Lower ratio means credit allowed by the supplier is for a long period or it may reflect delayed payment to suppliers which is not a very good policy as it may affect the reputation of the business.

- The average period of payment can be worked out by days/months in a year by the Trade Payable Turnover Ratio.

-

Question 19

5 / -1

The profits for the previous three years are given below:

2018-2019 Rs. 23,000 (including an abnormal gain of Rs, 8,000)

2019-2020 Rs. 40,000 (after charging an abnormal loss of Rs. 12,000)

2020-2021 Rs. 38,000 (after writing off bad debts amounting to Rs. 6,000)

The amount of goodwill at two years purchase of the average profits of the last three years will be ______.

Solution

The correct answer is Rs. 70000

Key Points Goodwill:

- Goodwill is an intangible asset acquired when one company buys another.

- Goodwill is defined as the portion of the purchase price that exceeds the total of the net fair value of all assets acquired and liabilities taken during the transaction.

Important Points

- Only the Normal Profits must be considered when assessing the value of goodwill based on the profits of the company.

- To compute Normal Profits for the given time, any sort of abnormal loss is added back and any type of abnormal gain is subtracted from the given Profits.

Calculation of value of goodwill:

| Year | Net profit | Abnormal Profit/Loss | Adjusted Net Profit |

| 2018 - 2019 | 23000 | Less: Abnormal Profit: (8000) | 15000 |

| 2019 - 2020 | 40000 | Add: Abnormal Loss: 12000 | 52000 |

| 2020 - 2021 | 38000 | ----- | 38000 |

| Total | 105000 |

Total Adjusted Profit = 105000

Average Profit = 105000 / 3 = 35000

Goodwill = Average Profits x Number of Years purchase

Goodwill = 35000 x 2 = Rs. 70,000

-

Question 20

5 / -1

In case of dissolution of partnership there was no workmen compensation fund and firm had to pay Rs3000 as compensation to workers where will be this Rs3000 recorded in the books of accounts?

Solution

The correct answer is debit side of realisation account.

Key Points

Dissolution of partnership - dissolution of partnership changes the existing relationship between partners but the firm may continue its business as before

Workmen Compensation Fund -fund created out of firm’s profits to pay compensation to employees.

Important PointsA payment is paid to compensate a worker at the time of dissolution of a partnership,

If there is no workmen compensation fund - amount of worker's compensation paid in cash is debited in realisation account. The Liabilities realised at the time of Dissolution of firm is recorded in realisation account.

| Particulars | Dr. | Cr. |

| Realisation A/c Dr. | 3,000 | |

| To cash A/c | | 3,000 |

| (amount of compensation paid to worker's) | | |

Thus, Rs.3000 paid as compensation to workers will be recorded in the debit side of Realisation Account.

Additional InformationIf there is an amount in workmen compensation fund then treatment of worker's compensation will be in the following way-

- if amount paid to workmen compensation fund is equal to worker's compensation - workmen Compensation Reserve is transferred to Realisation Account

- If the amount paid to workmen compensation fund is more than worker's compensation - The amount of worker’s compensation is transferred to Realisation Account and excess Workmen Reserve over the Workmen Compensation Claim is credited to partners in their profit sharing ratio.

- If the amount paid to workmen compensation fund is less than worker's compensation - The amount of Workmen Compensation reserve is transferred to Realisation Account. And remaining amount is adjusted in realisation & cash account.

-

Question 21

5 / -1

What will be the output of the following formula in Excel if today is 15 July 2022:

=DATE(YEAR(TODAY()),MONTH(TODAY()),12)

Solution

The correct answer is: 7/12/2022

Key Points

- The syntax for the DATE function in excel is like this: =DATE(year, month, day)

- The syntax for the Today function in excel is like this: =TODAY()

- The syntax for the Year, Month, and Day functions are like this respectively:

- =Year(Serial Number)

- =Month(Serial Number)

- =Day(Serial Number)

- The formula Year(Today()) will result as, Year(15-July-2022).

- Now, the Year function fetches the year from the serial number (a valid excel date (15-July-2022)), which is 2022, and passes it an argument in the DATE function.

- The Month function fetches the month from the serial number 15-July-2022 and passes this an argument for the DATE function.

- The value 12 is already passed as the argument for the day in the DATE function.

- As a result, the final result for the function becomes 7/12/2022.

-

Question 22

5 / -1

Mahima Limited has an authorised capital of Rs. 10,00,00,00 divided into 1,00,000 equity shares of Rs. 10 each. It offered 90,000 equity shares at Rs.10 each at a premium of Rs. 8. The public applied for 81,000 equity shares. Till 31st March 2018, Rs. 17 (including premium) was called. An applicant holding 5000 shares did not pay first call of Rs. 2 per share.

As per the above given information ______ is the amount of share capital to be shown in the balance sheet of the company.

Solution

The correct answer is ₹ 7,19,000

Key Points

Authorised Capital: The amount of share capital in which a corporation is permitted to issue its Memorandum of Association is known as authorised capital. The corporation is not permitted to raise more capital than specified in the Memorandum of Association. It's also known as Nominal or Registered capital.

Issued capital - The part of the allowed capital that is actually offered to the public for subscription, including the shares granted to vendors and signatories to the company's memorandum, is known as issued capital.

Subscribed Capital - It is the portion of the issued capital that has been subscribed by the general public. When the public shares offered for public subscription are fully subscribed, the issued capital and subscribed capital are equal.

Called up Capital : The amount of share capital that the shareholders owe and are yet to be paid is known as called up capital. It is that part of the share capital that the company calls for payment.

Important Points

| Particulars | Rs. |

| Share Capital | |

| Authorized or Registered or Nominal Capital | |

1,00,000 shares of each Rs.10 | 10,00,000 |

| | |

| Issued Capital | |

| 90,000 Shares of Each Rs.10 | 9,00,000 |

| | |

| Subscribed Capital | |

| Subscribed but not fully paid up | |

| 81,000 Shares of Rs.10 each, Rs.9 called up (excl. premium) | 729000 |

| Less: Calls in Arrears (5000 x 2) | (10,000) |

| Share capital to be shown in balance sheet | 7,19,000 |

-

Question 23

5 / -1

A and B were partners. They shared profits as A- 1/2 ; B- 1/3 and carried to reserve 1/6. B died. The balance of reserve on the date of death was Rs. 30,000. B’s share of reserve will be:

Solution

The correct answer is Rs. 12000

Important Points A : B : Reserve = 1/2 : 1/3 : 1/6 = 3 : 2 : 1

Profit sharing Ratio A : B = 3 : 2

Balance of reserve on the date of death = Rs. 30000

At the time of retirement or death of the partner, the Balance in reserves and other accumulated profit is distributed among partners in old ratio.

B's share in Reserve = 30000 x 2/5 = Rs. 12000.

-

Question 24

5 / -1

Share capital Rs. 8,00,000; Reserve and surplus Rs. 4,00,000; General reserve Rs.1,00,000 and Total assets Rs. 20,00,000. Proprietary ratio will be:

Solution

The correct answer is 0.60:1

Key Points Proprietary Ratio:

- The proprietary ratio is a form of solvency ratio that can be used to calculate the quantity or contribution of owners or proprietors to the total assets of a company.

- The equity ratio, also known as the shareholder equity ratio or the net worth ratio, is a measure of a company's financial strength.

- The main goal of this ratio is to figure out what percentage of a company's total assets is supported by the owners.

- It also indicates how much the shareholders will receive in the event of liquidation of the company.

- A high proprietary ratio implies that a company is in a strong position and can provide relief to creditors, whereas a low proprietary ratio suggests that the company is reliant on debt financing to operate.

Formula: Proprietary Ratio = Proprietors Funds / Total Assets

Important PointsShare capital = Rs. 8,00,000 (Given)

Reserve and surplus = Rs. 4,00,000 (Given)

General reserve = Rs.1,00,000 (Given)

Total assets = Rs. 20,00,000 (Given)

Shareholder's Fund or Proprietors Fund = Equity Capital + Preference Capital + Reserves and Surplus

Shareholder's Fund or Proprietors Fund = 8,00,000 + 4,00,000 = 12,00,000

Proprietary Ratio = Proprietors Funds / Total Assets

Proprietary Ratio = 12,00,000 / 20,00,000

Proprietary Ratio = 0.6 : 1

When expressed in the form of a percentage, it comes to 60%. It means 60% funds of the business are financed by the proprietors.

-

Question 25

5 / -1

A and B are partners sharing profits in the ratio of 2 : 3. Their Balance Sheet shows machinery at Rs. 4,00,000; stock at Rs. 80,000 and debtors, at Rs. 3,20,000. C is admitted and new profit sharing ratio is agreed at 6 : 9 : 5. Machinery is revalued at Rs. 3,40,000 and a provision is made for doubtful debts @2.5%. A's share in loss on revaluation amounted to Rs. 20,000. Revalued value of stock will be:

Solution

The correct answer is Rs. 98,000.

Key PointsRevaluation Account - Records change in the value of the firm’s assets & liabilities on admission or retirement or Death of the partner. The profit & loss on Revaluation A/c will be distributed in Old profit & loss ratio among the old partners.

Important Points Revaluation A/c

Dr. Cr.

| Particulars | Amount | Particulars | Amount |

| To Machinery A/c | 60,000 | By Stock A/c

(Bal. fig.) | 18,000 |

| To Provision for bad debts | 8,000 | By Partner's Capital A/c(Loss) A's capital 20,000 B's capital 30,000 | 50,000 |

Working Notes:

- Decrease in value of Machinery = Rs.4,00,000- Rs.3,40,000 =Rs.60,000

- Amount on Provision for Bad debts = Rs.3,20,000 x 20%= Rs.8,000

- Calculations of Loss of firm-

Loss debited in A's capital =Rs.20,000

A's old Profit & loss Ratio= 2/5

Loss of Firm = Loss debited in A's capital / A's old Profit & loss Ratio

=Rs.20,000 x 5/2

=Rs.50,000

Increase in value of Stock= Rs.60000+ Rs.8,000-50,000

=Rs.18,000

Thus, Revalued Value of Stock will be Rs.98,000 (Rs.80000+Rs.18000).

-

Question 26

5 / -1

Which of the following is components of MS Access?

Solution

The correct answer is option 4.

Concept:

MS Access:

MS Access or Microsoft Access is Database Management System (DBMS) by Microsoft. In Microsoft Access, Jet Database Engine is merged with the Graphical User Interface (GUI) and Software development tools.

There are seven major components of Microsoft Access:

Tables:

In MS Access Tables store the data or the information that we feed the program.

Relationships:

The connections that arise between one or more tables are known as relationships. So there are one-on-one connections, one-to-many relationships, and, of course, many-to-many ties.

Queries:

Queries are when the user or the programmer requests the database for information.

Forms:

This is an object class that enables a programmer or designer to develop an MS Access user interface. Tables and queries are what make up a form.

Reports:

The user will wish to examine the information once all of the data has been entered into the database.

Macros:

Macros are Microsoft Access capabilities that let you automate actions on your forms and reports.

Modules:

These are the software's foundations, which enable a programmer to design a series of predetermined instructions known as sub-routines.

Hence the correct answer is All the above.

-

Question 27

5 / -1

Interest and dividend earned by financial company is shown in Statement of Profit & Loss under the sub-head:

Solution

The correct answer is Revenue from Operations.

Key Points

Revenue from Operations: It refers to the revenue earned by the company from its business operations. As in the given question, the company is financial in nature that's why interest earned and dividend are counted in day to day operations of the company.

Important PointsInterest earned by a Financial company: Interest is a fee charged by a lender to a borrower for lending money. In financial company, these transactions are done on daily basis that's why it is recorded under revenue from operation heading.

Dividend Earned by Financial Company Dividends are payments made by a firm to its stockholders to share profits. They're paid on a regular basis, and they're one among the ways that stock investors might profit from their investments.

Additional InformationOther Income: It refers to the revenue earned by the company from activities other than its business operations.

For Example:

- Interest Income

- Dividend received

- Profit on sale of Investments or fixed assets.

- Bad debts recovered

- Excess provision written back

- Rental Income etc.

-

Question 28

5 / -1

Section 41 of partnership act 1932 deals with dissolution of a firm

Solution

The correct answer is compulsory dissolution.

Key PointsDissolution of a firm - the dissolution of a partnership between all the partners of a firm is called the dissolution of the firm. This brings end to existing business firm. This is defined under Section 39 of the Partnership Act of 1932.

Important Points

Compulsory dissolution -

A firm is dissolved compulsorily in the following circumstances:

(a) when all of the partners, or all but one, become insolvent, rendering them incompetent to sign a contract;

(b) when the firm's business becomes illegal; or

(c) when some event occurs that makes it illegal for the partners to carry on the firm's business in partnership, such as when a partner who is a citizen of a country becomes an alien enemy due to the declaration of war with that country.

This sort of compulsory dissolution is defined in Section 41 of the Indian Partnership Act of 1932.

Additional Information

By mutual agreement - Partners can dissolve a partnership by agreement and with the approval of all partners, according to Section 40 of the Indian Partnership Act, 1932. A contract that has already been made can also be used to terminate a partnership. A firm is dissolved :

(a) with the consent of all the partners or

(b) in accordance with a contract between the partners

By notice - In the event of a partnership at will, the firm can be dissolved if one of the partners sends the other partners written notice of his desire to dissolve the partnership.

By order of court - A partnership firm may be dissolved at the request of a partner for any of the following reasons:

- when a partner goes insane;

- when a partner becomes permanently incapable of performing his partner obligations.

- when a partner engages in conduct that is likely to harm the firm's business;

- when a partner repeatedly breaches the partnership agreement;

- when a partner has transferred the entirety of his interest in the firm to a third party;

- when the firm's business cannot be carried on except at a loss; or

- when the court determines that dissolution is just and equitable on any ground.

-

Question 29

5 / -1

All of the following would be included in company's Operating Activities except

Solution

The correct answer is Interest on Current Investment.

Key PointsInterest on current Investment will not come under Operating Activities, it will come under investing activities of Cash Flow Statement since interest results in inflow of cash on investments made by company.

Important PointsCash Flow From Operating Activities: A company's major revenue-generating activities are its operating operations. As a result, they include cash flows from operations and events that are utilised to determine the net profit or loss of the company. Here are some instances of cash flows generated by business operations:

- Cash receipts from the sale of products and performance of services.

- Cash revenue from taxes, fees, commissions, and other sources.

- Cash receipts from debtors and payables

- Cash receipts for purchases of goods and services.

- Cash and payable bills contributions to creditors

- Wages cash incentives and other payments to employee, Unless they can be directly linked to finance or investment, cash transfers or tax refunds are not appropriate.

Additional Information

Cash flow from Financing Activities : Financing operations are those that result in a change in the enterprise's capital and borrowings. The following are some examples of cash flow generated through financing activities.

- Receipts in cash from the sale of shares or other similar securities

- Cash revenues from the sale of debentures, loans, bonds, and other short- and long-term debt.

- Payment in cash for the purchase of equity shares

- Repayment of the R Borrowed in cash, including the redemption of debentures, bonds, and preference shares, among other things.

- Dividends on both preference and equity shares are paid in cash. Interest on debentures and loans is paid in cash.

-

Question 30

5 / -1

Mithas Limited was formed with share capital of Rs. 50,00,000 divided into 50,000 shares of Rs. 100 each. 9,000 shares were issued to the vendor as fully paid for purchase consideration of a furniture acquired. 30,000 shares were allotted in payment of cash on which Rs. 70 per share was called and paid. State the amount of subscribed capital:

Solution

The correct answer is Rs.30,00,000.

Key Points

Subscribed Capital :

- The subscribed capital, also known as the subscribed share, is the amount of money that investors agree to contribute when the shares are issued.

- When a corporation issues new stock to raise funds, it must find investors ready to buy the stock.

- However, subscribed share capital refers to the shares that investors are waiting to purchase; the company does not need to attract new investors to purchase these shares.

Important Points

| Date | Particulars | L.F. | Dr. | Cr. |

| 1. | Furniture A/c Dr. (9,000 x 100) | | 9,00,000 | |

| | To Mithas Ltd A/c | | | 9,00,000 |

| | (being furniture purchased) | | | |

| 2. | Mithas Ltd A/c Dr. (9,000 x 100 ) | | 9,00,000 | |

| | To Share Capital A/c | | | 9,00,000 |

| | (being share issued) | | | |

| 3. | Bank A/c Dr. ( 30,000 x 70) | | 21,00,000 | |

| | To Share Allotment A/c | | | 21,00,000 |

| | (being issue of allotment shares) | | | |

| 4. | Share Allotment A/c Dr. (30,000 x 70) | | 21,00,000 | |

| | To Share Capital A/c | | | 21,00,000 |

| | (being shares allotted for application) | | | |

Therefore, Subscribed Share capital = 21,00,000 + 9,00,000 = ₹ 30,00,000.

-

Question 31

5 / -1

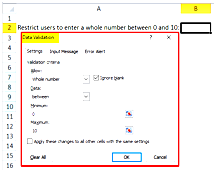

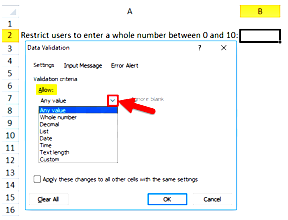

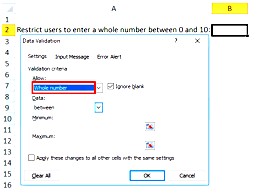

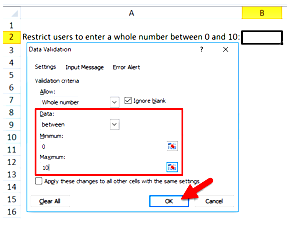

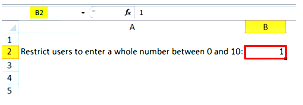

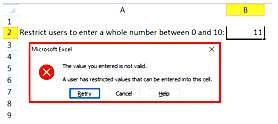

Which tool is used to control what a user can enter in a cell of excel sheet?

Solution

The correct answer is Data Validation.

- Data validation is a feature, which is used to control what a user can enter in a cell of an excel sheet. We can create a customized message which will appear if the user inserts any incorrect value or an incorrect format.

- Data validation is used in Excel to make sure that users enter certain values into a cell.

- Data Validation is located in Data tools.

Steps to Apply Data Validation:

- We can restrict a user to enter a whole number between 0 and 10. Select B2 Cell.

- A data validation Pop-Up will open on the screen.

- On the Settings tab, Click on Allow drop-down under validation Criteria.

- Select the Whole number, then some more required options will be enabled on the screen.

- Select between from the drop-down of the Data list, Enter the Minimum and Maximum number for restriction. And click on an ok option.

-

Question 32

5 / -1

E, F and G are partners sharing profits in the ratio of 3 : 3 : 2. As per the partnership agreement, G is to get a minimum amount of Rs. 80,000 as his share of profit every year and any deficiency on this account is to be personally borne by E. The net profit for the year ended 31st March, 2020 amounted to Rs. 3,12,000. Calculate the amount of deficiency to be borne by E?

Solution

The correct answer is Rs. 2000

Key Points Guarantee of Profit to a Partner:

- A guarantee is a commitment by one or more partners, and in certain situations, the firm, to guarantee a specific amount of profit, with the burden of proof falling on the party giving the guarantee.

- In other words, it is a set amount that must be paid by the partner who receives such a guarantee.

- If the actual profit share is less than the guaranteed amount, the deficit will be borne by the firm or any of its partners, as the case may be.

- If the actual share in profits is more than the minimum guarantee amount then the firm will provide the actual profits to the partner.

Important Points Calculation of share of profits:

| Particulars | E | F | G |

| Profit sharing Ratio | 3 | 3 | 2 |

Share in Net profit

Rs. 3,12,000 in | 117000 | 117000 | 78000 |

| Less: minimum guarantee to G | | | 80000 |

| Deficiency to be borne by E | -2000 | | +2000 |

| Share of profit after minimum guarantee | 115000 | 117000 | 80000 |

Deficiency to be borne by E is Rs. 2000

-

Question 33

5 / -1

Which of the following is an example of a spreadsheet?

Solution

The correct answer is Microsoft Excel.

- Excel is Microsoft’s spreadsheet program that can be used to organize, format, and calculate data.

- You can create formulas to aggregate large amounts of data, graph and chart data, create macros, and develop pivot tables.

- Originally a neck-and-neck competitor with Lotus 1-2-3, Excel is now the spreadsheet.

Key Points

Other major software from the MS Office Package:-

- Microsoft Word

- Word is Microsoft’s word processing app.

- It includes an array of features for document creation and editing, including Spell-check, a rich text editor, and page features such as justification, paragraphs, and indentation.

- You also benefit from the what-you-see-is-what-you-get (WYSIWYG) display – as the screen displays everything in the same way as the document will look when printed.

- Microsoft PowerPoint

- Microsoft PowerPoint helps you create professional presentations.

- PowerPoint was first launched in 1990, using slides to display text, graphics, and multimedia.

- Since then, it’s added a variety of features to streamline and enhance presentations, such as transition effects, timers, and software integrations.

Additional Information

- Microsoft OneNote

- OneNote allows you to jot down your thoughts before you forget them. Then, notes can be shared with others.

- Much like a digital notebook, the application automatically saves and syncs notes.

- OneNote was introduced as a standard Office application in 2013, allowing even more users to be able to share their typed notes, drawings, and screengrabs with other online users.

- Microsoft Outlook

- Mainly used as an email application, Outlook is considered a personal information manager, coordinating your calendars, task managers, contacts, notes, journals, and browsing sessions.

- Outlook can be used as a stand-alone app, or it can be networked to connect multiple users to shared mailboxes and calendars under a single organization, for example.

- Microsoft Access

- Access is Microsoft’s database management system that provides a graphical user interface (GUI) and software development tools that allow for stored data or imported data from other databases.

- With Access, you can use data to create forms, tables, queries, and reports.

-

Question 34

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) : If debt component of the total long-term funds employed is small, outsiders feel more secure.

Reason (R) : A high Debt-Equity Ratio is considered risky as it may put the firm into difficulty in meeting its obligations to outsiders.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Key PointsAssertion (A) : If the debt component of the total long-term funds employed is small, outsiders feel more secure.

Assertion is true because the debt-to-equity ratio assesses an organization's level of debt and informs a long-term lender about the debt's level of security. A low debt equity ratio indicates greater security to outsiders.

Reason (R) : A high Debt-Equity Ratio is considered risky as it may put the firm into difficulty in meeting its obligations to outsiders.

Reason is true because a high ratio is regarded risky because it may put the company in jeopardy in fulfilling its responsibilities to outsiders. From a security point of view, a capital structure with less debt and more equity is considered favourable as it reduces the chances of bankruptcy.

Important PointsDebt Equity Ratio:-

- The link between long-term debt and equity is measured by the ratio.

- Outsiders will feel more confident if the debt component of the total long-term capital used is small.

- From a security standpoint, a capital structure with less debt and more equity is preferable. More equity is considered beneficial because it lowers the risk of bankruptcy.

- In most cases, a debt equity ratio of 2: 1 is deemed safe. However, it' varies depending on the industry.

Formula of Debt - Equity Ratio = Long term Debts / Shareholders' Funds

where,

Shareholders’ Funds (Equity) = Share capital + Reserves and Surplus + Money received against share warrants

Shareholders’ Funds (Equity) = Non-current assets + Working capital – Non-current liabilities

Share Capital = Equity share capital + Preference share capital or

Working Capital = Current Assets – Current Liabilities

-

Question 35

5 / -1

Faltu Limited invited applications for 2,00,000 shares of Rs. 10 each. These shares were issued at a premium of Rs. 11 each which was allowed at the time of allotment. All money was called and duly received except on 10,000 shares on which only application money of Rs. 3 per share was received.

The company forfeited all the shares. 7000 of forfeited shares where re-issued at Rs. 13 per share. State the amount of securities premium to be shown under the head - Reserve and Surplus.

Solution

The correct answer is Rs. 21,11,000.

Key Points

Securities Premium Reserve:

- The additional amount levied on the face value of any share when it is issued, redeemed, or forfeited is known as the Security Premium Reserve.

- According to the Companies Act of 2013, when a security premium must be documented in the balance sheet, it must be done in the Reserve & Surplus section of the Equity & Liabilities section of the balance sheet.

- This item has been added to the Reserve & Surplus category. Furthermore, reserve and excess keep track of all revenues and losses.

Important Points

| Particulars | Note no | Amount ₹ |

| EQUITY AND LIABILITIES | | |

| Shareholder's Fund | | |

| (a)Share Capital | | |

| Reserve and Surplus | | |

| (b) Securities Premium | | 21,11,000 |

Working Note:

Since the securities premium was due with the allocation money, it was not paid for the 10,000 shares that were forfeited owing to non-payment of the allotment money, but the premium was paid on the remaining shares.

Total premium = premium on non-forfeited shares + premium on forfeited shares re-issued

Securities Premium of Rs. 11 on Allotment = 190000 x 11 = 20,90,000

Premium on forfeited shares re-issued = 7000 x 3 = 21,000

Total premium = 20,90,000 + 21,000 = 21,11,000

-

Question 36

5 / -1

In case of dissolution, total creditors of the firm were Rs 40,000; creditors worth Rs 10000 were given a piece of furniture costing Rs 8000 in full and final settlement. Remaining creditors allowed a discount of 10%. What will be the amount with which cash will be credited in the realisation account for payment to creditors:

Solution

The correct answer is ₹27000

Key Points Dissolution of Partnership Firm:

- The dissolution of a partnership firm is the process of the firm's partners' relationship being dissolved or terminated.

- The term "firm dissolution" refers to the breakup of a partnership between all the business's participants.

- When a firm's partnership dissolves, the firm ceases to exist.

- This procedure includes selling all the firm's assets, as well as account, asset, and liability settlements.

Important Points

| Particulars | Amount |

| Total creditors of the firm | ₹40000 |

| Less: Creditors settled with furniture | (₹10000) |

| Remaining Creditors | ₹30000 |

| Less: discount on settlement (10%) | (₹3000) |

| Amount paid in Cash to Creditors | ₹27000 |

The amount with which cash will be credited in the realisation account for payment to creditors is ₹27000

-

Question 37

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) : 'Interest accrued but not due on borrowings' is shown under' other current liabilities'.

Reason (R) : All liabilities, of which payment is expected to be made within 12 month from the date of Balance Sheet, shall be treated as current.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

Key Points Current liabilities are a company's financial commitments that are due and payable within a year. When a corporation engages in a transaction that results in the anticipation of a future outflow of cash or other economic resources, the result is a liability. Sub items under the head of current liabilities in balance Sheet -

Important PointsIn above question,

Assertion (A) : 'Interest accrued but not due on borrowings' is shown under' other current liabilities'.

Assertion (A) is True, interest accrued, but not due on a loan should be included under the heading current liabilities because it is a company obligation that must be met within a 12-month period. Interest accrued and due refers to the amount of interest computed over the period of computation, as well as the time allotted for payment of the instalment amount. Interest accrued but not due on borrowings' is shown under "other current liabilities".

Reason (R) : All liabilities, of which payment is expected to be made within 12 months from the date of Balance Sheet, shall be treated as current.

Reason (R) is true because all liabilities that are scheduled to be paid within 12 months of the date of the Balance Sheet are considered current liabilities.

Interest on borrowings that has accrued but is not due is reported under other current liabilities under the head of current liabilities since it should be paid within a year. Thus, Both Assertion (A) and Reason (R) are true, and Reason (R) is the correct explanation of Assertion (A).

-

Question 38

5 / -1

Net Assets minus Capital Reserve is

Solution

The correct answer is Purchase Consideration.

Key PointsPurchase Consideration:

- The sum paid by the acquiring company for the acquisition of assets or a business from another company is referred to as purchase consideration.

- The difference between the purchase consideration and the value of the net assets acquired is charged to the goodwill account, if purchase consideration is greater than net assets acquired.

- The difference between the purchase consideration and the value of the net assets bought is credited to the capital reserve account, if purchase consideration is less than net assets acquired.

- Either the capital reserve or the goodwill will arrive.

Important PointsPurchase Consideration: The phrase "purchase consideration" is defined by Accounting Standard-14 as "the sum of the shares and other securities issued, as well as the payment made in the form of cash or other assets by the transferee firm to the shareholders of the transferor company." Although buy consideration refers to the entire amount made by the acquiring business to the Vendor Company's shareholders, it can be calculated in a variety of ways, as explained below:

1. The lump-sum approach: Under this method purchase consideration will be paid in lump sum as per the valuation of purchasing companies' valuation.

2. The method of net assets: Under this method purchase consideration is the difference of agreed valued of assets taken over less agreed valued of liabilities taken over.

3. Method of Net Payment : Under this method purchase consideration should be calculated by aggregating total payments made by the purchasing company.

-

Question 39

5 / -1

Second hand furniture worth Rs. 6,000 was purchased. It was repaired for Rs.600 and installed by workmen to whom Rs. 200 was paid as wages. The furniture should be capitalised for

Solution

The correct answer is Rs. 6,800.

Important PointsFurniture capitalised for

Second hand furniture price + Repair Charges + Wages = 6,000 + 600 + 200 = 6,800

-

Question 40

5 / -1

X and Y shared profits and losses in the ratio of 3:2 with effect from 1st April, 2019. They decided to share profits equally. Goodwill of the firm was valued at Rs. 60,000. The adjustment entry for Goodwill will be:

Solution

the correct answer is Dr. Y's Capital A/c and Cr. X's Capital A/c with Rs.6,000.

Key PointsWhen there is change in partnership between the partners then treatment of goodwill and reserve can be made in two methods:

When partners decides to write off goodwill and reserves completely from balance sheet-Amount of goodwill and reserves will be distributed between among partners in old ratio.

When partners decides to retain goodwill and reserves completely in balance sheet, adjusted amount of goodwill and reserves will be distributed between among partners in sacrifice ratio/gain ratio to partner’s capital account.

Important Points

Adjustment of entry for Goodwill:

| Particulars | Dr. | Cr. |

| Y's capital A/c Dr. | 6,000 | |

| To X's capital A/c | | 6,000 |

| (adjustment of goodwill made in Capitals accounts | | |

Working Note:

Calculation of Sacrifice ratio-

Sacrifice ratio= Old ratio - New ratio

X's share= 3/5 -1/2 = (6-5)/10=1/10 (here sacrifice, will be credited)

Y's Share= 2/5-1/2= (4-5)/10=-1/10 (here gaining, will be debited)

Goodwill of the firm = Rs.60,000

X's share of sacrifice =Rs 60,000 x 1/10 =Rs.6,000.

-

Question 41

5 / -1

Interest collected by an automobile company selling a car on instalment basis will be classified as________ in cash flow statement.

Solution

The correct answer is Operating activity

Key Points

Cash Flow Statement:

- A cash flow statement (CFS) is a financial statement that shows how much cash and cash equivalents are coming in and going out of a business.

- The CFS assesses a company's ability to manage its cash position, or how successfully it generates cash.

- The CFS is a useful addition to the balance sheet and income statement.

- Cash is the most important component of the CFS, and it comes from three sources: operating, investing, and financing activities.

Important Points Operating Activities:

- These are a company's principal or primary activity.

- The major activities of a business firm's buying and selling of goods and services are referred to as operating activities.

- Manufacturing, distribution, selling, and marketing are examples of these operations.

- Even though these operations do not require investing or financing, they produce a significant cash flow in the organisation and aid in determining the firm's profitability.

In this case, Interest collected by an automobile company selling a car on instalment basis is classified as operating activities. Selling a car on instalment is a routine activity which creates a major revenue for the company. Hence, it is classified as Operating Activities.

-

Question 42

5 / -1

Y's profit after tax was Rs. 1,00,000. Its current assets were Rs. 4,00,000 , current liabilities Rs. 2,00,000, fixed assets Rs. 6,00,000 and 10% long term debt Rs. 4,00,000. The tax was Rs. 25,000. Return on investment will be:

Solution

The correct answer is 20.63%

Key Points

Return on investment:

- Return on Investment (ROI) calculates the profit or loss based on the amount of money invested.

- ROI (Return on Investment) is a term used to describe an organization's profit or the earnings of various assets.

- It is usually stated as a percentage. Simply said, Return on Investments calculates how much you get back for the money you put in.

- Return on Investment can be calculated in a variety of ways to determine a company's profitability.

- A corporation can use it to estimate inventory investments, pricing policies, capital equipment investments, and so on.

Formula: ROI = (Net Profit before interest, Tax & Dividend/ Capital Employed) x 100

Important Points Calculation of Net Profit before interest, Tax & Dividend

Profit after tax = ₹ 1,00,000 (Given)

Tax = ₹ 25000 (Given)

Profit after tax = Profit before tax - Tax

Profit before tax = Profit after tax + Tax = 1,00,000 + 25,000 = ₹1,25,000

10% long term debt = Rs. 4,00,000 (Given)

Interest on Long term Debt = 4,00,000 x 10% = ₹40000

Profit before tax and Interest = Profit before tax + Interest = 1,25,000 + 40,000 = 1,65,000

Calculation of Capital Employed

Capital Employed = Fixed Assets+ Current Assets – Current Liabilities

Capital Employed = ₹6,00,000 + ₹4,00,000 – ₹2,00,000 = ₹8,00,000

Calculation of Return on Investment

ROI = (Net Profit before interest, Tax & Dividend/ Capital Employed) x 100

ROI = (1,65,000/ 8,00,000) x 100

ROI =20.625% = 20.63% (Approx)

-

Question 43

5 / -1

To discover how many cells in a range contain values that meet a single criterion, use the _______ function.

Solution

The correct answer is COUNTIF.

Key Points

- COUNTIF is an Excel function to count the number of cells which meet up with the given single criteria.

- It can be used to count cells containing data like numbers, dates, and characters matching the given specific criteria.

- The logical operator supported by the COUNTIF function is ‘>’.

-

Question 44

5 / -1

Capital employed by a firm is Rs. 5,00,000. Its average profit is Rs. 60,000. The normal rate of return in similar type of business is 10%. The amount of super profits is:

Solution

The correct answer is ₹10000

Key Points Super Profit:

- The difference between the expected future profit and the usual profit is known as super profit.

- It is a method of calculating the additional earnings made by a company.

- The value of super profits is multiplied by a particular number (that number being the number of years since the acquisition).

Super Profit = Average estimated profit – Normal Profit

Important Points Calculation of Normal Profit

Capital employed by a firm = Rs. 5,00,000 (Given)

Normal Profit = Capital Employed x (Normal Rate of Return/100)

Normal Profit = 5,00,000 x (10/100) = ₹ 50,000

Calculation of Super Profit

Super Profit = Average estimated profit – Normal Profit

Super Profit = 60000 – 50000

Super Profit = ₹ 10,000

-

Question 45

5 / -1

Match Column I with Column II

| | Column I | | Column II |

| i. | Incoming partner brings his share of goodwill | A. | No Entry |

| ii. | Incoming partner does not bring his share of goodwill | B. | Premium for Goodwill A/c Dr.

Incoming Partner’s Capital A/c Dr.

To Sacrificing Partners Capital A/c |

| iii. | Incoming partner pays his share of goodwill privately | C. | Premium for Goodwill A/c Dr.

To Sacrificing Partners Capital A/c |

| iv. | Incoming partner brings only a part of his share of goodwill | D. | Incoming Partner’s Capital A/c Dr.

To Sacrificing Partners Capital A/c |

Solution

The correct answer is i- C, ii-D, iii-A, iv-B.

| | Column I | | Column II |

| i. | Incoming partner brings his share of goodwill | C. | Premium for Goodwill A/c Dr.

To Sacrificing Partners Capital A/c |

| ii. | Incoming partner does not bring his share of goodwill | D. | Incoming Partner’s Capital A/c Dr.

To Sacrificing Partners Capital A/c |

| iii. | Incoming partner pays his share of goodwill privately | A. | No entry |

| iv. | Incoming partner brings only a part of his share of goodwill | B. | Premium for Goodwill A/c Dr.

Incoming Partner’s Capital A/c Dr.

To Sacrificing Partners Capital A/c |

Key Points Goodwill brought in by new partner:

- Since no consideration in money or money's worth is paid for a partner's admission, goodwill cannot be raised in the firm's books.

- If an incoming partner delivers a premium above and beyond his capital contribution at the time of his admission, such premium should be shared among existing partners.

- When a new partner is accepted to a firm, the former partner usually makes a sacrifice in the future in the form of a lower profit sharing ratio.

- As a result, on the basis of profit sacrificing ratio, the premium for goodwill brought in by the new partner will be provided to the existing partners.

Important PointsI. When the new partner brings goodwill in cash the following entries are passed :-

| | Particulars | L.F | Debit | Credit |

| i. | Bank A/c Dr. | | | |

| | To Premium for Goodwill A/c | | | |

| | ( Amount brought by new partner for his share of Goodwill) | | | |

| ii. | Goodwill A/c Dr. | | | |

| | To Sacrificing Partner's Capital A/c | | | |

| | ((Goodwill brought by new partners distributed

among the existing partners in their sacrificing

ratio) | | | |

II. When the new partner does not bring his share of goodwill in cash

| | Particulars | L.F | Dr. | Cr. |

| i. | Incoming Partner's Capital A/c Dr. | | | |

| | To Sacrificing Partner's Capital A/c ( Individually) | | | |

| | (Account of goodwill not brought by new partner) | | | |

III. When the new partner brings only part of his share of goodwill:

| | Particulars | L.F | Dr. | Cr. |

| i. | Bank A/c Dr. | | | |

| | To Premium for Goodwill A/c | | | |

| | ( Premium for goodwill brought by the new partner) | | | |

| ii. | Premium for Goodwill A/c Dr. | | | |

| | Incoming Partner's Capital A/c | | | |

| | To Sacrificing partner's capital A/c | | | |

| | ( Goodwill credited in sacrificing ratio) | | | |

IV. When Incoming partner pays his share of goodwill privately

No entry is Passed

-

Question 46

5 / -1

Out of total face value, liability of a shareholder is limited to _______ value of the share allotted to him.

Solution

The correct answer is Nominal.

Key PointsShares-a part or portion of a larger amount which is divided among a number of people, or to which a number of people contribute. The person who hold shares are called shareholders.The shareholders are owners of the company.

A company, being an artificial person, cannot generate its own capital, which has necessarily to be collected from several persons. These persons are known as shareholders, and the amount contributed by them is called share capital.

Important Points If Companies Limited by Shares: The liability of its members is restricted in this scenario to the nominal value of the shares they own. If a member has paid the whole price of the shares, he has no accountability for the company's debts. He is not required to pay a single penny from his personal assets. If there is any liability, it can be enforced both during the company's existence and throughout the winding up process.

Thus, Out of total face value, liability of a shareholder is limited to Nominal value of the share allotted to him.

Additional InformationCompanies Restricted by Guarantee: In this arrangement, the members' liability is limited to the amount they agree to contribute if the business is liquidated. As a result, the members' culpability will emerge only if the company is wound up.

Unlimited Companies: An unlimited company is one in which the responsibility of its members is unrestricted. When the company's assets are insufficient to pay off its debts, private property owned by its members can be used. In other words, creditors have the right to collect their debts from the organization's members.

-

Question 47

5 / -1

Which of the following is the main difference between Primary Key and Unique Key

Solution

The correct option is Primary Key does not accept NULL Values whereas Unique Key does

CONCEPT:

A column or attribute of a table is said to be a primary key of the table if it can uniquely identify each tuple in the table.

In a table, there can only be one primary key and it can not contain any duplicate and NULL values.

The primary key is selected from a set of candidate keys of a relation.

Whereas

Unique key constraints also identify a tuple uniquely in a table. Unlike primary key, a table can have more than one unique key.

A Unique key can accept NULL values but cannot contain any duplicate.

Example: Consider the below Student table,

| Roll No. | Name | Email | Class |

| 1 | Aayush | aayush19@gmail.com | 12 |

| 2 | Pankaj | panka@gmail.com | 12 |

| 3 | Abhishek | --- | 11 |

In the above table Roll No. is the primary key of the relation and it cannot contain NULL values.

But Email is the Unique Key that does not contain duplicates but can have NULL values.

Additional Information

There can only be one primary key in a table but there can be multiple unique keys.

-

Question 48

5 / -1