-

Question 1

5 / -1

Calculate the amount of second & final call when Aabhar Ltd, issues Equity shares of ₹100 each at a premium of 25% payable on Application ₹50, On Allotment ₹30, On First Call ₹10.

Solution

The correct answer is Second & final call ₹35.

Key Points Issue of shares on premium:

Key Points Issue of shares on premium:

- When the shares are issued at an amount that is higher than the par value or the nominal value, such instance of issuing shares is known as shares issued at premium.

- The premium amount, or the amount in excess of the par value acquired by issuing shares, is credited to a separate account known as the securities premium account.

Important Points Amount of Premium:

Important Points Amount of Premium:

Rate of premium = 25% on face value

Rate of premium = 25% x 100 = ₹ 25

Issue price of shares = 100 + 25 = ₹ 125

Application ₹50, Allotment ₹30, On First Call ₹10.

Second & final call = Issue price - Application - Allotment - First Call = 125 - 50 - 30 - 10 = ₹ 35

Second & final call = ₹35

-

Question 2

5 / -1

Which of the following statements are true?

Solution

The correct statement is " Old furniture written off doesn’t affect cash flow."

Key Points

Cash Flow Statement:

- A cash flow statement (CFS) is a financial statement that shows how much cash and cash equivalents are coming in and going out of a business.

- The CFS assesses a company's ability to manage its cash position, or how successfully it generates cash.

- The CFS is a useful addition to the balance sheet and income statement.

- Cash is the most important component of the CFS, and it comes from three sources: operating, investing, and financing activities.

Important Points Statement 1: Old furniture written off doesn’t affect cash flow.

- This statement is true as writing furniture off in business is claiming that it no longer serves a purpose and has no future value. It denotes that the value of the asset is now zero. Hence, it does not affect cash flow.

Statement 2: Cash flow statement is a substitute for cash account.

- This statement is not true as the purpose of a cash flow statement is to ascertain the sources of cash and where the cash has been utilised categorising the type of transaction while the purpose of a cash account is to record daily cash transactions and to ascertain the end balance of cash. Hence, Cash flow statement is not a substitute for cash account.

Statement 3: Appropriation of retained earnings is shown in cash flow statement.

- This statement is false as retained earnings do not appear on the cash-flow statement, which lists all changes in cash and cash equivalents for the period, because it has no connection to net-cash flow. As there is no actual cash outflow.

Statement 4: Net cash flow during a period can never be negative:

- This statement is not true as net cash flow during a period can be negative. Negative cash flow occurs when a business spends more than it makes within a given period. Low profits, overinvesting, unexpected financial expenses can lead to negative cash flow.

-

Question 3

5 / -1

A company has an operating cycle of 14 months. It has trade payables amounting to ₹30,00,000 out of which ₹3,00,000 have a maturity period of 13 months. How would this information be presented in the balance sheet?

Solution

The correct answer is ₹3,00,000 as Current liabilities.

Key PointsThus, the company have an operating cycle of 14 months, and the trade payables have a maturity period of 13 months which is less than a operating cycle of company. So, it will be recorded as Current Liabilities in balance sheet of company.

Important PointsOperating Cycle:

- The amount of days it takes a corporation to convert its inventories to cash is referred to as the operating cycle. It is calculated by adding the time spent selling inventories (days inventories outstanding) to the time spent recovering cash from trade receivables (days sales outstanding).

- The operating cycle length of a corporation is a measure of its liquidity and asset usage. Companies with longer operational cycles, on average, must demand a larger return on sales to offset the higher opportunity cost of cash held in inventories and receivables.

- The process of producing/purchasing inventory, selling them, recovering cash from consumers, utilising that revenue to acquire raw materials to generate new inventories, and so on is called the operating cycle since it is repeated as long as the company is in existence.

- Operating Cycle = DIO + DSO

Day inventories outstanding (DIO) and days sales outstanding (DSO) are acronyms for days inventories outstanding and days sales outstanding, respectively. The average number of days a company's inventory remains unsold is known as days inventories outstanding. Days sales outstanding, on the other hand, refers to the average time it takes for receivables to be paid in cash.

Operating cycle minus days payable outstanding (DPO) equals net operating cycle (also known as cash conversion cycle).

-

Question 4

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R)

Assertion (A) : Interest on Loan by Partner is shown in Profit & Loss A/c.

Reason (R) : Interest on Loan by Partner is given only when Partnership Firm earns the profits.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is (A) is correct, but (R) is wrong.

Key Points Profit and loss account

- The profit and loss account is a recurring statement that illustrates the net result of business operations over a given time period.

- This is where you keep track of all of your spending and earnings for the reporting period.

Important PointsAssertion (A) : Interest on Loan by partner is shown in Profit & Loss A/c.

- The Assertion (A) is true as Interest on a loan from a partner to the firm is treated as an expense and deducted from the profit and loss account.

Reason (R) : Interest on Loan by partner is given only when Partnership Firm earns the profits.

- The Reason (R) is not true as Interest on loan by partner is a charge against profit. It is charged irrespective of profits. It is charges even firm makes profit or loss.

-

Question 5

5 / -1

Your worksheet has the value 27 in cell B3. What value is returned by the function =MOD (B3,6)?

Solution

The correct answer is option 4.

Concept:

The MOD function accepts two real number operands as parameters and returns the residual after dividing the integer component of the first argument (the dividend) by the integer part of the second argument (the divisor). The data type returned is INT (or INT8 for remainders outside the range of INT).

MOD(X,Y)

- The above-mentioned function is from Microsoft Excel.

- When two values are split, the MOD function returns the residual, which is referred to as the modulo function.

Explanation:

The mod function =MOD(27, 6) will produce the following value: 3.

The given data,

27 = B3

=MOD(B3, 6) may be written as =MOD(27, 6)

The numerator is equal to 27.

The denominator is equal to 6.

As a result, 27/6 = 4 and the remaining (27 - 24) = 3

27 - (6 × 4) = 27 - 24 = 3

Hence the correct answer is 3.

-

Question 6

5 / -1

What will be the Quick Ratio if Current Assets = ₹72,500; Inventories = ₹12,500; Prepaid Expenses = ₹15,000; Building = ₹50,000; Working Capital = ₹50,000.

Solution

The correct answer is 2 : 1

Key Points Quick Ratio or Acid Test Ratio:

The quick ratio, also known as the acid test ratio, is used to establish whether a firm or a business has sufficient liquid assets that can be converted into cash quickly enough to pay short-term obligations.

Formula: Quick Ratio = Quick Assets / Current Liabilities

Where, Quick Assets = Current Assets – Inventory – Prepaid expenses

Important PointsCalculation of Quick Assets

Current Assets = ₹72,500; (Given)

Inventories = ₹12,500; (Given)

Prepaid Expenses = ₹15,000; (Given)

Quick Assets = Current Assets – Inventory – Prepaid expenses

Quick Assets = 72,500 – 12,500 – 15,000

Quick Assets = 45000

Calculation of Current Liabilities

Current Assets = ₹72,500; (Given)

Working Capital = ₹50,000 (Given)

Working Capital = Current Assets - Current Liabilities

Current Assets = Current Assets - Working Capital

Current Assets = 72,500 - 50,000

Current Assets = 22,500

Calculation of Quick Ratio

Quick Ratio = Quick Assets / Current Liabilities

Quick Ratio = 45000 / 22500

Quick Ratio = 2 : 1

-

Question 7

5 / -1

Pawan and Vikas are partners in a firm sharing profits and losses in the ratio of 4 ∶ 3.

| Balance Sheet (Extract) |

| Liabilities | ₹ | Assets | ₹ |

| | | Inventory | 2,00,000 |

If the value of Inventory reflected in the above balance sheet is overvalued by 25%, find out the value of inventory to be shown in the new Balance Sheet:

Solution

The correct answer is ₹1,60,000

Key Points Inventory:

- Inventory refers to both the raw materials needed in the manufacturing of commodities and the finished goods that will be sold on the market.

- There are mainly three types of inventory: raw materials, work-in-progress goods, and finished goods.

- Inventory is categorised as a part of the current assets in the balance sheet of a company.

Important Points Inventory as per balance sheet = 2,00,000

This inventory is overvalued, which means the actual inventory is lower than what is shown in the balance sheet.

Revalued Inventory = 2,00,000 x 100 / 125

Revalued Inventory = 1,60,000

-

Question 8

5 / -1

A special value _______ is used to represent values that are unknown or non-applicable to certain attributes.

Solution

The correct answer is an option (2)

Concept:-

A special value "Null" is used to represent values that are unknown or non-applicable to certain attributes.

Key Points

- The term NULL is used to signify a missing value in SQL. In a table, a NULL value is a value in a field that seems to be empty.

- Within the scope of the fundamental relational model, each value in a tuple is an indivisible value, implying that it is not divisible into components.

- The NOT NULL constraint prevents a column from accepting NULL values, meaning we can't insert or update a record without giving it a value.

- This rule requires that the RDBMS support a distinct NULL placeholder, regardless of datatype.

For example:-

Table Name: Student

| Roll No | Name | Marks |

| 111 | Ajay | 70 |

| 222 | Vijay | 80 |

| 333 | Sanjay | |

| 444 | Malay | 76 |

In the given table the Marks contain one null value with respect to the name 'Sanjay', as it's not applicable for Sanjay, due to any reason.

-

Question 9

5 / -1

Match the items given in Column I with the headings/subheadings (Balance sheet) as defined in Schedule III of Companies Act 2013 in Column II.

| | Column I | | Column II |

| (a) | Trademark | (i) | Inventories |

| (b) | Securities Premium Reserve | (ii) | Tangible Fixed Assets |

| (c) | Bank Overdraft | (iii) | Intangible Fixed Assets |

| (d) | Motor Vehicles | (iv) | Short Term Borrowings |

| (e) | Stores and Spare Parts | (v) | Reserve and Surplus |

Solution

The correct answer is a - (iii), b - (v), c - (iv), d - (ii) and e - (i).

Key Points

| | Column I | | Column II |

| (a) | Trademark | (iii) | Intangible Fixed Assets |

| (b) | Securities Premium Reserve | (v) | Reserve and Surplus |

| (c) | Bank Overdraft | (iv) | Short Term Borrowings |

| (d) | Motor Vehicles | (ii) | Tangible Fixed Assets |

| (e) | Stores and Spares Parts | (i) | Inventories |

Important PointsIntangible Fixed Assets :A non-physical asset is referred to as an intangible asset. Intangible assets include goodwill, brand awareness, and intellectual property like as patents, trademarks, and copyrights. Tangible assets, such as land, vehicles, equipment, and inventories, compete with intangible assets.

Reserve and Surplus: Reserves and surplus are the total amount of retained earnings reported as a component of the Shareholders Equity and are set aside by the company for specified objectives such as purchasing fixed assets, paying legal settlements, repaying debts, or paying dividends, among others.

Short Term Borrowings :Short-term borrowing refers to loans taken out for a relatively short length of time in order to meet a brief business necessity. For example, a one-year short-term loan is used to pay off debtors. Small firms, particularly start-ups, might use this sort of borrowing to meet their short-term demands. These loans aren't just for corporate purposes. In fact, these can be used by individuals to meet their cash needs.

Tangible Fixed Assets :Tangible assets are assets that have a high value and are physically available. It indicates that any tangible asset with a long-term value that can be touched and felt qualifies as a tangible asset. These fixed assets assist firms in the manufacture and production of goods and products in order to increase revenue. Furthermore, businesses can use these assets as loan collateral.

Inventories: The term inventory refers to both the raw materials utilised in production and the finished goods that are ready to sell. Inventory is one of a company's most valuable assets because inventory turnover is one of the key sources of revenue production and, as a result, earnings for the company's shareholders. Raw materials, work-in-progress, and finished goods are the three forms of inventory. On a company's balance sheet, it's classified as a current asset.

-

Question 10

5 / -1

Nisha and Aisha were partners in a firm. Their Balance Sheet showed Stock at ₹1,20,000; Furniture at ₹80,000 and Sundry Creditors at ₹40,000. Harshita was admitted as a new partner. Stock was revalued at ₹1,30,000, Furniture ₹70,000 and Creditors of ₹20,000 are not likely to be claimed. Share of Aisha in profit on revaluation will be:

Solution

The correct answer is ₹10000

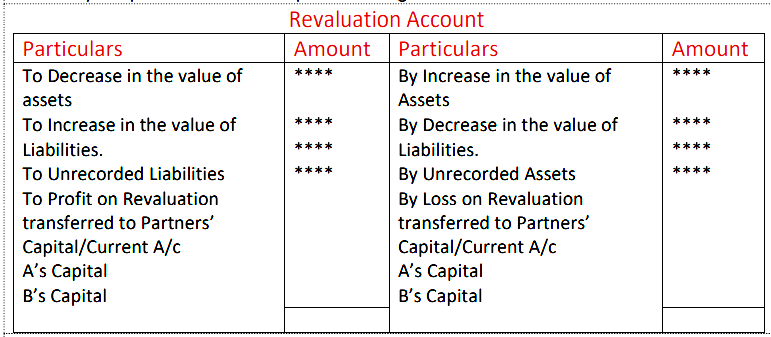

Key Points Revaluation account:

The revaluation account is a nominal account used to distribute and transfer profits and losses resulting from increases and decreases in the book value of assets and liabilities as a result of changes in profit sharing ratio, admission of a partner, retirement of a partner, and death of a partner.

Important Points Revaluation account

Dr. Cr.

| Particulars | Amount | Particulars | Amount |

| To furniture | 10000 | By stock | 10000 |

| | | By Creditors | 20000 |

| To profit on Revaluation: | | | |

| Nisha: 10000 | 20000 | | |

| Aisha: 10000 | | |

| Total | 30000 | Total | 30000 |

Share of Aisha in profit on revaluation will be ₹10,000

Working Notes:

Increase in Stock = 130000 - 120000 = 10000

Decrease in furniture = 80000 - 70000 = 10000

-

Question 11

5 / -1

The degree of the relation describes the number of __________ in relation.

Solution

The correct option is answer (3)

Concept:-

The amount of qualities (columns) in a relation (table) determines its degree. A property or feature of an entity is referred to as an attribute.Key Points

- The number of tuples/ rows in a relation is called the cardinality of the relation.

- Attributes in an Entity-relationship model are represented by an ellipse shape.

- A degree of relationship in a database management system (DBMS) is the number of entity types that are associated in a relationship.

Additional InformationTuples:- A tuple is a single record in a relational database (one row). In a typical database, rows and columns are represented by multiples and fields. A tuple can be thought of as a map with fields that can be added or removed.

Additional InformationTuples:- A tuple is a single record in a relational database (one row). In a typical database, rows and columns are represented by multiples and fields. A tuple can be thought of as a map with fields that can be added or removed.

Keys:- A key is a single column (or attribute) or a set of columns that can be used to identify rows (or tuples) in a table in a unique way.

Relationship:- A relationship type is a sort of connection between two separate (or the same) entity types. In the database, there are three sorts of relations.

- one-to-one

- one-to-mamy

- many-to-many.

-

Question 12

5 / -1

CNB Ltd, issued a prospectus inviting applications for 20,000 shares. Applications were received for 30,000 shares and pro-rata allotment was made to the applicants of 25,000 shares. If Seema has been applied for 500 shares, how much shares she have been allotted?

Solution

The correct answer is 400.

Key Points

Pro-rata allotment of shares :

- Pro-rata allotment refers to the distribution of shares in proportion to the number of shares requested.

- When a corporation makes a pro-rata allocation, it first applies the surplus funds received at the time of application to the allotment, then to the calls.

- After adjusting the amount for allotment and calls to the applicants, any surplus is refunded.

- The procedure for allotment is advertised in the major newspapers by the corporation.

For Example:The public is offered 10,000 shares by XYZ Ltd. The issuance was oversubscribed by a large margin. It receives 20000 share applications. When a corporation decides to allot shares on a pro-rata basis, it must allot 10,000 shares to each of the 20000 applicants. As a result, the ratio will be 20000:10000, which is 2:1. As a result, an application seeking two shares will only receive one. This is a pro rata distribution.

Important Points

Number of Shares allotted by Seema

= Total number of applied Shares/Total number of allotted Shares x Number of applied shares

=20,000/25,000 x 500

= 400

-

Question 13

5 / -1

If 6% Pref. share capital ₹2,00,000 were redeemed at a premium of 5%, while preparing Cash Flow Statement its effect on cash flow will be :

Solution

The correct answer is Cash used (payment) from financial activities ₹2,10,000.Key Points

Cash Flow Statement:

- A cash flow statement (CFS) is a financial statement that shows how much cash and cash equivalents are coming in and going out of a business.

- The CFS assesses a company's ability to manage its cash position, or how successfully it generates cash.

- The CFS is a useful addition to the balance sheet and income statement.

- Cash is the most important component of the CFS, and it comes from three sources: operating, investing, and financing activities.

Important PointsRedemption of Preference Share: Preference shareholders are paid back the amount they invested in the shares when their preference shares are redeemed. It leads to an outflow of cash. This outflow would be shown in the Cash Flow Statement as Rs 2,10,000 in financing activities.

Redemption of Preference Share Capital = Rs. 2,00,000

Add: Premium on Redemption = 5% on redemption = 5/100 x 2,00,000 = 10,000

Hence, the cash used(payment) from financial activities = 2,00,00 + 10,000 = 2,10,000

-

Question 14

5 / -1

Mehar and Priya are partners sharing profit in the ratio 3 ∶ 1. On 31st March 2021, firms net profit is ₹4,00,000. The partnership deed provided interest on capital to Mehar and Priya ₹40,000 and ₹30,000 respectively. Mehar is also entitled to commission @10% on net divisible profits, before charging such commission. What will be the Commission payable to Mehar?

Solution

The correct answer is 33,000.

Important Points

| Particulars | Amount |

| Net Profit | 4,00,000 |

| Less: Interest on Mehar's Capital | (40,000) |

| Less: Interest on Priya's Capital | (30,000) |

| | 3,30,000 |

| Less: Commission to Mehar | 33,000* |

| Net Divisible Profit | 2,97,000 |

Working Note:

* Mehar's Commission @ 10% on net divisible profits before charging such commission

Net divisible profit before charging such commission = 3,30,000

Hence, Commission to Mehar = 10/100 x 3,30,000 = 33,000

-

Question 15

5 / -1

What will be the Purchased Consideration if Sundry Assets = ₹1,20,000, Sundry Creditors = ₹30,000 Goodwill = ₹20,000

Solution

The correct answer is ₹1,10,000

Key Points Purchase Consideration:

In case of a company taking over another company, purchase consideration is the agreed amount which transferee company (Purchasing company) pays to the transferor company (Vendor company) in exchange for the ownership of the transferor company. It may be in form of cash, shares or any other assets as agreed between both the companies.

Methods of determination of Purchase Consideration:

- Lump Sum Method

- Net Worth or Net Assets Method

- Net Payment Method

- Intrinsic Value Method (Shares Exchange Method).

Important Points Calculation of Purchase Consideration

Purchase Consideration = Assets taken over - liabilities taken over

Purchase Consideration = Sundry Assets + Goodwill - Sundry Creditors

Purchase Consideration = 1,20,000 + 30,000 - 20,000

Purchase Consideration = 1,10,000

-

Question 16

5 / -1

Chetan and Amit are partners in the ratio of 3 ∶ 2. Their fixed Capital were ₹2,00,000 and ₹3,00,000 respectively. After the closing of accounts for the year it was observed that the Salary to Amit was given wrongly ₹50,000 during the year as there was not any agreement regarding it. By what amount will Chetan's account be affected if partners decide to pass an adjustment entry for the same considering partners capital accounts are fixed?

Solution

The correct answer is Chetan's Current A/c will be credited by ₹30,000.

Important Points

| Particulars | Chetan's Current A/c | Amit's Current A/c | Firm | Firm |

| | Dr. | Cr. | Dr. | Cr. | Dr. | Cr. |

| Salary wrongly Credited to Amit's account Rs. 50,000 | | | 50,000 | | | 50,000 |

| Profit of 50000 shared in 3:2 | | 30,000 | | 20,000 | 50,000 | |

| Net effect | | 30000 (Cr) | 30000 (Dr) | | | |

Adjustment Journal Entry:

| Particulars | Amount Dr. | Amount Cr |

| Amit's Current A/c Dr | 30000 | |

| To Chetan's Current A/c | | 30000 |

| (Salary wrongly provided to Amit adjusted) | | |

-

Question 17

5 / -1

Trendy Ltd took over business of Oxylight Ltd and paid for it by

(i) Issue of 2,000 10% Preference Shares of ₹100 each at a premium of 10%

(ii) Equity Shares of ₹1,00,000 at a par and

(iii) a cheque of ₹1,00,000.

What was the total agreed purchase consideration payable to Oxylight Ltd.

Solution

The correct answer is ₹4,20,000.

Key PointsTotal agreed purchase consideration payable to Oxylight Ltd. by Trendy Ltd. = 4,20,000

(i) Issue of 2,000 10% Preference Shares of ₹100 each at a premium of 10%

= 2,000 x 100 = 2,00,000

Premium is 10% which means 10/100 x 100 = 10

2,000 x 10 = 20,000

(ii) Equity Shares of ₹1,00,000 at a par, which means

= Equity Shares issued of Rs. 1,00,000

(iii) A cheque of ₹1,00,000

Important PointsJournal Entry will be:

| Particulars | Dr. | Cr. |

| Oxylight Ltd. A/c Dr. | 4,20,000 | |

| To Preference Share Capital a/c | | 2,00,000 |

| To Securities Premium Reserve A/c | | 20,000 |

| To Equity Share Capital A/c | | 1,00,000 |

| To Bank A/c | | 1,00,000 |

| (payment made by Trendy Ltd. to Oxylight Ltd.) | | |

Additional InformationPurchase Consideration : The payment made by the transferee company to the transferor company for the business taken over is referred to as Purchase Consideration. It covers all sorts of payments, including those made in the form of shares, equities, bonds, or cash.

According to Accounting Standard 14,

- The total number of shares and other securities issued, as well as the payment made in cash or other assets by the transferee firm to the transferor company's shareholders."

- The purchase price does not include payments to debenture holders or any other outside liabilities that Transferee Company assumes and discharges.

- It is determined by the fair market value of the securities and assets. The fair value of securities is determined by the authorities, while the fair value of assets is determined by their book value and, if available, market value.

-

Question 18

5 / -1

At the time of admission of a partner in the Partnership Firm, recording of an unrecorded Liability will lead to:

Solution

The correct answer is Loss to the existing partners in their old profit sharing ratio.

Key Points

- A reassessment of the liabilities is also done so that these are brought in the books at their correct values. At times there may also be some unrecorded assets and liabilities of the firm. These also have to be brought into the books of the firm.

- For this purpose the firm has to prepare the Revaluation Account. The gain or loss on revaluation of each asset and liability is transferred to this account and finally its balance is transferred to the capital accounts of the old partners in their old profit sharing ratio.

- In other words, the revaluation account is credited with increase in the value of each asset and decrease in its liabilities because it is a gain and is debited with decrease in the value of assets and increase in its liabilities is debited to revaluation account because it is a loss.

- Similarly unrecorded assets are credited and unrecorded liabilities are debited to the revaluation account. If the revaluation account finally shows a credit balance then it indicates net gain and if there is a debit balance then it indicates net loss. Which will be transferred to the capital accounts of the old partners in old ratio.

For an unrecorded liability, the journal entry will be

Revaluation A/c Dr.

To Liability A/c (Loss)

Important PointsAdmission of Partner:: A new partner may be admitted when the firm needs additional capital or managerial help. According to the provisions of Partnership Act 1932 unless it is otherwise provided in the partnership deed a new partner can be admitted only when the existing partners unanimously agree for it.

Unrecorded Liabilities: These are the liabilities which have not been recorded in the books of account, these are the loss for the companies.

-

Question 19

5 / -1

Akhil and Ravi are partners sharing profits and losses in the ratio of 7:3 with capitals of Rs. 8,00,000 and Rs. 6,00,000 respectively. According to partnership deed, interest on capital is to be provided @ 8% p.a profit for the year is Rs. 80,000. Choose the correct option:

Solution

The correct answer is Akhil will be credited by Rs. 45,715 and B will be credited by Rs. 34,285

Key PointsInterest on capital - No partner is entitled to claim any interest on the amount of capital contributed by him to the firm as a matter of right. However, interest can be allowed when it is expressly agreed to by the partners. Thus, no interest on capital is payable if the partnership deed is silent on the issue.

Important PointsCalculation of Interest on capital of Partner's Capital -

Interest on capital= Capital of Partner x rate of interest/100

Akhil's Capital - Rs.8,00,000 x 8/100 = Rs.64,000

Ravi's Capital - Rs.6,00,000 x 8/100 = Rs.48,000

Thus, interest of Capital will be credited in Akhil's Capital A/c by Rs.64,000 & Ravi's Capital A/c by Rs.48,000.

Since available profit is only 80,000 which is less than total amount of interest, the interest is distributed only till the available profit in the ratio of interest.

Interest on capital = Akhil : Ravi = 64000: 48000 = 4 : 3

Akhil = 80000 x 4/7 = 45715

Ravi = 80000 x 3/7 = 34285

Journal Entry for recording of Interest on Capital

| Particulars | Amount Dr. | Amount Cr. |

| Interest on Capital A/c | 80000 | |

| To Akhil's Capital A/c | | 45715 |

| To Ravi's Capital A/c | | 34285 |

Additional Information

Recording of Interest on Capital in P&L Appropriation A/c

Profit & Loss Appropriation A/c

Dr. Cr.

| Particulars | Amount | Particulars | Amount |

By Int. on Capital A/c Akhil 45715 Ravi 34285 | 80,000 | By Net Profit A/c | 80,000 |

-

Question 20

5 / -1

Rakesh and Sachin are partners sharing profits in the ratio of 4 ∶ 1. Vikas was admitted for 1/4 share of which 3/4 was gifted by Rakesh. The remaining was contributed by Sachin. Goodwill of the firm is valued at ₹40,000. How much amount for goodwill will be credited to Sachins Capital account?

Solution

The correct answer is ₹2,500.

Important PointsAt the time of admission of new partner into firm, the goodwill of the firm is to be distributed in sacrificing ratio of old partners.

Sacrifice Ratio = Old Ratio - New Ratio

Vikas's total share = 1/4

Rakesh's Sacrifice = 1/4 x 3/4 = 3/16

Sachin's Sacrifice = Total share of Vikas - Rakesh's sacrifice

=1/4 - 3/16 = 1/16

Sacrificing Ratio of Rakesh and Sachin = 3:1

Amount of goodwill Vikas b= 40,000 x 1/4 = 10,000.

The amount for goodwill will be credited to Sachin's Capital account = 10000 x 1/4 = ₹2500

-

Question 21

5 / -1

A spreadsheet consists of rows and columns. Each row and column intersection creates a ______ into which you may enter data.

Solution

The correct answer is cell,

Key Points

- A spreadsheet consists of rows and columns. Each row and column intersection creates a cell into which you may enter data.

- In Microsoft Excel, a cell is a rectangular box that occurs at the intersection of a vertical column and a horizontal row in a worksheet. Vertical columns are numbered with alphabetic values such as A, B, C. Horizontal rows are numbered with numeric values such as 1, 2, 3.

- Each cell has its own set of coordinates or position in the worksheet such as A1, A2, or M16.

Additional Information

- function: A function is a predefined formula that performs calculations using specific values in a particular order. Excel includes many common functions that can be used to quickly find the sum, average, count, maximum value, and minimum value for a range of cells.

- formulas: A formula in Excel is used to do mathematical calculations. Formulas always start with the equal sign ( = ) typed in the cell, followed by our calculation.

- tab: There are nine tabs on the Excel Ribbon: File, Home, Insert, Page Layout, Formulas, Data, Review, View, and Help. The Home tab is the default tab when Excel is opened.

-

Question 22

5 / -1

Tara Ltd. forfeited 500 shares of ₹10 each, ₹8 called up, on which John had paid application money ₹4 and allotment money of ₹3 per share. Out of these, 300 shares were reissued to Kishor as fully paid up for ₹ 8 per share. What is the amount that has been transferred to Capital Reserve Account?

Solution

The correct answer is ₹1500.

Key Points

| Date | Particulars | L.F | Dr. | Cr. |

| (i) | Share Capital A/c Dr. (500 x 8) | | 4,000 | |

| | To Share Forfeiture A/c (500 x 7) | | | 3,500 |

| | To Calls in arrears A/c (500 x 1) | | | 500 |

| | (being share forfeited for non-payment of amount) | | | |

| (ii) | Bank A/c Dr. (300 x 8) | | 2,400 | |

| | Share Forfeiture A/c Dr. (300 x 2) | | 600 | |

| | To Share Capital A/c (300 x 10) | | | 3,000 |

| | (reissue of 300 shares as fully paid up for Rs. 8) | | | |

| (iii) | Share Forfeiture A/c Dr. | | 1500 | |

| | To Capital Reserve A/c | | | 1500 |

| | (transfer of profit to capital reserve) | | | |

Working Note:

Profit on 500 shares =Rs. 500

Hence, Profit on 300 shares = 500/500 x 300 = 300

Less: Loss on reissue of = 300 x 2 = 600

Transferred to Capital Reserve = 300

Balance in Share Forfeiture A/c of Re-issued share = 3500 x 300/500 = 2100

Capital Reserve = Balance in Share Forfeiture A/c of Re-issued share - Loss on reissue

Capital Reserve = 2100 - 600 = 1500

Important PointsShare Forfeiture : The circumstance in which the allotted shares are cancelled by the issuing firm due to non-payment of the subscription amount as requested by the issuing company from the shareholder is referred to as forfeiture of shares. If a shareholder's shares are forfeited, the shareholder's rights and interests as a shareholder are lost, and the shareholder ceases to be a member of the organisation.

-

Question 23

5 / -1

R, S and G are partners sharing profits in the ratio of 4 ∶ 2 ∶ 1. According to the partnership agreement, G is to get a minimum amount of ₹70,000 as his share of profits every year and any deficiency on this account is to be personally borne by R. The net profit for the year ended 31st March 2021 amounted to 4,20,000. Calculate the amount of deficiency to be borne by R?

Solution

The correct answer is 10,000.

Important Points

| Particulars | R | S | G |

| Profit Sharing Ratio of R, S and G | 4 | 2 | 1 |

| Net profit distributed (4,20,000 in 4:2:1) | 2,40,000 | 1,20,000 | 60,000 |

| Minimum Guarantee to G | | | 70000 |

| Amount of deficiency borne by R | -10000 | | +10000 |

| Final Share of Partners | 2,50,000 | 1,20,000 | 70000 |

Hence, R is to borne deficiency on account of G is Rs. 10,000.

-

Question 24

5 / -1

If Cash Revenue from Operations is \(\frac{1}{4}\)th of Total Revenue from Operation and Cost of Revenue from Operation is ₹2,00,000 and Gross Profit is 25% on Cost of Revenue from Operations. Gross Profit Ratio is:

Solution

The correct answer is 20%

Key Points

Gross Profit Ratio:

Gross Profit Ratio is a profitability ratio that measures the relationship between the gross profit and net sales revenue. When it is expressed as a percentage, it is also known as the Gross Profit Margin.

Formula = Gross Profit Ratio = (Gross Profit/Net Revenue of Operations) × 100

Important Points Cost of Revenue from Operation is ₹2,00,000 (Given)

Gross Profit = 25% on Cost of Revenue from Operations

Gross Profit = 25% x 200000

Gross Profit = ₹ 50,000

Net Revenue from Operation = Cost of revenue from operations + Gross Profit

Net Revenue from Operation = 2,00,000 + 50,000 = 2,50,000

Gross Profit Ratio = (Gross Profit/Net Revenue of Operations) × 100

Gross Profit Ratio = (50,000/2,50,000) × 100

Gross Profit Ratio = 20%

-

Question 25

5 / -1

Sudhir had been allotted for 400 shares by SVB Ltd on pro rata basis which had issued two shares for every three applied. He had paid application money of ₹4 per share and could not pay allotment money of ₹4 per share. First and final call of ₹2 per share was not yet made by the company. His shares were forfeited the following entry will be passed:

Equity Share Capital A/c ....Dr ₹X

To Share Forfeited A/c ₹Y

To Equity Share Allotment A/c ₹Z

Here X, Y and Z are:

Solution

The correct answer is ₹3,200; ₹2,400; ₹800 respectively.

Key Points

Forfeiture of Shares:

- The circumstance in which the allotted shares are cancelled by the issuing firm due to non-payment of the subscription amount as requested by the issuing company from the shareholder is referred to as forfeiture of shares.

- If a shareholder's shares are forfeited, the shareholder's rights and interests as a shareholder are lost, and the shareholder ceases to be a member of the organisation.

Important Points

| Particulars | Amount |

| Sudhir's Allotted Shares = | 400 |

| Sudhir's Applied Shares = 3/2 x 400 = | 600 |

| Amount paid by Sudhir on Application = 600 x 4 = | 2,400 |

| Less: Application Amount due on Sudhir's Share = 400 x 4 = | (1,600) |

| Excess amount paid by Sudhir on Application = 2,400 - 1,600= | 800 |

| Allotment Amount due on Sudhir's Share = 400 x 4 = | 1,600 |

| Less: Excess amount received on Application | (800) |

| Amount not paid by Sudhir on Allotment | 800 |

Hence, the forfeiture entry will be;

| Particulars | Dr. | Cr. |

| Equity Share Capital A/c Dr. | 3200 | |

| To Share Forfeiture A/c | | 2,400 |

| To Equity Share Allotment A/c | | 800 |

| (being share forfeited for non-payment of allotment money) | | |

-

Question 26

5 / -1

The average profit earned by the firm is ₹2,40,000. Capital invested in the business is ₹21,00,000 and the normal rate of return is 10%. What is the value of Goodwill of the firm on the basis of four times the super profit:

Solution

The correct answer is ₹ 1,20,000

Key Points Super Profit:

The excess of actual/average profit over normal or average profit is called a super profit method.

Formula: Super Profit = Average Profit – Normal Profit

Important Points The goodwill is determined by multiplying the value of super profits by a certain number (that number being the number of years of purchase).

Normal Profit = Normal Rate of Return x Capital Employed

Normal Profit = 10% x 21,00,000

Normal Profit = 2,10,000

Super Profit = Average Profit – Normal Profit

Super Profit = 2,40,000 – 2,10,000

Super Profit = ₹ 30,000

Goodwill = Super Profits x Number of Years purchased

Goodwill = 30,000 x 4

Goodwill = ₹ 1,20,000

-

Question 27

5 / -1

What does the nper argument specify in the PMT function of Excel?

Solution

The correct answer is option 3.

The PMT is used to calculate the payment of each month as EMI, for the owned loan. The PMT stands for payment.

The nper is used to define the number of payments.

Key Points

- The PMT formula is represented as: PMT(rate, nper, pv, [fv], [type])

- Where the rate, nper, pv, [fv], [type] are arguments.

- The arguments which are in square brackets are optional arguments.

- The arguments which are not in square brackets are mandatory arguments.

The arguments are described as:

- rate:- it represents the monthly rate of interest for the loan.

- nper:- it represents the number of payments of months in which the loan will be paid completely with interest.

- pv:- it represents the principal amount that is taken as a loan.

- fv:- it represents the future value or a cash balance a user wants to achieve after the last payment is made.

- type:- it represents the number 0 (zero) or 1 and indicates when payments are due. The 0 represents the due amount at the end of the period, and the 1 represents the due amount at the beginning of the period.

-

Question 28

5 / -1

Which one of the following is correct?

(i) Ideal accepted Quick Ratio is 2 ∶ 1.

(ii) A high inventory turnover ratio means inefficient use of investment in inventory and over investment in stocks.

(iii) Operating Profit = Revenue from Operations - Operating Cost.

Solution

The correct answer is Only (iii).

Key Points(i)Ideal accepted Quick Ratio is 2 ∶ 1, is incorrect statement because ideal Quick ratio is 1:1.

(ii)A high inventory turnover ratio means inefficient use of investment in inventory and overinvestment in stocks, is an incorrect statement because, Low turnover of inventory may be due to bad buying, obsolete inventory, etc., and is a danger signal. High turnover is good, but it must be carefully interpreted as it may be due to buying in small lots or selling quickly at low margin to realise cash. Thus, it throws light on utilisation of inventory of goods.

(iii) Operating Profit = Revenue from Operations - Operating Cost, is correct because formula for calculating Operating Profit is the difference of revenue from operations and operating cost.

Important PointOperating Profit Ratio: It is calculated to reveal operating margin. It may be computed directly or as a residual of operating ratio. Operating Profit Ratio = 100 – Operating Ratio Alternatively, it is calculated as under:

- Operating Profit Ratio = Operating Profit/ Revenue from Operations × 100

- Where , Operating Profit = Revenue from Operations – Operating Cost

- Operating ratio is computed to express cost of operations excluding financial charges in relation to revenue from operations’.

- It helps to analyse the performance of business and throws light on the operational efficiency of the business. It is very useful for inter-firm as well as intra-firm comparisons.

- Lower operating ratio is a very healthy sign.

Additional Information

Quick Ratio :

- It is the ratio of quick (or liquid) asset to current liabilities. It is expressed as Quick ratio = Quick Assets : Current Liabilities or Quick Assets / Current Liabilities.

- The quick assets are defined as those assets which are quickly convertible into cash. While calculating quick assets we exclude the inventories at the end and other current assets such as prepaid expenses, advance tax, etc., from the current assets. Because of exclusion of non-liquid current assets it is considered better than current ratio as a measure of liquidity position of the business.

- It is calculated to serve as a supplementary check on liquidity position of the business and is therefore, also known as ‘Acid-Test Ratio’.

- The ratio provides a measure of the capacity of the business to meet its short-term obligations without any flaw. Normally, it is advocated to be safe to have a ratio of 1:1 as unnecessarily low ratio will be very risky, and a high ratio suggests unnecessarily deployment of resources in otherwise less profitable short-term investments.

Inventory Turnover Ratio:

- It expresses the relationship between the cost of revenue from operations and average inventory.

The formula for its calculation is as follows:

Inventory Turnover Ratio = Cost of Revenue from Operations / Average Inventory - Where average inventory refers to the arithmetic average of opening and closing inventory, and the cost of revenue from operations means revenue from operations less gross profit.

- Low turnover of inventory may be due to bad buying, obsolete inventory, etc., and is a danger signal.

- High turnover is good, but it must be carefully interpreted as it may be due to buying in small lots or selling quickly at low margin to realise cash. Thus, it throws light on utilisation of inventory of goods.

-

Question 29

5 / -1

Naval Ltd offered 20,000 Equity Shares of 10 each, of these 19,000 shares were subscribed. The amount was payable as ₹3 on application, ₹4 an allotment, ₹2 on First Call and balance on Second and Final call. If a shareholder holding 1,000 shares has defaulted on Second and Final call, what is the amount of money received on Second and Final call?

Solution

The correct answer is ₹18,000.

Key PointsOver subscription - There are times when more applications for a company's shares are received than the quantity of shares available for public subscription. This is known as a 'Over Subscription' when it occurs in the case of a well-managed and financially sound company's share offering.

In this case, the directors have three options for dealing with the problem:

(1) accept certain applications in whole and reject the rest;

(2) make a pro rata allotment to everyone; or

(3) combine the above two options, which is the most usual path taken in practice.

Important PointsFace Value of shares = Rs.10

Application amount = Rs.3

Allotment amount = Rs.4

First call amount = Rs.2

Amount on Second & Final call = Rs.10 - Rs.3 - Rs.4 - Rs.2= Rs.1

No. of Shares subscribed by company= 19,000 Shares

Calls in Arrears on shares = 1000 Shares

No. shares on Second & Final call received = 19,000 -1,000 =18,000 Shares

Amount of money received on Second and Final call = Rs.1 x 18,000 = Rs.18,000.

-

Question 30

5 / -1

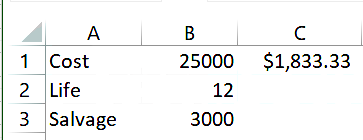

What will be the sequence of cell addresses passed as arguments in the SLN formula at cell C1 in the sheet?

Solution

The correct answer is: (B1,B3,B2)

Key Points

- The SLN function is used to calculate the depreciation of a product on the basis of a straight line for one period.

- The syntax of the SLN function is like this: =SLN(cost, salvage, life)

- The straight line is the easiest way to calculate the depreciation of a fixed asset.

- The formula used in a straight-line method to calculate SLN is like this: \(SLN=\frac{cost-salvage}{life}\)

The arguments are described as:

- cost: The principal cost of an asset at the point of purchase.

- salvage: The value of an asset after the end of the depreciation.

- life: The life (in periods) of an asset over which the asset will get deprecated.

Explanation:

- The Cost value is at cell B1, as a result, the B1 is passed as a cost argument in the SLN function.

- The Salvage value is at cell B3, as a result, the B3 is passed as salvage in the SLN function.

- The Life value is at cell B2, as a result, the B2 is passed as life in the SLN function.

- Consequently, the sequence of arguments will be like (B1, B3, B2).

-

Question 31

5 / -1

Mohit, Abhay and Vikas are partners in a firm sharing profits and losses in the ratio of 3 ∶ 3 ∶ 1. On 1st April 2021, they decided to change their profit sharing, ratio to 2 ∶ 2 ∶ 3. On that date, debit balance of Profit and Loss A/c ₹70,000 appeared in the balance sheet and partners decided to pass an adjusting entry for it.

Which of the following option represents the correct treatment for the above?

| Date | Particular | L.F. | Dr. (₹) | Cr. (₹) |

(a) | Vikas's Capital A/c Dr To Mohit's Capital A/c To Abhay's Capital A/c (Being adjustment entry passed) | | 20,000 | 10,000 10,000 |

(b) | Vikas's Capital A/c Dr To Mohit's Capital A/c To Abhay's Capital A/c (Being adjustment entry passed) | | 20,000 | 15,000 5,000 |

(c) | Mohit's Capital A/c Dr Abhay's Capital Dr To Vikas's Capital A/c (Being adjustment entry passed) | | 15,000 5,000 | 20,000 |

(d) | Mohit's Capital A/c Dr Abhay's Capital A/c Dr To Vikas's Capital A/c (Being adjustment entry passed) | | 10,000 10,000 | 20,000 |

Solution

The correct answer is c.

Key PointsOld Ratio of Mohit, Abhay and Vikas = 3:3:1

New Ratio of Mohit, Abhay and Vikas = 2:2:3

Debit balance of Profit and Loss Account is to be distributed in Sacrificing Ratio.

Hence, Sacrifice/Gain = Old Ratio - New Ratio

Mohit = 3/7 - 2/7 = 1/7 (in case of loss Mohit is gaining)

Abhay = 3/7 - 2/7 = 1/7

Vikas = 1/7 - 3/7 = -2/7

Share of Mohit = 1/7 x 70,000 = 10,000

Share of Abhay = 1/7 x 70,000 = 10,000

Share of Vikas = 2/7 x 70,000 = 20,000

Hence, adjusting entry will be:

| Date | Particulars | LF | Dr. | Cr. |

| (a) | Mohit's Capital A/c Dr | | 10,000 | |

| | Abhay's Capital A/c Dr | | 10,000 | |

| | To Vikas's Capital A/c | | | 20,000 |

| | (being adjustment entry passed) | | | |

Note : Debit balance of P&L a/c denotes loss, and the adjustment entry has been passed accordingly

-

Question 32

5 / -1

Quick ratio of Affon Ltd. is 2.5 ∶ 1. Accountant wants to maintain it at 2 ∶ 1. Following options are available.

(i) He can pay off sundry creditors.

(ii) He can purchase goods on credit

(iii) He can take short term loan from bank

Choose the correct option.

Solution

The correct answer is Only (ii) and (iii) are correct.

Key PointsQuick Ratio : It is the ratio of quick (or liquid) asset to current liabilities. It is expressed as Quick ratio = Quick Assets : Current Liabilities or Quick Assets / Current Liabilities. The quick assets are defined as those assets which are quickly convertible into cash. While calculating quick assets we exclude the inventories at the end and other current assets such as prepaid expenses, advance tax, etc., from the current assets. Because of exclusion of non-liquid current assets it is considered better than current ratio as a measure of liquidity position of the business. It is calculated to serve as a supplementary check on liquidity position of the business and is therefore, also known as ‘Acid-Test Ratio’.

Important PointsThe given Quick ratio is 2 .5: 1. Let us assume that Quick assets are Rs. 25,000 and current liabilities are Rs. 10,000; Thus, the quick ratio is 0.. Now we will analyse the effect of given transactions on quick ratio.

(i)Assume that Rs. 5,000 of creditors is paid by cheque. This will reduce the quick assets to Rs. 20,000 and current liabilities to Rs. 5,000 The new ratio will be 4:1.(Rs. 20,000/Rs.5,000). Hence, it will not be included because it improved the ratio.

(ii)Assume that goods of Rs. 5,000 are purchased on credit. This will increase the Quick assets to Rs. 30,000 and current liabilities to Rs. 15,000. The new ratio will be 2:1 (Rs. 30,000/Rs. 15,000). Hence, it has reduced, will be included.

(iii) Assume that Short term loan has been taken of Rs. 5,000. This will increase quick assets to Rs.30,000 and current liabilities to Rs. 15,000.The new ratio will be 2:1 (30,000/15,000).Hence it has reduced the ratio, will be included.

-

Question 33

5 / -1

Which of the following persons cannot become a partner in a partnership firm in any condition?

(i) Minor

(ii) Persons of complete unsound mind

(iii) Persons disqualified by any law

Solution

The correct answer is (ii) and (iii).

A Persons of unsound mind and Persons disqualified by any law cannot become a partner in a partnership firm in any condition.

Key Points Partnership :

A partnership is a type of business in which two or more persons sign a legal agreement to be co-owners, allocate duties for running an organisation, and share the profits and losses generated by the enterprise.

Types of Partnerships:

- General Partnership

- Limited Partnership

- Limited Liability Partnership

- Partnership at Will

Important Points1. Minor as a Partner:

Though a minor cannot be a partner in a firm, under Section 30 of the Indian Partnership Act, he may be entitled to the advantages of partnership by an agreement executed through his guardian with the other partners with the approval of all the partners for the time being.

Conditions of minor becoming a partner:

- With the approval of all existing partners, a minor can be admitted to the benefits of partnership. It should be noted that a minor must have the approval of all partners before being allowed in a partnership.

- Before a minor to be admitted to the benefits of a partnership, it must first exist. As a result, a minor cannot form a new partnership but can join an existing one.

- There cannot be a partnership consisting of all minors

Hence, under certain conditions, a minor can become a partner.

2. Persons of complete unsound mind:

Persons of unsound mind cannot become a partner in a partnership firm in any condition.

3. Persons disqualified by any law

Persons disqualified by any law cannot enter into any contract and since partnership is established by a contract between persons entering into partnership, Persons disqualified by any law cannot become a partner.

-

Question 34

5 / -1

Investments made by a financial enterprise with the purpose to resell after the expiry of three months will come under which of the following activity in a Cash flow statement?

Solution

The correct answer is Operating

Key Points

Cash Flow Statement:

- A cash flow statement (CFS) is a financial statement that shows how much cash and cash equivalents are coming in and going out of a business.

- The CFS assesses a company's ability to manage its cash position, or how successfully it generates cash.

- The CFS is a useful addition to the balance sheet and income statement.

- Cash is the most important component of the CFS, and it comes from three sources: operating, investing, and financing activities.

Important Points

Investments made by a financial enterprise with the purpose to resell after the expiry of three months:

- This amount will be qualified as current assets since, it is sold within 12 months.

- All the cash flows from current assets are recorded as cash flows from operating activities.

- Hence, Investments made by a financial enterprise with the purpose to resell after the expiry of three months will be considered as Operating Activities.

-

Question 35

5 / -1

Which of the following are Solvency ratios?

(i) Debt Equity Ratio

(ii) Current Ratio

(iii) Total Assets to Debt Ratio

(iv) Quick Ratio

(v) Gross Profit Ratio

Solution

The correct answer is (i) and (iii)

Key Points Solvency ratios:

- Solvency ratios are an important part of financial analysis since they assist to determine if a company has enough cash flow to meet its debt commitments.

- Leverage ratios are another name for solvency ratios.

- It is thought that if a company's solvency ratio is low, it is more likely to be unable to meet its financial obligations and to default on debt repayment.

Important PointsSolvency Ratios:

1. Debt Equity Ratio: It is an important statistic for determining a company's financial leverage. This ratio determines if the shareholder's equity has the ability to satisfy all debts in the event of a business failure. Debt to equity is one of the most used debt solvency ratios.

Formula: Debt to equity ratio = Long term debt / shareholder’s funds

2. Debt to Asset Ratio:

- A debt-to-assets ratio is a sort of leverage ratio that compares a company's total assets to its debt obligations (including short- and long-term debt).

- A company with a debt-to-assets ratio greater than one has more debt than assets.

- The business has more assets than debt if the ratio is less than one.

Formula: Debt-to-Assets Ratio = Total Debt / Total Assets.

Additional Information 1. Current Ratio: The current ratio is a type of liquidity ratio that assesses a company's capacity to pay off its debts within the next twelve months. Creditors use this ratio to determine if a company is eligible for short-term debt. It also contains data about the company's operational cycle. Formula: Current ratio = Current Assets / Current Liabilities

2. Quick Ratio: The quick ratio, also known as the acid test ratio, is a type of liquidity ratio which is used to establish whether a firm or a business has sufficient liquid assets that can be converted into cash quickly enough to pay short-term obligations. Formula: Quick Ratio = (Cash + Marketable securities + Accounts receivable) / Current liabilities.

3. Gross Profit Ratio: Gross Profit Ratio is a profitability ratio that measures the relationship between the gross profit and net sales revenue. When it is expressed as a percentage, it is also known as the Gross Profit Margin. Formula: Gross Profit Ratio = Gross Profit/Net Revenue of Operations × 100

-

Question 36

5 / -1

As per the Companies Act 2013, Sweat equity shares are issued by a company, to its _______ for non cash consideration or at a discount for providing know how's or any value additions in any form:

Solution

The correct answer is Director or Employees

Key Points

Sweat Equity Shares:

Sweat Equity Shares are equity shares issued by a company at a discount or for a consideration other than cash to a director or employee in exchange for giving know-how or making available intellectual property rights or value addition.

Important Points Section 54 of Companies Act 2013:

Notwithstanding anything contained in section 53, a company may issue sweat equity shares of a class of shares already issued, if the following conditions are fulfilled, namely:—

- the issue is authorised by a special resolution passed by the company

- the resolution specifies the number of shares, the current market price, consideration, if any, and the class or classes of directors or employees to whom such equity shares are to be issued

- not less than one year has, at the date of such issue, elapsed since the date on which the company had commenced business; and

- where the equity shares of the company are listed on a recognised stock exchange, the sweat equity shares are issued in accordance with the regulations made by the Securities and Exchange Board in this behalf and if they are not so listed, the sweat equity shares are issued in accordance with such rules as may be prescribed

-

Question 37

5 / -1

Amar, Sanjay and Rajesh are partners, their partnership deed provides for interest on drawings at 6% per annum. Rajesh withdrew a fixed amount in the end of every month, during the year and his interest on drawings amounted to ₹6,600 at the end of the year. What was the amount of his monthly drawings?

Solution

he correct answer is ₹20,000.

Key PointsInterest on partner's drawings - No interest is to be charged on the drawings made by the partners, if there is no mention in the Deed. Interest on Drawings are Debited in Partner's Capital Account.

Calculation of Interest on drawings When Fixed Amounts was Withdrawn Every Month-

Interest on drawings = Total Drawing in a year x Average period/12 x rate of interest/100

Average period:

1.When the amount is withdrawn at the beginning of each month= 6.5 months

2. When the amount is withdrawn at the end of each month= 5.5 months

3.When money is withdrawn in the middle of the month= 6months

Important PointsInterest on drawing of Rajesh's capital = Rs.6,600

Avg. Period = 5.5 months

Rate of Interest = 6%p.a

Interest on drawings = Total Drawing in year x Average period/12 x rate of interest/100

6,600 =Total Drawing in year x 5.5/12 x 6/100

Drawing in a year = 6,600 x 12/5.5 x 100/6

= Rs.2,40,000

Drawing per month = Rs.2,40,000/12

=Rs.20,000 p.m.

Thus, Drawing for per month is Rs.20,000 p.m.

Additional Information

- Calculation of Average period when Fixed Amount is withdrawn Quarterly -

- If the amount is withdrawn at the beginning of each quarter = 7.5 months

- If the amount is withdrawn at the end of each quarter = 4.5 months

2.Caluation of interest on drawing When Varying Amounts are Withdrawn at Different Intervals=

=Total of products × Rate × 1/12

-

Question 38

5 / -1

Sunil, Naresh and Joginder are the partners sharing profits and losses in the ratio of 3 ∶ 2 ∶ 1 with capitals of ₹2,00,000, ₹2,00,000 and ₹1,00,000 respectively. Partnership Deed provides for interest on Capital @ 10% p.a. and profit for the year is ₹25,000. How much interest will be provided on Sunil's Capital during the year?

Solution

The correct answer is ₹10,000.

Key PointsInterest on partner's capital - No partner is entitled to claim any interest on the amount of capital contributed by him in the firm as a matter of right. However, interest can be allowed when it is expressly agreed to by the partners. Thus, no interest on capital is payable if the partnership deed is silent on the issue.

Important PointsSunil's Capital = Rs.2,00,000

Interest on capital = 10%p.a.

Interest on Sunil's Capital = Rs.2,00,000 x 10/100 = Rs.20,000

Interest on Naresh's Capital = Rs.2,00,000 x 10/100 = Rs.20,000

Interest on Joginder's Capital = Rs.1,00,000 x 10/100 = Rs.10,000

Interest on Capital ratio = Sunil : Naresh : Joginder

= 20000 :20000 :10000

=2:2:1

Total Interest on capital = 20000+20000+10000 = Rs 50,000

Total Profit = Rs.25,000

Note : Interest on capital is greater than total profit, so interest on capital will be distributed in interest on capital ratio.

Interest on Sunil's Capital = Rs.25,000 x 2/5 = Rs.10,000

-

Question 39

5 / -1

Happyall Ltd has Issued Capital of 1,00,000 Equity shares of ₹10 each. Till Date, ₹8 per share have been called up and the entire amount received except calls of ₹2 per share on 4,000 shares and ₹3 per share from another holder who held 6,000 shares. What will be amount appearing as ‘Subscribed but not fully paid capital' in the balance sheet of the company?

Solution

The correct answer is ₹7,74,000.

Key Points

Issued capital - The part of the allowed capital that is actually offered to the public for subscription, including the shares granted to vendors and signatories to the company's memorandum, is known as issued capital.

Subscribed Capital - It is the portion of the issued capital that has been subscribed by the general public. When the public shares offered for public subscription are fully subscribed, the issued capital and subscribed capital are equal.

Important PointsIssued shares = subscribed shares = 1,00,000 Shares

Face value of shares = Rs.10 per shares

Issued capital = Subscribed Capital = 1,00,000 x 10 = Rs.10,00,000

Called up amount = Rs.8 per shares

Called Capital = Rs.8 x 100000

Called Capital = Rs.8,00,000

Calls in arrears = 4,000 x 2 + 6,000 x 3

Calls in arrears = Rs.8,000 + 18,000

Calls in arrears = Rs.26,000

Paid up Capital = Rs.8,00,000 - Rs.26,000

Paid up Capital = Rs.7,74,000

Notes to Accounts for share capital -

| Particulars | | Rs. |

| Share Capital | | |

| Authorized or Registered or Nominal Capital | | |

| __________Shares of each Rs.10 | | |

| | | |

| Issued Capital | | |

| 1,00,000 Shares of Each Rs.10 | | 10,00,000 |

| | | |

| Subscribed Capital | | |

| Subscribed but not fully paid up | | |

| 1,00,000 Shares of Rs.10 each, Rs.8 called up | 8,00,000 | |

| Less : Calls in Arrears | (26,000) | 7,74,000 |

-

Question 40

5 / -1

Nirav, Sahil and Gautam are partners in the ratio of 3 ∶ 3 ∶ 2. If Nirav's share of profit at the end of the year amounted to 3,00,000, what will be Gautam's share of profits?

Solution

The correct answer is ₹2,00,000.

Key PointsProfit & loss ratio - Over a certain time period, the average profit on winning transactions is divided by the average loss on losing deals.

Important PointsNirav's Share of Profit = 3/8

Nirav's share of profit in the end of year= Rs.3,00,000.

Total Profit of firm=Rs.3,00,000 x 8/3

=Rs.8,00,000

Gautam's share of profits= Rs.8,00,000 x 2/8

=Rs.2,00,000

Thus, Gautam's share of profits is Rs.2,00,000.

-

Question 41

5 / -1

What will be the output of the following MS-Excel formula?

=AVERAGE (4, 5, 3, 8)

Solution

The Excel AVERAGE function calculates the average (arithmetic mean) of supplied numbers.

Key PointsAverage is the arithmetic mean and is calculated by adding a group of numbers and then dividing by the count of those numbers. For example, the average of 2, 3, 3, 5, 7, and 10 is 30 divided by 6, which is 5.

Syntax

AVERAGE(number1, [number2], ...)

The AVERAGE function syntax has the following arguments:

- Number1 Required. The first number, cell reference, or range for which the user wants the average.

- Number2, ... Optional. Additional numbers, cell references, or ranges for which the user wants the average, up to a maximum of 255.

The output of the given MS-Excel formula

=AVERAGE (4, 5, 3, 8) is 5

-

Question 42

5 / -1

VBT Ltd foreited 2,000 shares of ₹10 each, fully called up, on which application money of ₹3 has been paid. Out of these 500 shares were reissued and 500 has been transferred to capital reserve. Calculate the rate at which these shares were reissued.

Solution

The correct answer is ₹8 Per share.

Key PointsForfeiture of Shares - Shares are forfeited when shareholders fail to pay one or more instalments on shares that have been assigned to them. The corporation has the ability to confiscate the defaulters' shares in such a circumstance. This is known as 'Share Forfeiture.'

Reissue of shares -Forfeited shares may be issued again as fully paid at a par, premium, discount. It should be noted that the discount permitted on reissue of forfeited shares cannot exceed the amount received on forfeited shares at the time of first issue, and that the discount allowed on reissue of forfeited shares shall be deducted to the 'Forfeited Share Account.' The amount previously paid by the original shareholder determines the pace at which these shares are reissued.

Important Points

Forfeited Shares = 2,000 Shares

Application money = Rs.3

unpaid amount on allotment & calls = Rs.7 per shares

The rate of reissue of shares =10 - 3 = 7 per share

The minimum rate of reissue of shares = Total value of shares - money already received on shares.

=10 - 3 shares

= 7 per shares

Amount on Share forfeiture used in reissue of shares = 500 x 3 = Rs.1,500

Amount of profit on reissued shares transferred to capital reserve = Rs.500 (Given)

shares reissued = 500 shares

Profit on reissue of shares = Rs.500/500

=Rs.1

Amount of reissue par shares= minimum rate of reissue of per shares + Profit on reissue of per shares

= Rs.7 + Rs.1

= Rs.8 per Share

Additional InformationEntry for Forfeiture of 2000 Shares

| Particulars | Dr. | Cr. |

| Shares Capital A/c Dr. (2,000 x 10) | 20,000 | |

| To Shares Forfeitures A/c (2,000 x 3) | | 6,000 |

| To shares allotment & calls A/c (2,000 x 7) | | 14,000 |

| (2,000shares forfeited for non-payment of allotment money and calls made) | | |

Reissue of shares - 500 Shares

| Particulars | Dr. | Cr. |

| Share Forfeiture A/c Dr. (500 x 2) | 1,000 | |

| Cash A/c Dr.(500 x 8) | 4,000 | |

| To Share Capital A/c (500 x 10) | | 5,000 |

| Reissue of 500 forfeited shares at Rs.7 per share as fully paid) | | |

| Share Forfeiture A/c Dr. | 500 | |

| To Capital Reserve A/c | | 500 |

| (amount on profit of reissue of shares transferred to Capital reserve) | | |

-

Question 43

5 / -1

For which of the following purpose, MBB Ltd. company can utilise its Securities Premium Reserve:

Solution

The correct answer is Writing off preliminary expenses of the company.

Key Points Securities Premium Reserve:

- The additional amount charged on the face value of any share when it is issued, redeemed, or forfeited is known as the Security Premium Reserve.

- According to the Companies Act of 2013, when a security premium must be documented in the balance sheet, it must be done in the Reserve & Surplus section of the Equity & Liabilities section of the balance sheet.

- This item has been added to the Reserve & Surplus category.

- Furthermore, reserve and surplus keep track of all revenues and losses.

Important Points Section 52 Sub-section (2) of Companies Act 2013

The securities premium account may be applied by the company—

- towards the issue of unissued shares of the company to the members of the company as fully paid bonus shares;

- in writing off the preliminary expenses of the company;

- in writing off the expenses of, or the commission paid or discount allowed on, any issue of shares or debentures of the company

- in providing for the premium payable on the redemption of any redeemable preference shares or of any debentures of the company

- for the purchase of its own shares or other securities under section 68

-

Question 44

5 / -1

Own debentures are those debentures of the company which ?

Solution

The correct answer is The company purchases from the markets and holds them as investments.

Key PointsDebentures – marketable security (a type of Loan) issued by a business or other organization to raise money for long-term activities and growth and yielding a fixed rate of interest. Debentures can be issued at par, at premium and at discount.

Important PointsOwn Debentures - When a firm purchases its own debentures for investing purposes rather than cancellation, called "Own Debentures" is created in the records. Regardless of the nominal value of the debentures purchased, the Investment Account (Own Debenture Account) will be debited by the real amount paid.

Thus, Own debentures are those debentures of the company purchases from the markets and holds them as investments.

Additional Information Entries for Purchase of Own Debenture :

| Particulars | Dr. | Cr. |

| Own Debentures A/c Dr.. | xxx | |

| To Bank A/c | | xxx |

| (purchase of own debentures @Rs.___each) | | |

| % Debentures A/c Dr. | xxx | |

| To Own Debentures A/c | | xxx |

| To Profit on redemption of Debentures A/c | | xxx |

| (Own debenture purchased being cancelled) | | |

| Profit on cancellation of debentures A/c Dr. | xxx | |

| To Capital Reserve A/c | | xxx |

| (Profits on cancellation of debentures transferred to Capital Reserve) | | |

-

Question 45

5 / -1

Bhumi and Priya were partners sharing profits and losses in the ratio of 4 ∶ 1. Rashmi was admitted for \(\frac{1}{5}\)th share in the profit but was unable to bring his share of goodwill premium in cash. The Journal entry recorded for goodwill premium is given below.

| Date | Particular | L.F. | Dr. (₹) | Cr. (₹) |

| | Rashmi's Current A/c Dr To Bhumi's Capital A/c To Priya's Capital A/c (Adjustment of goodwill premium on Rashmi's Admission) | | 30,000 | 24,000 6,000 |

The new profit-sharing ratio of Bhumi, Priya and Rashmi will be

Solution

The correct answer is 16 ∶ 4 ∶ 5.

Key Points Profit & Loss ratio - ratio in which profit or loss of partner's share are calculated.

When the new Partner brings goodwill in cash-

Important PointsCalculation of Sacrifice ratio=Bhumi : Priya

= 24,000 : 6,000

=4:1

Rashmi Share of profit= 1/5

Bhumi's share of sacrifice = 4/5 x 1/5 = 4/25

Priya's share of sacrifice = 1/5 x 1/5 = 1/25

Calculation of new Profit & Loss Share Ratio= Old ratio - Sacrifice ratio

Bhumi's share of profit= 4/5 -4/25= (20-4)/25= 16/25

Priya's share of profit=1/5 - 1/25= (5-1)/25=4/25

Rashmi Share of profit= 1/5 = 5/25

Thus, New Profit & Loss Share Ratio will be

Bhumi : Priya : Rashmi

16 : 4 : 5

-

Question 46

5 / -1

Manger is entitled to a commission of 10% of the net profits after charging such commission. The net profit for the year is Rs 1,32,000. What will be the amount of manger's commission?

Solution

The correct answer is Rs. 12,000.

Key PointsManager's Commission on Net Profits:- Sometimes, the manager is to be allowed a certain percentage of net profits as his commission. It is calculated by two methods as given below:-

(I) On profits before charging such commission : For example- if the profit before charging his commission is Rs. 44,000 and the manager is to be allowed a commission of 10% on the profit before charging such commission, the commission will be :-

Manager's commission = Net profits x Rate / 100

44,000 x 10/100 = Rs. 4,400

(II) On profits after charging such commission : For example - if the profit before charging his commission is Rs. 44,000 and the manager is to be allowed a commission of 10% on the profit after charging such commission, the commission will be :

Manager's commission = Net profits x Rate / (100 +Rate)

44,000 x 10/110 = Rs. 4,000

Important PointsThe given question is of Case II, hence manager's commission will be calculated as follows:

Net Profit = 1,32,000 (given)

Manager's Commission = 10%

Manager's commission = Net profits x Rate / (100+Rate)

Hence, Manager's commission = 1,32,000 x 10/110 = 12,000.

-

Question 47

5 / -1

One or more than one attributes that can be used to uniquely identify the tuples in the relation are know as _______________.

Solution

The correct answer is option (4)

Concept:-

One or more attributes can take different values in relation. Any of these attributes can be used to identify the tuples in relation to a unique way. As each of these properties is a candidate for the primary key, they are referred to as candidate keys.

Key Points

- The set of attributes that can uniquely identify a tuple is known as Super Key.

- At any given time, a multivalued attribute can have more than one value. Consider the address field, which accepts several values such as zip code, street address, state, and so on.

- A key is a characteristic (or group of properties) that allows us to identify the rows of a table in a unique way.

Additional InformationPrimary keys:- It uniquely identifies each record in a table. It must have unique values and cannot contain nulls. For example, the ROLL NO. field is marked as the primary key, which means the ROLL NO. field cannot have duplicate and null values.

Composite keys:- A composite key is made up of various columns that are used to uniquely identify all of the rows that are involved.

Foreign key:- Foreign keys are the columns of a table that points to the primary key of another table. They act as a cross-reference between tables.

-

Question 48

5 / -1

A and B were partners sharing profits and losses in the ratio of 4 ∶ 3. On 1st April, 2021 they admitted C as a new partner and new ratio was decided as 3 ∶ 3 ∶ 1. Goodwill of the firm was valued as ₹7,00,000. C brought his required share of goodwill premium in cash. Cs share of goodwill credited to A and B Capital Accounts by:

Solution

The correct answer is

Key PointsWhen the new Partner brings goodwill in cash-

When the new Partner does not bring goodwill in cash-

- New Partner's Current or capital account is debited and Old Partner's capital account is credited.

Important Points Calculation of Sacrifice Ratio -

Sacrifice Ratio= Old Ratio - New Ratio

A's share = 4/7 - 3/7 = 1/7

B's share = 3/7 - 3/7 = 0

Here, only A's sacrifice, so A's account will be credited.

Total Firm of Goodwill = Rs.7,00,000

C's share of Profit = 1/7

C's share of Goodwill = Rs.7,00,000 x 1/7

= Rs.1,00,000

Thus, A's Capital account will be credited by Rs.1,00,000 & B's Capital account is Nil.

Additional Information

Entry for Goodwill bring by C in Cash -

| Particulars | Dr. | Cr. |

| Premium for goodwill A/c Dr. | 1,00,000 | |

| To A's Capital A/c | | 1,00,000 |

| (goodwill bring by C) | | |

-

Question 49

5 / -1

Which of the following statements are false?

(i) Comparative Financial Statement is an indicator of trend and helps in forecasting.

(ii) In Common Size Financial Statement, 100% is taken as base and all other related amounts are expressed as a percentage of base.

(iii) Analysis through Comparative Financial Statement is also known as Horizontal Analysis.

Choose from the following Options:

Solution

The correct answer is All are true.

Key PointsFinancial analysis means analysis and interpretation of financial statements. Financial analysis helps to know financial position, operational efficiency, future prospectus of business and also helps to make decisions in future.

Important Points(i) Comparative Financial Statement is an indicator of trend and helps in forecasting is true because

Comparative Financial statement- an item compared with itself in the previous year to know whether it has increased or decrease. The data in comparative statements can be used to determine the direction of changes as well as trends in various measures of an organization's performance & helps in Forecasting\projections.

(ii) In Common Size Financial Statement, 100% is taken as base and all other related amounts are expressed as a percentage of base is true because

Common size statement- an item compared with itself in the previous year to know whether it has increased or decreases in percentage ratio. Thus, in Common Size Financial Statement, 100% is taken as base and all other related amounts are expressed as a percentage of base.

(iii) Analysis through Comparative Financial Statement is also known as Horizontal Analysis is true because

Horizontal analysis takes the form of comparative statements. The profitability and financial condition of a company are shown in a comparative form in a common size statement to offer an impression of the status of two or more periods.

Thus, Option (i) , (ii) & (iii) are true.

-

Question 50

5 / -1

Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R):

Assertion (A) : After reissue of all the forfeited shares, balance left in Forfeited Shares Account is transferred to General Reserve Account.

Reason (R) : Gain on reissue of forfeited shares is of revenue nature that is why it is transferred to General Reserve A/c.

In the context of the above statements, which one of the following is correct?

Solution

The correct answer is Both (A) and (R) are false.